New Chapter 11 Bankruptcy Filing - Briggs & Stratton Corporation ($BGG)

Briggs & Stratton Corporation

July 20, 2020

You may not know of Briggs & Stratton Corporation ($BGG) but it’s likely that you’ve used one of its products. Its small gasoline engines are used in outdoor power equipment like lawn mowers, and it designs, manufactures and markets power generation, pressure washer, lawn and garden, turf care and job site products. Its engines even power go-karts! It offers a variety of different brands and its products are in 100 countries around the world.

The company has a rich history. In Wisconsin circa 1908, inventor Stephen Briggs and investor Harold Stratton co-founded what, two years later, would be an auto and auto parts manufacturer incorporated as Briggs & Stratton. The two men added small gasoline engines to their product suite, powering early washing machines and reel mowers. The company went public in 1928. For decades thereafter, the business ventured into agricultural and military applications (producing generators for the WWII effort), ultimately revolutionizing the first lightweight aluminum engine in 1953. The post-War suburbian boom helped fuel the company’s growth in the 50s and 60s. Lots of lawns to mow! The company has iterated a lot since then: it no longer produces auto components, for instance. The core business is currently focused around two segments: engines (primarily sold to OEMs of lawn and garden equipment) and products (i.e., outdoor power equipment, job site products, etc.).

Unfortunately, a rich history doesn’t insulate companies from distress — a lesson that many long-standing companies have learned lately as the bankruptcy bin fills to the brim with companies with 100+ year histories (see, also, BJ Services LLC, Brooks Brothers Group, RTW Retailwinds, Congoleum Corporation). Alas, the company and four affiliates (the “debtors”) also could not avoid chapter 11, filing early Monday in the Eastern District of Missouri, and citing (i) cautious ordering patterns from channel partners, (ii) weather, (iii) Sears’ demise and bankruptcy (bankruptcy dominos!!), (iv) consumer preference shifts, and (v) China, for its troubles. With approximately $200mm of notes maturing at year end (Dec) and a springing maturity of 9/15/20 if the notes are still outstanding by then, the debtors, to top things off, faced real challenges related to the balance sheet.

Because of all of the aforementioned factors, the debtors implemented a “strategic repositioning plan” that included shutting plants, laying off workers, suspending employee benefits (including underfunded and unfunded pensions), lowering capital and discretionary spending, eliminating a shareholder dividend and suspending a share repurchase program. COVID-19, as we’ve seen over and over again, got in the way of these efforts. “The preliminary estimate of the sales decline caused by the pandemic for the fiscal fourth quarter was $157 million and for the fiscal year was $197 million.” 😬

The good news is that the debtors have a buyer in the wings. Bucephalus Buyer LLC, a dramatically-named affiliate of KPS Capital Partners LP entered into a stalking horse purchase agreement with the debtors pursuant to which it would buy the debtors’ assets and equity interests in non-debtor subsidiaries for $550m in cash plus the assumption of certain liabilities. To fund this process (and take out the ABL in full), the debtors obtained (i) a commitment from prepetition ABL lender, JPMorgan Chase Bank NA, for a $412.5mm DIP ABL (L+3.5%), (ii) a commitment from KPS for a $265mm DIP Term Loan facility (L+7%) and (iii) consent to use the ABL lenders’ cash collateral. The DIP agreement mandates that a qualified sale order be entered by the bankruptcy court no later than September 24, 2020 (subject to caveats that would push the date out to December 31, 2020).

Jurisdiction: E.D. of Missouri (Judge Schermer)

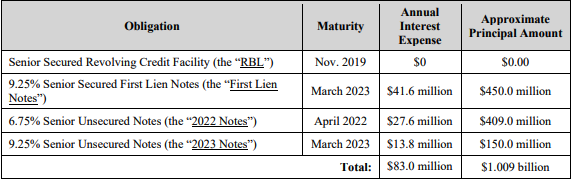

Capital Structure: $260.4mm North American ABL, $53mm LOCs, $12.4mm Swiss ABL (JP Morgan Chase Bank NA), 202.7mm unsecured notes (Wilmington Trust NA)

Professionals:

Legal: Weil Gotshal & Manges LLP (Gary Holtzer, Ronit Berkovich, Debora Hoehne, Martha Martir, Andrew Citron, Edward Soto, Janiel Jodi-Ann Myers, Lauren Alexander, Corey Berman) & Carmody MacDonald PC (Robert Eggmann, Christopher Lawhorn, Danielle Suberi, Thomas Riske, Lindsay Leible Combs, Angela Drumm)

Financial Advisor: EY (Jeffrey Ficks)

Investment Banker: Houlihan Lokey Capital Inc. (Reid Snellenbarger, Jeffrey Lewis)

Claims Agent: KCC (*click on the link above for free docket access)

Other Parties in Interest:

Prepetition & DIP Agent ($677.5mm): JPMorgan Chase Bank NA

Legal: Latham & Watkins LLP (Peter Knight, Jonathan Gordon)

Stalking Horse Purchaser ($550mm): Bucephalus Buyer, LLC (KPS Capital Partners LP)

Legal: Kirkland & Ellis LLP (Chad Husnick, Gregory Pesce, Claire Stephens, Guy Macarol) & Armstrong Teasdale LLP (Richard Engel)

Ad Hoc Group of Noteholders

Legal: Gibson Dunn & Crutcher LLP

Financial Advisor: Imperial Capital LLC