💥Sleep Number's Sweet Dreams💥

Plus: Multi-Color Corp. closes out.

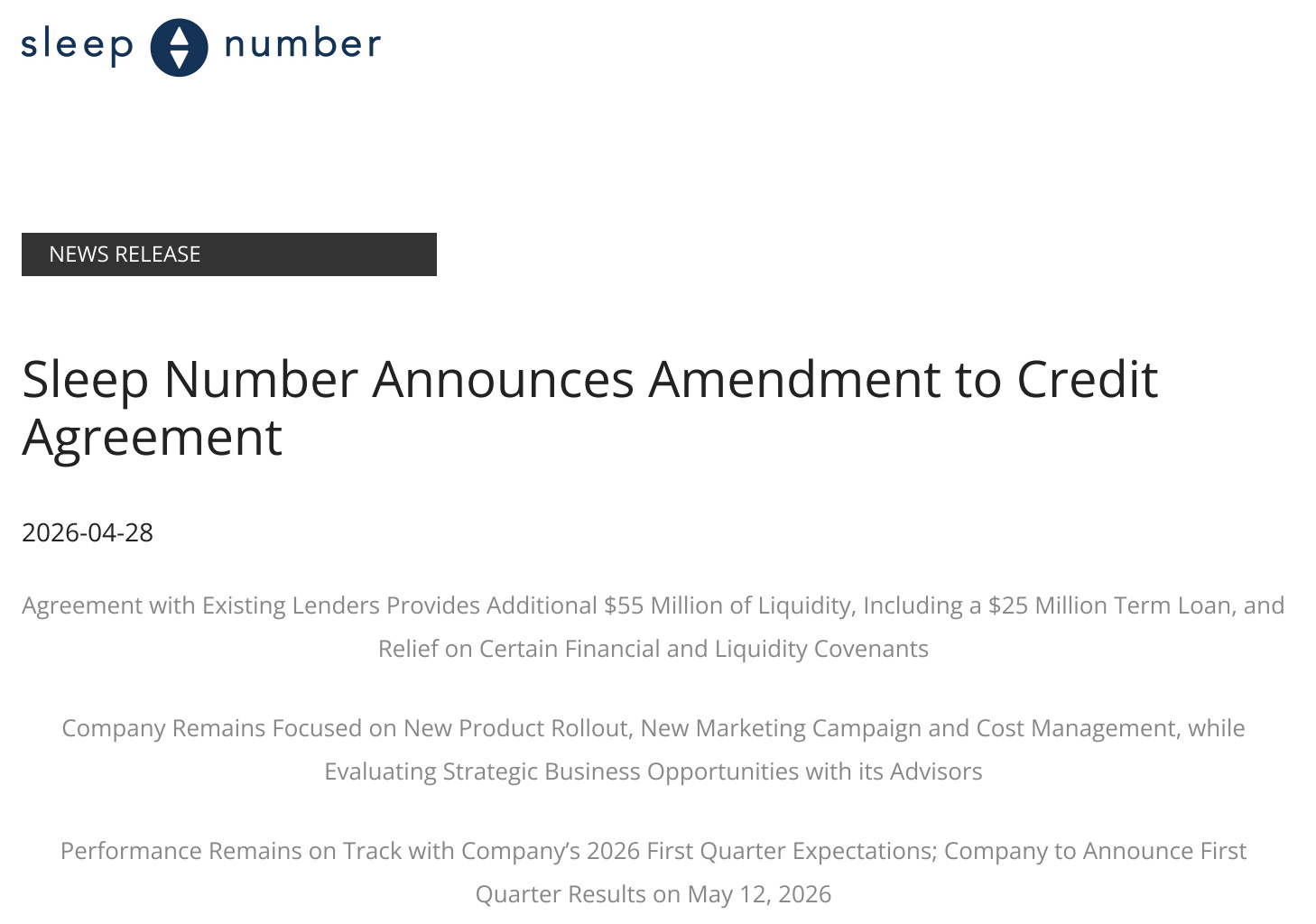

See, y’all, this 👇 is the kind of thing we’ve been talking about.

Lenders need to stop doing this sh*t. Lawyers need to stop doing this sh*t. How in hell are we all supposed to afford this Spring’s charity shakedown circuit if we don’t have chapter 11 filings filling coffers with cold hard administrative expense cash?!?

😔

As regular …