New Chapter 11 Bankruptcy & CCAA Filing - Pier 1 Imports Inc. ($PIR)

Pier 1 Imports Inc.

February 17, 2020

Fort Worth, Texas-based Pier 1 Imports Inc. and seven affiliates (the “debtors”) have fulfilled their obvious destiny and finally fallen into bankruptcy court in the Eastern District of Virginia. Contemporaneously, the debtors filed a CCAA proceeding in Canada to effectuate the closure of all Canadian operations. Color us pessimistic but we’re not feeling so great about the debtors’ go-forward chances in the US either.

We’ve covered the debtors ad nauseum in previous editions of PETITION. Here — supported by an ode to “Anchorman” — we described the debtors’ recent HORRIFIC financial performance and noted how a bankruptcy would be sure to confuse a peanut gallery accustomed to spouting regular (and sometimes inaccurate) hot takes about how private equity is killing retail.* We wrote:

The reaction to this surely-imminent bankruptcy (and, if we had a casino near us, liquidation) is going to be interesting. It is sure to flummox the “Private Equity is Killing Retail” camp because, well, it’s not PE-backed. Similarly it’ll confuse the “You Shouldn’t Put So Much Debt on Retail” cohort because, well, there really isn’t that much debt on the company’s balance sheet. Chuckling in the corner will be “The US is Over-Stored” team … And “The Millennials Aren’t Buying Homes and Furnishing Them With Chinese-Made Tchotchkes” gang (thanks a ton, Marie Kondo) … And the “Management Has Blown Chunks, The Assortment Sucks” bunch … And, finally, “The Amazon Effect” squad….

Over the weekend, The New York Times ran a piece from Austan Goolsbee, an economics professor at the University of Chicago’s Booth School of Business, that — no disrespect to the professor — says many of the same things PETITION has been saying for a LONG LONG time. That is, “The Amazon Effect” is overstated. He argues that “three major economic forces have had an even bigger impact on brick-and-mortar retail than the internet has”: (1) big box stores, (2) income inequality, and (3) the preference shift away from goods towards services. It’s fair to say that these three forces affected the debtors in a big big way.**

Surely, e-commerce has a lot to do with it too. As one PETITION advisor said about the debtors’ wares yesterday:

“You can just order that sh*t online. You don’t need to try it on.”

It’s a fair point.

Another fair point that Mr. Goolsbee omits from his analysis is the role of management. It’s safe to say that the US is suffering from an epidemic of retail ineptitude.

And like the coronavirus, it keeps spreading from one retailer to the next.***

But we digress.

The business has clearly suffered:

From fiscal years 2014 to 2018, the company’s net income dropped from $108 million to about $11.6 million and in fiscal year 2019 Pier 1 experienced a $198.8 million loss.

So, what’s the upshot here? The debtors announced a plan support agreement and intend to use the chapter 11 bankruptcy process to (a) continue to shutter the previously announced ~450 stores (read: get ready for a lot of lease rejections) and (b) pursue a sale pursuant to a chapter 11 plan of reorganization of what remains of the debtors’ business. Frankly, this was masterful messaging: the announcement relating to a plan support agreement and potential plan of…wait for it…”reorganization”(!) head-faked the entire market into thinking this thing might actually be salvageable. That’s where the fine print comes in.

The debtors have dubbed this an “all weather” chapter 11 plan because it provides for either a sale or the equitization of the term loan at the term lenders’ election. This begs the question: will Pathlight Capital LP want to own this thing?🤔 This bit was eye-catching:

“To be clear, the term loan lenders have made no decision at this point, but instead support the process as outlined in the plan support agreement.”

Yeah, we bet they do. Qualified bids will be due on or before March 23 and the lenders have until March 27 to make their election. Which way will the winds blow?

Note that “the process” isn’t currently supported by a stalking horse purchaser. 🤔

Note further that the debtors are required under the DIP to distribute informational packages and solicitations for sale of the debtors’ assets on a liquidation basis to liquidators by March 9.🤔 🤔

It looks like we’ll know the answer very soon.

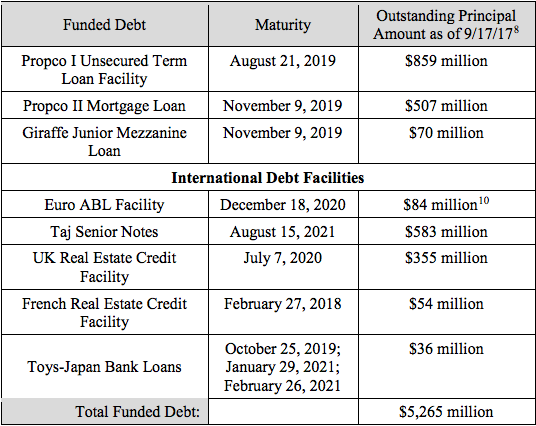

To finance the cases, the debtors obtained a committed for a $256mm DIP credit facility. The facility includes a $200mm revolving loan commitment and a $15mm first in last out term loan, each provided 50/50 by Bank of America N.A. and Wells Fargo National Association, and a $41.2mm term loan from Pathlight. This was the pre-petition capital structure:

The DIP effectively just rolls up much of the pre-petition debt. There is no new money. The messaging here, then, is also critical: the DIP facility ought to provide customers, vendors and employees comfort that there is access to liquidity if needed. Cash collateral usage, however, is the main driver here: the debtors believe that operating cash flow will suffice to handle working capital needs and bankruptcy expenses.

To summarize, we have another distressed retailer that is scratching and clawing to live. They’ve taken all of the usual steps to extend runway: cost cuts, footprint minimalization, new management. Bankruptcy is a last-ditch effort to survive: the debtors take pains to try and convince some prospective buyer that there is life left in the debtors’ brick-and-mortar business:

The remaining go-forward stores achieved superior sales and customer metrics in the last twelve months compared to the closing stores, including approximately 15% greater sales per square foot on average.

And if that doesn’t do it, there’s the argument that there’s an e-commerce play here. The debtors similarly go to great lengths to state OVER AND OVER AGAIN that e-commerce represents 27% of total sales. They’re practically screaming, “Look at me, look at me! We can be interesting to you [Insert Authentic Brands Group here]!”

Pathlight is sure as hell hoping someone bites.

*Kirkland & Ellis…uh…we mean, the “debtors” appear to agree, stating, in reference to private equity, that “[t]oo many pundits have sought to point in too many wrong directions,” citing pieces in RetailDive and The Wall Street Journal. THAT ladies and gentlemen, is client advocacy!

**It’s also fair to say that Professor Goolsbee does his readers a disservice by neglecting the overall picture which, no doubt, also includes over-expansion, too much retail per capita, private equity and over-levered balance sheets. These cowboys are closing 400+ stores for a reason.

Of course, long time PETITION readers know that we’ve been arguing for a LOOOOONG time that the “perfect storm” hitting retail is a confluence of factors that cannot just be lazily summarized as “private equity” or “The Amazon Effect.” It’s good to see that the folks at Kirkland & Ellis agree:

In the face of the longest bull run in U.S. history (close to 3,000 days and counting), a myriad of factors have collectively changed the ways in which consumers and retailers interact—creating for retailers what is tantamount to a perfect storm—and directly contributing to the struggles retailers face in a shifting marketplace.5

Then it’s as if they lifted this footnote straight out of previous PETITION briefings:

***Not to cast aspersions, but the resume of the current PIR CEO is…uh…interesting: prior experience includes FullBeauty Brands, HHGregg, and Marsh Supermarkets. Any of those names sound familiar to bankruptcy professionals?

Jurisdiction: E.D. of Virginia (Judge Huennekens)

Capital Structure: $140mm RCF + $47.3mm LOC, $189mm Term Loan (Wilmington Savings Fund Society FSB), $9.9mm industrial revenue bonds

Professionals:

Legal: Kirkland & Ellis LLP (Joshua Sussberg, Emily Geier, AnnElyse Scarlett Gains, Joshua Altman) & Kutak Rock LLP (Michael Condyles, Peter Barrett, Jeremy Williams, Brian Richardson)

Canadian Legal: Osler Hoskin & Harcourt LLP

Independent Directors: Steven Panagos & Pamela Corrie

Financial Advisor: AlixPartners LLP (Holly Etlin)

Investment Banker: Guggenheim Securities LLC (Durc Savini)

Real Estate Advisor: A&G Realty Partners LLC

Liquidation Consultant: Gordon Brothers Retail Partners LLC

Legal: Riemer & Braunstein LLP (Steven Fox, Anthony Stumbo)

Claims Agent: Epiq Corporate Restructuring LLC (*click on the link above for free docket access)

Other Parties in Interest:

DIP ABL Agent: Bank of America NA

Legal: Morgan, Lewis & Bockius LLP, Hunton Andrews Kurth LLP, and Norton Rose Fulbright Canada LLP

DIP ABL Term Agent: Pathlight Capital LP

Legal: Choate Hall & Stewart LLP (John Ventola, Jonathan Marshall) and Troutman Sanders LLP (Andrew Buxbaum)

Ad Hoc Term Lender Group: Eaton Vance Management, Insight North America LLC, Marathon Asset Management LP, MJX Asset Management LLC, Whitebox Advisors LLC, ZAIS Group LLP

Legal: Brown Rudnick LLP (Robert Startk, Uchechi Egeonuigwe, Steven Pohl, Sharon Dwoskin) & Whiteford Taylor & Preston LLP (Christopher Jones, Vernon Inge, Corey Booker)

Financial Advisor: FTI Consulting Inc.

Large Equityholders: Charles Schwab Investment Management, Dimensional Fund Advisors LLP

Official Committee of Unsecured Creditors: Bhati & Company, Synergy Home Furnishings LLC, United Parcel Services Inc., Brixmor Operating Partnership LP, Brookfield Property REIT Inc.

Legal: Foley & Lardner LLP (Erika Morabito, Brittany Nelson, Timothy Mohan) & Cole Schotz PC (Seth Van Aalten)

Financial Advisor: Province Inc. (Paul Huygens, Sanjuro Kietlinski, Walter Bowser, Paul Navid, Shane Payne, Courtney Clement)