🥈Second Order Effects Are Real (Long #retailapocalypse Victims)🥈

We’ve spent a considerable amount of time discussing the possible and/or actual second order effects of disruption. For instance, waaaaaaay back in December 2016, we queried to what degree the scanless technology that Amazon Inc. ($AMZN) had then launched in its AmazonGo concept might affect grocers and quick service restaurants. We noted the following possibilities:

[Our] list of losers: manufacturers of conventional scanners...plastic separator bricks...cash registers...conveyer belts; landlords (maybe? - less square footage required without the cashier and self-checkout stations); print media/candy manufacturers/gift cards - all things that benefit from lines and impulse buys at checkout; human capital; people on the wrong end of income inequality.

Three years later, you don’t hear much about AmazonGo. Sure, it’s grown: there are now reportedly 20 locations with more on the way, but it hasn’t exactly taken the world by storm and caused mass disruption to either grocers or QSRs. It’s still worth watching though: the possible second order effects are countless.

An example of actual second order effects is Cenveo Inc., which filed for bankruptcy in February 2018. At the time we wrote:

…it's textbook disruption. Per the company,

"In addition to Cenveo’s leverage issues, macroeconomic factors, including the introduction of new e-commerce, digital substitution for products, and other technologies, are transforming the industry. Consumers increasingly use the internet and other electronic media to purchase goods and services, pay bills, and obtain electronic versions of printed materials. Moreover, advertisers increasingly use the internet and other electronic media for targeted campaigns directed at specific consumer segments rather than mail campaigns."

Ouch. To put it simply, every single time you opt-in for an electronic bank statement or purchase a comic book on your Kindle rather than from the local bookstore (if you even have a local bookstore), you're effing Cenveo.

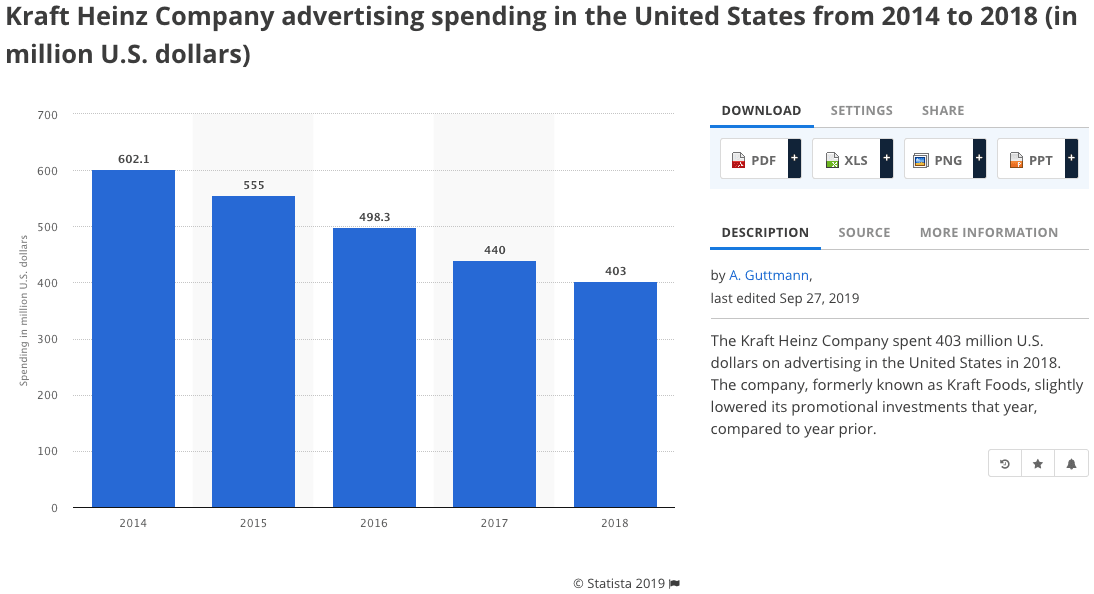

To close the trifecta, we’ll again highlight the recent pain in the SMA space. Catalina Marketing and Acosta Inc. both became chapter 11 filers while Crossmark Holdings Inc. narrowly avoided it. Why? Because CPG companies are taking it on the chin from new and exciting direct-to-consumer e-commerce brands, among other things, and have therefore shifted marketing strategies.

So, on the topic of second order effects, imagine being in the C-suite of a company that, among other things:

Prints signage, displays, shelf marketing and other promotional-print-material for brick-and-mortar retailers including the likes of, among others, struggling GNC Inc. ($GNC), Gap Inc. ($GPS), and GameStop Inc. (GME), all of which are shrinking their brick-and-mortar footprint;

Creates menu boards, register toppers, ceiling danglers and more for QSRs and fast casual restaurants who are competing with food delivery services more and more every day; and

Services consumer packaged goods companies by creating end cap promotions, shelf marketing, floor graphics and more.

Uh….YEAAAAAAAAAH. Some high risk exposure areas right there, folks.😬 And, so you’ve got to imagine that revenues of this “hypothetical” C-suiter’s company are declining, right? Particularly given that print is a highly competitive price-compressed industry?

Luckily, you don’t have to stretch the imagination too far.

LIKE THIS SO FAR AND WANT TO READ THE REST? YOU CAN, BY SUBSCRIBING TO OUR PREMIUM BI-WEEKLY KICK@$$ NEWSLETTER, HERE.