💥Hike Baby Hike💥

Raizen SA & The LYCRA Company LLC File + Multi-Color Corporation & Carbon Health Technologies Inc. updates.

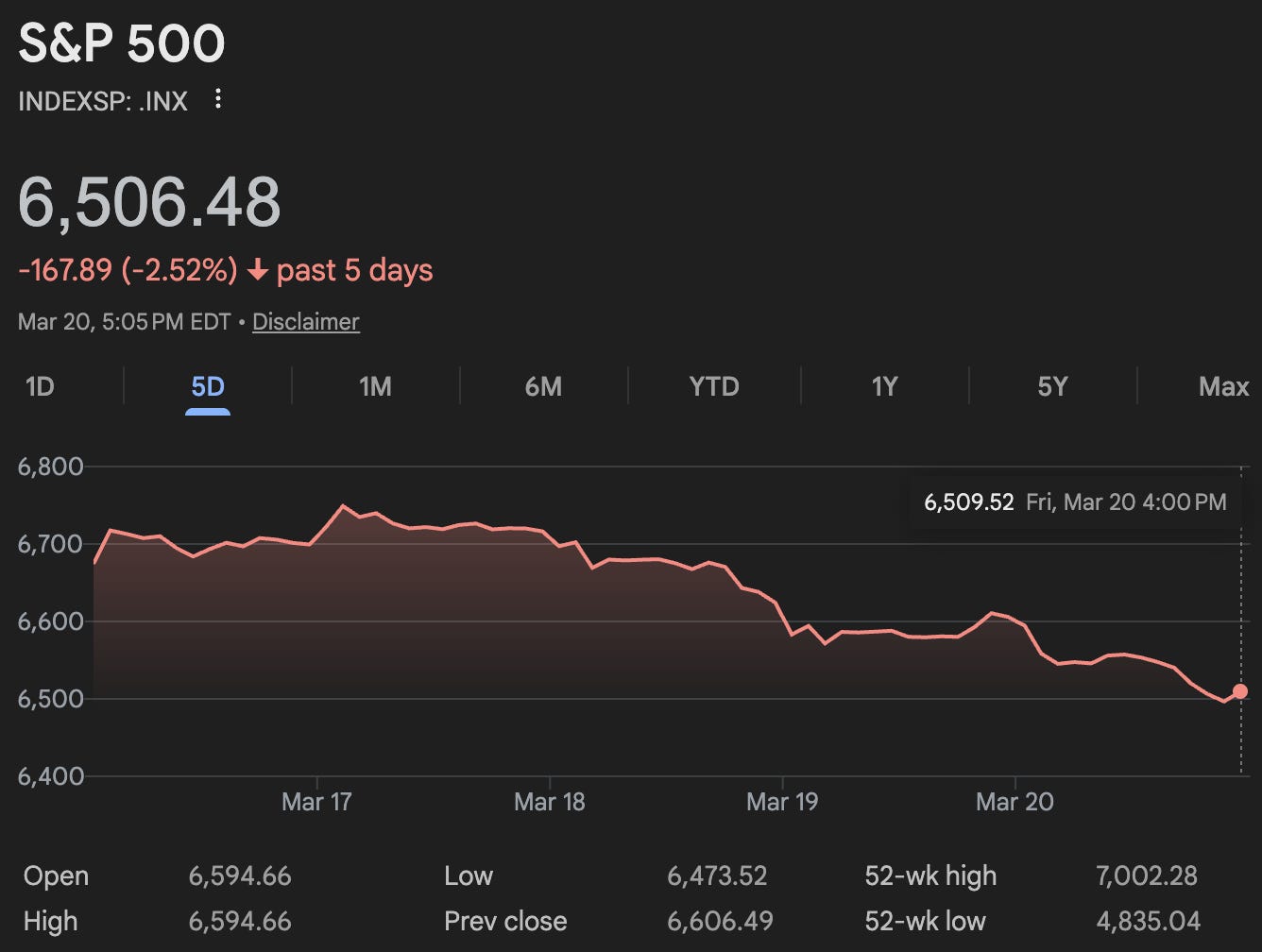

As the joint US and Israeli military action against the Islamic Republic of Iran rages on engulfing other Gulf countries and inflating oil prices around the globe, the Fed held its March meeting and to the surprise of literally no one, opted to hold the funds rate steady. Apparently the deflating number of IRGC and Basij scumbags doesn’t factor into the PCE. Who knew, 🤷♀️?

Comments from Chairman Jerome POW-ell called into question whether there’d be any additional cuts in ‘26. Okay, fine, things still seem on target for one cut later this year — in terms of the dot plot — but the market is questioning probability. Indeed, the market is reflecting that, given the Fed’s failure over such a prolonged period of time to actually hit the target rate coupled with more (inflationary) international conflict, a rate hike may actually be more realistic than a cut by year end! See 👇:

Oh, it’s actually worse than that:

Hopefully nobody tells President Trump because he may just go ahead and nuke somebody. And by “somebody,” we don’t mean whoever is next in line to be assassinated lead the Iranian regime, we mean Chairman Jerome POW-ell.

For now it’s the markets that are going nuclear.

Indeed, these charts 👇 be زشت.

That be “ugly” in Farsi.

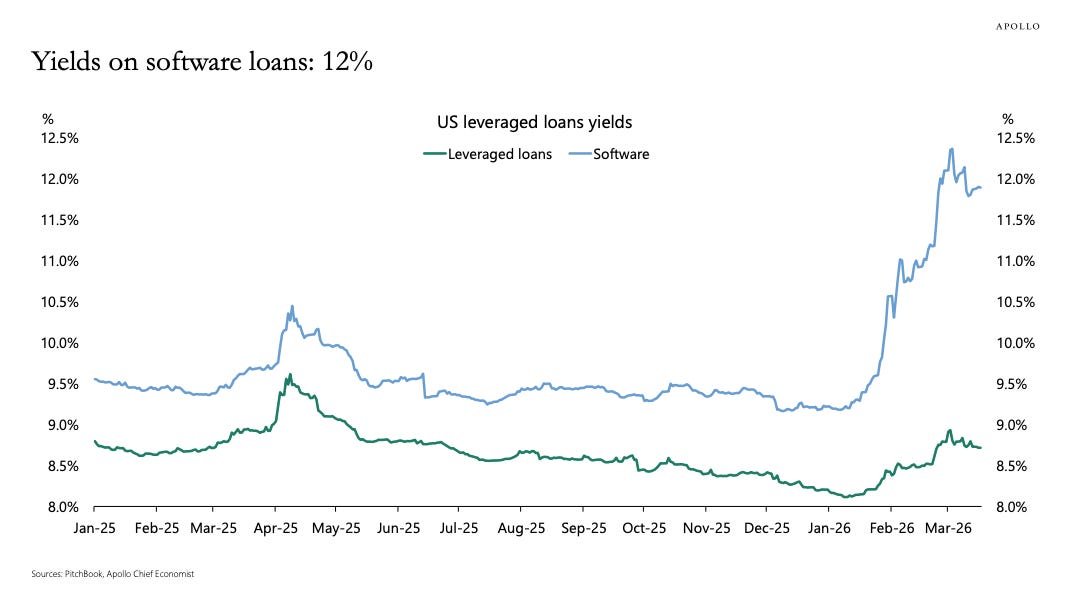

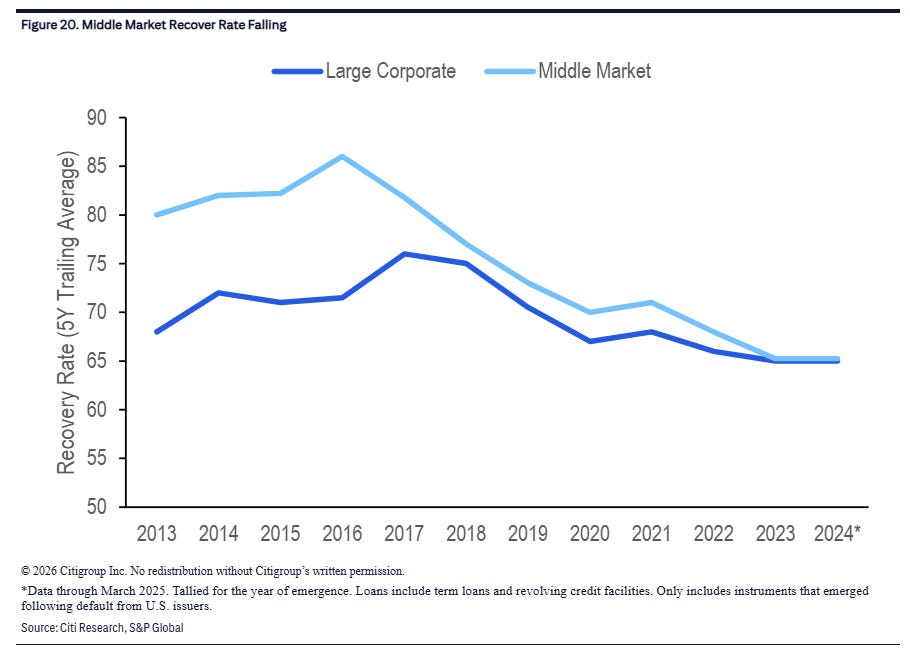

For its part, credit markets demonstrated weakness this week as rising treasury yields and macro volatility drove negative total returns. Now only 26% of leveraged loans sit above par, down from roughly 65% earlier this year. Care to guess how much of that consists of software names? We’ll spare you the suspense: just 1%.

No wonder Perella Weinberg Partners ($PWP) is hosting software-oriented seminars!

And yet things in the world of RX seem relatively tame. Yes, there’ve been a smattering of recent filings — a crypto sh*tco here, a retail sh*tco there — but nothing is really getting Johnny excited. Between LME, bankruptcy alternatives, the flood of in-court (oft-busted LME) prepacks (real and mislabeled) and AI (supposedly) coming for the lawyers among you …

… pretty soon LawDragon’s super exclusive and prestigious Top 500 RX Pros, 🙄, may deflate down to the LawDragon Top 400 RX Pros. The horror!

Anyway, Fitch Ratings (“Fitch”) released its latest default figures and … 🥁🥁🥁… not much has changed. Per Fitch:

“U.S. default rates held steady in February 2026 amid increasing geopolitical volatility, according to a new Fitch Ratings report. Trailing twelve-month (TTM) default rates were 2.7% for U.S. high-yield (HY) bonds, flat from January, and 5.1% for leveraged loans, slightly down from January’s 5.2%. The HY default rate remains in line with the non-recessionary average of 2.6%, while the leveraged loan rate continues well above its 2007–2025 average of 2.8%.”

Note, however, that the February default activity came mostly from lame-a$$ out of court sh*t:

“February’s total default volume across leveraged loans and HY was approximately $8.1 billion, split between $6.0 billion from four loan issuers and $2.1 billion from five HY issuers. Notable defaults include Vibrantz Technologies, with $3.3 billion in combined loan and bond defaults, and CSC ServiceWorks, which completed a $1.9 billion distressed debt exchange. Vibrantz’s liability management exercise, backed by over 90% of creditors, extended most of its debt to 2030 and provided $350 million in new funding. CSC ServiceWorks’ restructuring raised $115 million of new money but left the company with weak liquidity and high capital expenditure needs.”

Despite all of the doom and gloom out there, Fitch left its default forecast unchanged; it predicts leveraged loan defaults in the 4.5%-5% range and high yield defaults between 2.5%-3% — and that’s despite all of the noise around software.

For its part, S&P Global Ratings released its latest and greatest, citing (i) a decline in global corporate defaults to eight in February from ten in January, (ii) a YTD tally of 18 versus 17 at this point last year, (iii) deflated distressed exchanges — 44% YTD but wildly below the 71% at this same point in ‘25, and (iv) “[f]ive of the eight defaults in February were repeat defaulters that account for 50% of all year-to-date defaults, the highest share since 2020.”

For its part, Morningstar noted that “[d]efault activity among private credit, middle market borrowers has accelerated meaningfully over the past year, led by distressed exchanges resulting from material impairment of debtholders' interest. Over the last 12 months, 16 of 17 private credit rating downgrades to D (default) or SD (selective default) met our criteria for a distressed debt exchange, which we view as a default event. For comparison, we recorded nine downgrades to D/SD in 2024, including four distressed debt exchanges. We attribute the rise in distressed exchange situations to borrowers still struggling with declining revenue, weak operating margins, and a significant debt burden.”

Things could be even worse …

… but, as you all know, it’s raining PIK interest these days (not that, as Claude apparently notes, all PIK interest is created equal). The obvious upshot, LOL, is that literally nobody wants to file for bankruptcy anymore:* you all continue to cannibalize yourselves.

That said, there has been some recent action so let’s get into it 👇.

*This is a common refrain in BK circles … which is pretty dumb, candidly, because it’s not like people wanted to file for bankruptcy before. Remember something called “bankruptcy stigma”? We sure do.

⚡Update: Multi-Color Corporation⚡

It was never going to be easy, Mr. Bennett.

Back in early February ‘26, we covered the January 29th “prepackaged” filings of label-maker Multi-Color Corporation (“MCC”), MCC-Norwood, LLC (“MCC Norwood”), and fifty-four affiliates (collectively, together with MCC and MCC Norwood, the “debtors” and together with their non-debtor subsidiaries, the “company”) in the District of New Jersey (Judge Kaplan). From the second the petitions hit the docket, there was controversy over whether Newark was a suitable venue for these cases. You can catch up on that here 👇:

But you didn’t click the link, so to briefly recap, MCC-Norwood — an Ohio company with its principal place of business in Atlanta — served as the debtors’ hook to get into the Garden State. To create an argument, it opened a NJ bank account in December ‘25, which it funded on January 13, 2026 — sixteen days before the petition date — with $1.05mm of what had previously been somebody else’s cash.*

To put the money to work? No. It is the utilities’ adequate assurance account.

Given the obvious gamesmanship, the day after the petition date, a crossholder ad hoc group (the “crossholder AHG”), represented by Jones Day (home of the aforementioned Bruce Bennett), called bullsh*t and filed a motion to dismiss or transfer the cases .** The US trustee (the “UST”) got in on the action a couple weeks later too. The argument was dead simple: MCC-Norwood had other assets — twelve patents, AR, causes of action, and contract rights, each of which, to borrow from the crossholder AHG’s reply, “… existed for a greater portion of the 180-day period preceding the petition date than the newly funded bank accounts”*** and, for the 164 days prior to receipt of the bankruptcy-specific cash, constituted its only assets. Ergo, for at least 164 days, the debtors’ principal assets weren’t in NJ, so toss or move the cases.

The court found the position “… straightforward and logical ….”

That didn’t stop it, though, from giving both motions a …

LOL, c’mon, y’all, Judge Kaplan was never kicking the cases to another court. We wished the crossholder AHG good luck in its appeal in our first-day coverage.

You can read the 28-page, means-to-an-end opinion here (and the short-form order here), but to give you the gist, rather than apply a “straightforward and logical” analysis, the court opted for an “assets-based approach” under which you “… evaluate[] the assets that a debtor possesses at the time the petition is filed and where such assets were located …” for the longer portion of the 180-day period prior to filing.

That is, you decide “principal assets” one time — on the petition date, and after deciding MCC-Norwood’s patents, A/R, causes of action, and contract rights either couldn’t be ascribed a value under the record or had little to none, that left only the cash. The rest was a fait accompli.

Which begs a couple questions. Is that approach subject to extensive manipulation? Does it undermine the point of having a venue statute at all?****

Judge Kaplan agrees:*****

“The Court acknowledges that the Asset-Based Approach, to some degree, makes venue subject to manipulation.”

To some degree? It lets a debtor straight-up pick where it files. Don’t have sixteen days? Don’t worry, one should do the trick.******

After that, the interests of justice were dealt with. Simply too. You can’t just uproot cases after the court has … *checks notes* … “… entered a scheduling order; set confirmation timelines; supervised first-day relief; addressed several emergent motions; and invested judicial resources.” Good g-d, we wish that weren’t a quote detailing, uh, normal bankruptcy judge stuff? Here, where the lion’s share of it happened after the crossholder AHG’s motion had been docketed. Alas.

At a March 17, 2026 hearing,******* Mr. Bennett noted at the top that his group would be appealing, although, as of writing, a notice hasn’t yet hit the docket. He will need to act fast if he wants to avoid equitable mootness arguments.

Really fast. Because the debtors, an ad hoc group of primarily first lien debt holders, and equity owner/lender Clayton, Dubilier & Rice, LLC will push forward with their RSA-plan’s confirmation on March 31, 2026 at 10am ET.********

*On the same January date, the debtors opened a second NJ bank account and transferred $1k of the $1.05mm into it.

**On February 24, 2026, an hoc group of “excluded” first-lien lenders joined the crossholder AHG’s motion.

***See 11 USC § 1408(1) (“… a case under title 11 may be commenced in the district court for the district … in which the … principal assets in the United States, of the person or entity that is the subject of such case have been located for the one hundred and eighty days immediately preceding such commencement, or for a longer portion of such one-hundred-and-eighty-day period than the … principal assets in the United States, of such person were located in any other district[.]”)

****In the opinion, Judge Kaplan writes …

“… Debtors created a situation that enabled MCC-Norwood to file in New Jersey. To the extent this does not ‘sit right’ with the parties in interest, the Court shares that sentiment.”

… before using Congress’ “broad[] draft[ing]” as a scapegoat to effectively kill the venue statute.

*****The opinion then dove into hypotheticals about machinery in Kansas and Texas that, frankly, Johnny didn’t find all that compelling and don’t withhold scrutiny.

******As long as you used a pre-existing entity? That is, in essence, the distinction the court drew between these facts and Patriot Coal’s. Long-lived and/or dormant is apparently fine, but newcos ain’t.

*******March 17 was the first day of the final hearing on the DIP, which lasted ~7 hours and will carry over to tomorrow, March 23. The crossholder AHG is contesting the DIP because pre-filing it submitted a much superior DIP proposal … that the debtors immediately ignored. Regardless, we all know where it’s going to end in the bankruptcy court: final approval and another appeal.

********The plan classifies the crossholder AHG’s unsecured notes claims with the RSA-supporting 1Ls’ deficiency claims. Obviously an effort to stuff the ballot box, which, per the tabulation report, worked. We have no doubt Mr. Bennett will be objecting to that.

💥New Chapter 15 Bankruptcy Filing - Raízen S.A.💥

On March 12, 2026, Raízen S.A. ($RAIZ4) and eight affiliates (collectively, the “debtors” and together with their non-debtor affiliates, the “company”) filed chapter 15 cases in the Southern District of New York (Judge Beckerman), seeking recognition of their March 11, 2026-filed Brazilian recuperação extrajudicial proceedings (the “EJ”), which is, basically, the Brazilian version of a scheme of arrangement.