Nine West Finally Bites It

Another Shoe Retailer Strolls into Bankruptcy Court

A few weeks back, we wrote this in “👞UGGs & E-Comm Trample Birkenstock👞,”

“Mere days away from a Nine West bankruptcy filing, we can’t help but to think about how quickly the retail landscape is changing and the impact of brands. Why? Presumably, Nine West will file, close the majority of - if not all of - its brick-and-mortar stores and transfer its brand IP to its creditors (or a new buyer). For whatever its brand is worth. We suppose the company’s lenders - likely to receive the company’s IP in a debt-for-equity swap, will soon find out. We suspect ‘not a hell of a whole lot’.”

Now we know: $123 million. (Frankly more than we expected.)

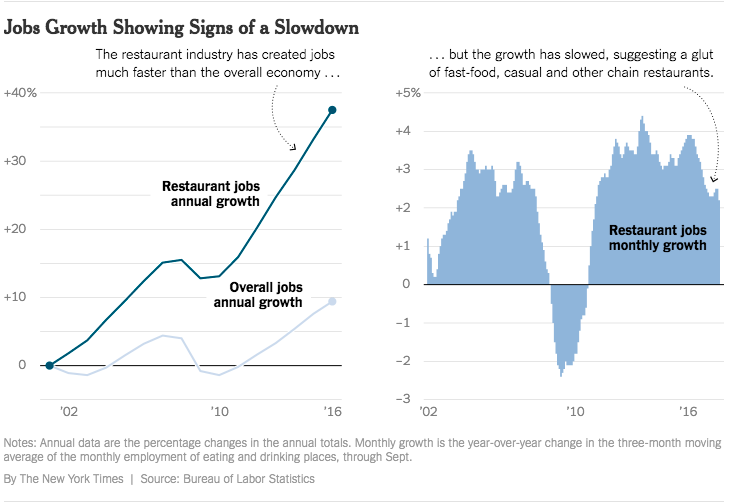

Consistent with the micro-brands discussion above, we also wrote,

“Saving the most relevant to Nine West for last,

Sales at U.S. shoe stores in February 2017 fell 5.2%, the biggest year-over-year tumble since 2009. Online-only players like Allbirds, Jack Erwin, and M.Gemi have gained nearly 15 percentage points of share over five years.

Yes, the very same Allbirds that is so popular that it is apparently creating wool shortages. Query whether this factor will be featured in Nine West’s First Day Declaration with such specificity. Likely not.”

Now we know this too: definitely not.

But Nine West Holdings Inc., the well-known footwear retailer, has, indeed, finally filed for bankruptcy. The company will sell the intellectual property and working capital behind its Nine West and Bandolino brands to Authentic Brands Group for approximately $200 million (inclusive of the above-stated $123 million allocation to IP, subject to adjustment) and reorganize around its One Jeanswear Group, The Jewelry Group, the Kasper Group, and Anne Klein business segments. The company has a restructuring support agreement (“RSA”) in hand with 78% of its secured term lenders and 89% of its unsecured term loan lenders to support this dual-process. The upshot of the RSA is that the holders of the $300 million unsecured term loan facility will own the equity in the reorganized entity focused on the above-stated four brands. The case will be funded by a $247.5 DIP ABL which will take out the prepetition facility and a $50mm new money dual-draw term loan funded by the commitment parties under the RSA (which helps justify the equity they’ll get).

Regarding the cause for filing, the company notes the following:

“The unprecedented systemic economic headwinds affecting many brick-and-mortar retailers (including certain of the Debtors’ largest customers) have significantly and adversely impacted the operating performance of the Debtors’ footwear and handbag businesses over the past four years. The Nine West Group (and, prior to its sale, Easy Spirit®), the more global business, faced strong headwinds as the macro retail environment in Asia, the Middle East, and South America became challenged. This was compounded by a difficult department store environment in the United States and the Debtors’ operation of their own unprofitable retail network. The Debtors also faced the specific challenge of addressing issues within their footwear and handbag business, including product quality problems, lack of fashion-forward products, and design missteps. Although the Debtors implemented changes to address these issues, and have shown significant progress over the past several years, the lengthy development cycle and the nature of the business did not allow the time for their operating performance within footwear and handbags to improve.”

Regarding the afore-mentioned “macro trends,” the company further highlights,

“…a general shift away from brick-and-mortar shopping, a shift in consumer demographics away from branded apparel, and changing fashion and style trends. Because a substantial portion of the Debtors’ profits derive from wholesale distribution, the Debtors have been hurt by the decline of many large retailers, such as Sears, Bon-Ton, and Macy’s, which have closed stores across the country and purchased less product for their stores due to decreased consumer traffic. In 2015 and 2016, the Debtors experienced a steep and unanticipated cut back on orders from two of the Debtors’ most significant footwear customers, which led to year over year decreases in revenue of $16 million and $46 million in 2015 and 2016, respectively. These troubles have been somewhat offset by e-commerce platforms such as Amazon and Zappos, but such platforms have not made up for the sales volume lost as a result of brick-and-mortar retail declines.”

No Allbirds mention. Oh well.

But wait! Is that a POSITIVE mention of Amazon ($AMZN) in a chapter 11 filing? We’re perplexed. Seriously, though, that paragraph demonstrates the ripple effect that is cascading throughout the retail industrial complex as we speak. And it’s frightening, actually.

On a positive note, The One Jeanswear Group, The Jewelry Group, the Kasper Group, and Anne Klein business segments, however, have been able to “combat the macro retail challenges” — just not enough to offset the negative operating performance of the other two segments. Hence the bifurcated course here: one part sale, one part reorganization.

But this is the other (cough: real) reason for bankruptcy:

Source: First Day Declaration

Soooooo, yes, don’t tell the gentlemen mentioned in the Law360 story but this is VERY MUCH another trite private equity story. 💤💤 With $1.6 billion of debt saddled on the company after Sycamore Partners Management LP took it private in 2014, the company simply couldn’t make due with its $1.6 billion in net revenue in 2017. Annual interest expense is $113.9 million compared to $88.1 million of adjusted EBITDA in fiscal year 2017. Riiiiight.

A few other observations:

Leases. The company is rejecting 75 leases, 72 of which were brick-and-mortar locations that have already been abandoned and turned over to landlords. Notably, Simon Property Group ($SPG) is the landlord for approximately 35 of those locations. But don’t sweat it: they’re doing just fine.

Liberal Definitions. As Interim CEO, the Alvarez & Marsal LLC Managing Director tasked with this assignment has given whole new meaning to the word “interim.” Per Dictionary.com, the word means “for, during, belonging to, or connected with an intervening period of time; temporary; provisional.” Well, he’s been on this assignment for three years — nearly two as the “interim” CEO. Not particularly “temporary” from our vantage point. P.S. What a hot mess.

Chinese Manufacturing. Putting aside China tariffs for a brief moment, if you're an aspiring shoe brand in search of manufacturing in China and don't know where to start you might want to take a look at the Chapter 11 petitions for both Payless Shoesource and Nine West. A total cheat sheet.

Chinese Manufacturing Part II. If President Trump really wants to flick off China, perhaps he should reconsider his (de minimus) carried interest restrictions and let US private equity firms continue to run rampant all over the shoe industry. If the recent track record is any indication, that will lead to significantly over-levered balance sheets borne out of leveraged buyouts, inevitable bankruptcy, and a top 50 creditor list chock full of Chinese manufacturing firms. Behind $1.6 billion of debt and with a mere $200 million of sale proceeds, there’s no shot in hell they’d see much recovery on their receivables and BOOM! Trade deficit minimized!!

Yield Baby Yield! (Credit Market Commentary). Sycamore’s $120 million equity infusion was $280 million less than the original binding equity commitment Sycamore made in late 2013. Why the reduction? Apparently investors were clamoring so hard for yield, that the company issued more debt to satisfy investor appetite rather than take a larger equity check. Something tells us this is a theme you’ll be reading a lot about in the next three years.

Athleisure & Casual Shoes. The fleeting athleisure trend took quite a bite out of Nine West’s revenue from 2014 to 2016 — $36 million, to be exact. Jeans, however, are apparently making a comeback. Meanwhile, the trend towards casual shoes and away from pumps and other Nine West specialties, also took a big bite out of revenue. Enter casual shoe brand, GREATS, which, like Allbirds, is now opening a store in New York City too. Out with the old, in with the new.

Sycamore Partners & Transparency in Bankruptcy. Callback to this effusive Wall Street Journal piece about the private equity firm: it was published just a few weeks ago. Reconcile it with this statement from the company, “After several years of declines in the Nine West Group business, part of the investment hypothesis behind the 2014 Transaction was that the Nine West® brand could be grown and strong earnings would result.” But “Nine West Group net sales have declined 36.9 percent since fiscal year 2015—from approximately $647.1 million to approximately $408 million in the most recent fiscal year.” This is where bankruptcy can be truly frustrating. In Payless Shoesource, there was considerable drama relating to dividend recapitalizations that the private equity sponsors — Golden Gate Capital Inc. and Blum Capital Advisors — benefited from prior to the company’s bankruptcy. The lawsuit and accompanying expert report against those shops, however, were filed under seal, keeping the public blind as to the tomfoolery that private equity shops undertake in pursuit of an “investment hypothesis.” Here, it appears that Sycamore gave up after two years of declining performance. In the company’s words, “Thus, by late 2016 the Debtors were at a crossroads: they could either make a substantial investment in the Nine West Group business in an effort to turn around declining sales or they could divest from the footwear and handbag business and focus on their historically strong, stable, and profitable business lines.” But don’t worry: of course Sycamore is covered by a proposed release of liability. Classic.

Authentic Brands Group. Authentic Brands Group, the prospective buyer of Nine West's IP in bankruptcy, is familiar with distressed brands; it is the proud owner of the Aeropostale and Fredericks of Hollywood brands, two prior bankrupt retailers. Authentic Brands Group is led by a the former CEO of Hilco Consumer Capital Corp and is owned by Leonard Green & Partners. The proposed transaction means that Nine West's brand would be transferred from one private equity firm to another. Kirkland & Ellis LLP represented and defended Sycamore Partners in the Aeropostale case as Weil Gotshal & Manges LLP & the company tried to go after the private equity firm for equitable subordination, among other causes of action. Kirkland prevailed. Leonard Green & Partners portfolio includes David's Bridal, J.Crew, Tourneau and Signet Jewelers (which has an absolutely brutal 1-year chart). On the flip side, it also owns (or owned) a piece of Shake Shack, Soulcycle, and BJ's. The point being that the influence of the private equity firm is pervasive. Not a bad thing. Just saying. Today, more than ever, it seems people should know whose pockets their money is going in to.

Official Committee of Unsecured Creditors. It’ll be busy going after Sycamore for the 2014 spin-off of Stuart Weitzman®, Kurt Geiger®, and the Jones Apparel Group (which included both the Jones New York® and Kasper® brands) to an affiliated entity for $600 million in cash. Query whether, aside from this transaction, Sycamore also took out management fees and/or dividends more than the initial $120 million equity contribution it made at the time of the transaction. Query, also, whether Weil Gotshal & Manges LLP will be pitching the committee to try and take a second bite at the apple. See #8 above. 🤔🤔

Timing. The company is proposing to have this case out of bankruptcy in five months.

This will be a fun five months.