💥Serta Simmons: Another Failed Liability Management Exercise. Part VII.💥

Judge Lopez finally rendered his opinion after Fifth Circuit remand and dropped a bomb.

Holy hell, is the appellate process slooooooooooow.

If you recall, at the very end of ‘24 — a staggering 1.5 years ago — the Fifth Circuit took a massive pre-cyclospora deuce on the man formerly known as Judge Jones by unanimously reversing his decision that the June ‘20 liability management exercise (“LME”) performed by Serta Simmons Bedding (together with thirteen affiliates, the “debtors”) and certain favored lenders (the “favored lenders”) — funds managed by Invesco, Credit Suisse, Boston Management, Eaton Vance, and Barings — fit within the credit agreement’s “open market purchase” exception to pro-rata paydowns. We wrote about it then:

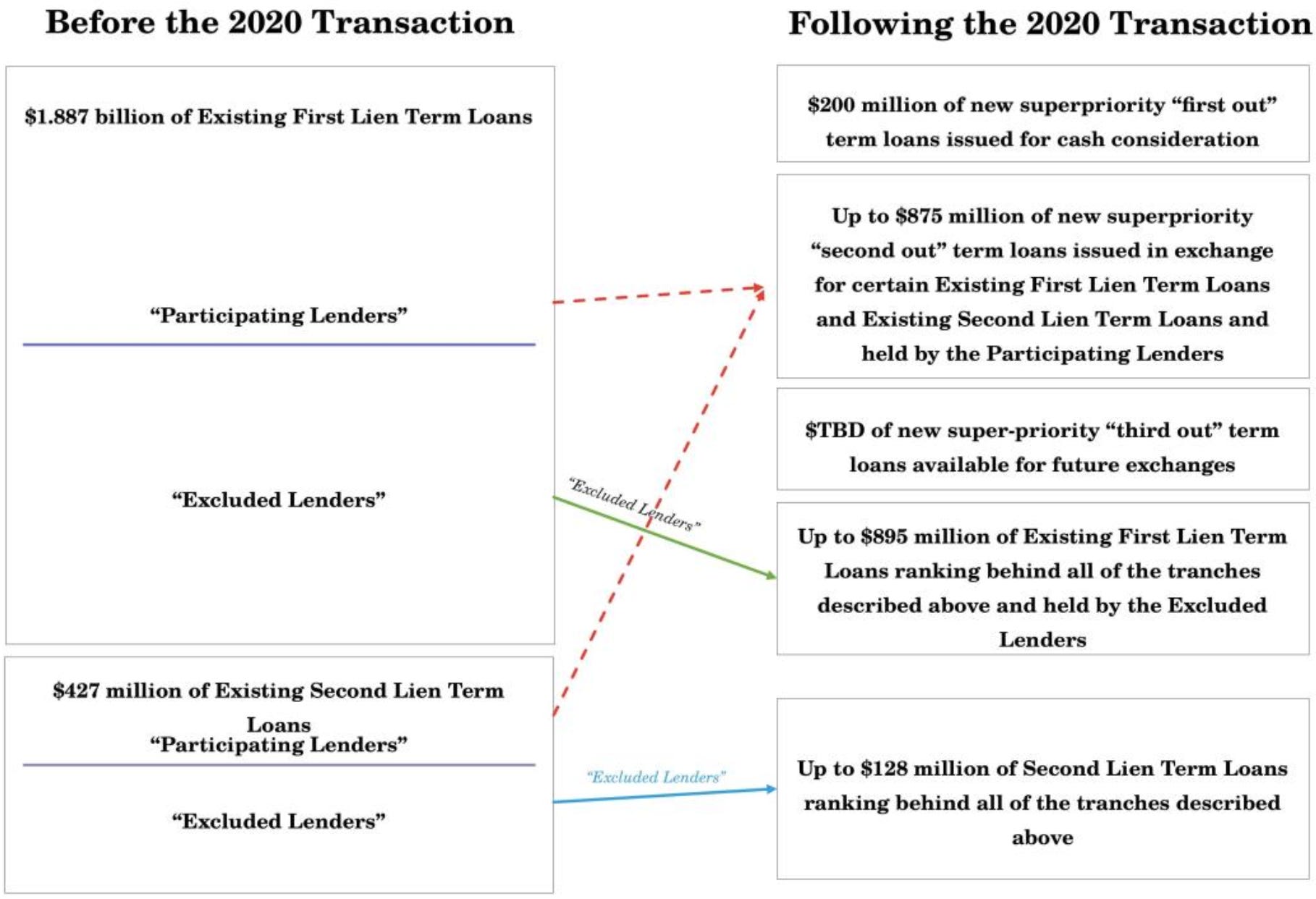

In short, the Fifth’s ruling meant the debtors’ post-LME structure 👇 was no bueno …

… and left the bankruptcy court — Judge Lopez now presiding — with two questions:

📍Did the favored lenders owe moolah to the excluded, minority lenders (the “excluded lenders”),* and

📍If so, how much?

On July 7, 2026 — another ~1.5 year wait, 😩 — we got our answer when Judge Lopez released a thick, 48-page opinion, the first page of which had the upshot …

“The question on remand is whether the lenders who participated in the liability management transaction—the Defendants—breached the credit agreement by receiving payments on their first-lien debt without purchasing participations in the loans held by the excluded first lien lenders—who are the Plaintiffs. The answer to this question is yes. Judgment is for the Plaintiffs.”

… before diving into a super-textualist analysis. We’d encourage you to give it a read. It was … the right answer? That didn’t kowtow to the debtors or the favored lenders.

What in the heck, Judge Lopez?

We mean, just take a look at this analysis:

“… the text of the Credit Agreement shows that the Participating Lenders received a payment within the meaning of § 2.18(c). Section 2.18(c) is designed to capture pro rata treatment for all consideration in respect of principal or interest on a loan. The Participating Lenders structured the 2020 Transaction as an attempted open-market transaction falling within an express carve-out under § 2.18(c). It didn’t work, so § 2.18(c) applies. Under the plain language of § 2.18(c), the Participating Lender received a payment and no other carve-out applies.”

Uncomplicated. Easy. All of which continued and, after disposing of equitable arguments,** was set out in plain English:

“The Participating Lenders received a payment in respect of their First Lien Term Loan without purchasing participations in Plaintiffs’ First Lien Term Loans. The payment the Participating Lenders received was on account of and in satisfaction of their First Lien Term Loan debt. The fact that the Participating Lenders exchanged their First Lien Term Loan at a discount is irrelevant. Section 2.18(c) focuses on whether the Participating Lenders recovered a greater proportion of their Loans than the proportion received by other Lenders. And they did. The Participating Lenders received a payment on their First Lien Term Loan. Plaintiffs received nothing.”

🙌.

You know what was simple? Damages. Well, simpl-y … brutal. To start, give the aforementioned section 2.18(c) a one-over:

“If any Lender obtains payment . . . in respect of any principal of or interest on any of its Loans of any Class held by it resulting in such Lender receiving payment of a greater proportion of the aggregate amount of its Loans of such Class and accrued interest thereon than the proportion received by any other Lender with Loans of such Class, then the Lender receiving such greater proportion shall purchase (for Cash at face value) participations in the Loans of other Lenders of such Class at such time outstanding to the extent necessary so that the benefit of all such payments shall be shared by the Lenders of such Class ratably in accordance with the aggregate amount of principal of and accrued interest on their respective Loans of such Class.”

Did you catch that parenthetical? The one that requires the comparatively better-off lender to “… purchase (for Cash at face value) participations …”?

Good. Judge Lopez did too. He applied it as written.

“The Participating Lenders and Serta structured a transaction that always had a risk of not complying with § 2.18(c), which means that having to pay face value for participations in distressed First Lien Term Loans to the Plaintiffs was always a possibility. The 2020 Transaction was structured to use the open market purchase exception under § 9.05(g) and parties proceeded without complying with § 2.18(c).[] Sophisticated parties accepted the litigation risk that came with it … The result of the decision is that, based on the record and applicable law, § 2.18(c) now applies. Damages viewed from that perspective is not absurd. It is what § 2.18(c) was designed to protect. Strict textual analysis was required to determine whether the 2020 Transaction complied with the Credit Agreement as an open market purchase without triggering any sacred rights. Now the text must be strictly applied when assessing damages.”

Giving the favored lenders a taste of their own medicine?

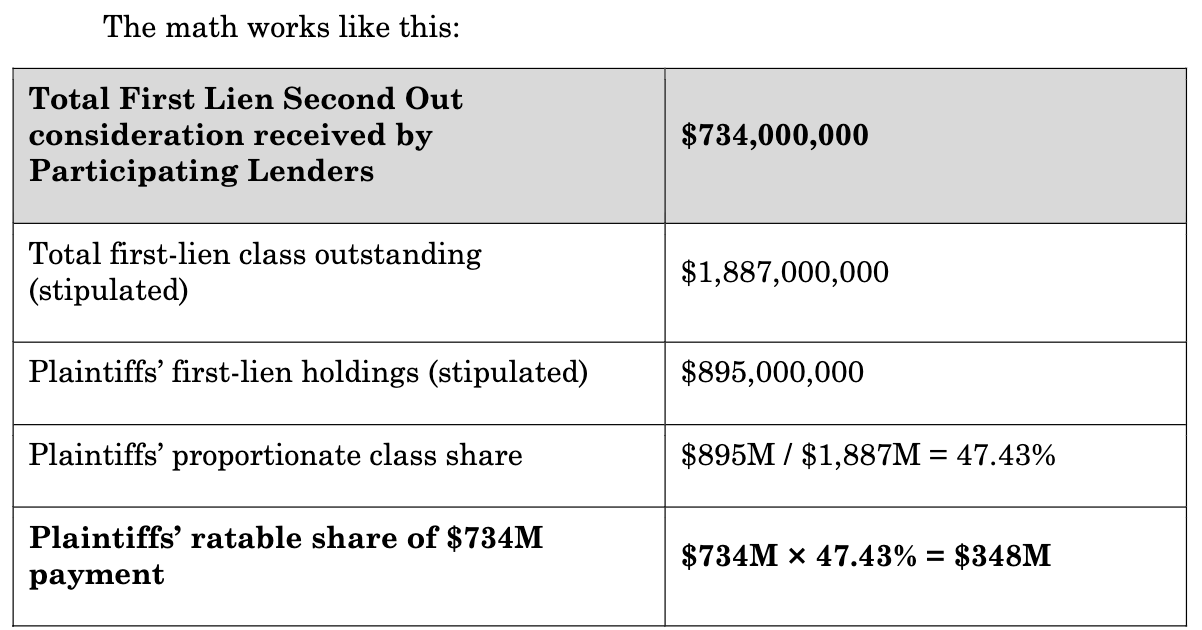

Here’s where we got charts. First up was its calculation of what the excluded lenders should’ve gotten — but didn’t get — in the exchange.

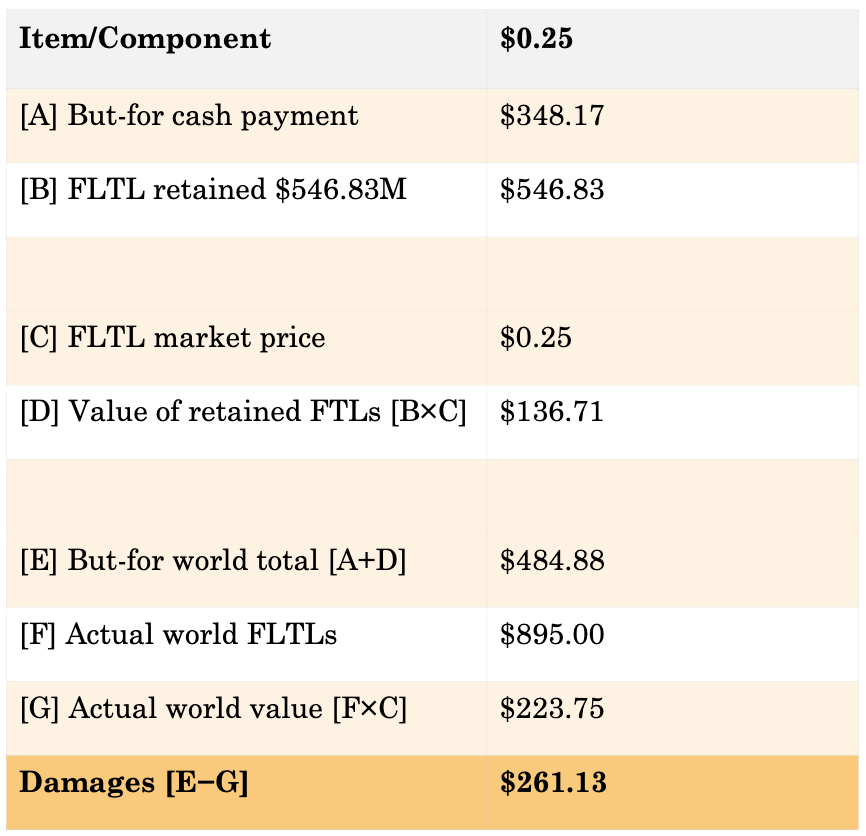

The court then paired that figure with another hypothetical: the amount in unexchanged first lien loans the excluded lenders would’ve retained had they been in the deal, aka ~$546.8mm (their full $895mm minus the $348mm above). On the date of the LME’s closing, the loans traded at 25c, so he tossed in a discount there, arriving at a total value of $484.88mm ($348mm + $546.8mm x 0.25).

From that, he deducted the excluded lenders’ real-world, never-exchanged loans, multiplied by the same discount, and voila, you’ve arrived at collective damages …

Here’s a live shot of the excluded lenders and their two-hundred-and-sixty-one million reasons to celebrate:

Meanwhile, the favored lenders be like …

… and looking over at Gibson, Dunn & Crutcher LLP, the favored lenders’ quarterback, like this:

That was before Judge Lopez’s kill shot. You see, the credit agreement contains a New York law provision, and prejudgment interest under NY law runs at a statutory 9%. Judge Lopez didn’t let anyone squirm out of it. From the second the LME closed until the opinion came down:

“This Court will not substitute the parties’ decision to have New York law govern disputes about the Credit Agreement without any applicable exceptions. Plaintiffs are awarded prejudgment interest at 9.00% per annum from June 22, 2020 through July 7, 2026.”

All in, the favored lenders are looking at a collective (but not joint) obligation in the neighborhood of … *gulp* … $400mm+.

Which takes us to some takeaways. The first one seems obvious:

As for others, the Patrick Walling, Joshua Sturm and William Brisman over at Proskauer Rose LLP hustled to provide this:

“The court sent a clear message: loan documents will be interpreted strictly in accordance with their terms and applicable law. Judge Lopez brushed aside every equitable argument … and addressed the dispute as a straightforward breach of contract claim governed by the plain language of the agreement. Opinions as to the fairness of the result — of the court, the parties, and the broader finance markets — were deemed irrelevant.”

For good reason, ioho. Sophisticated parties do be sophisticated. Separately, Vinson & Elkins LLP (“V&E”) scrambled to put this bit of “wisdom” out there:***

“● Lenders should account for potential liability and possibly significant prejudgment interest when evaluating transaction economics …

● Given the magnitude of the damages award and the significance of the legal issues, the ruling may be subject to appeal to the Fifth Circuit.”

Accounting for potential liability, huh? 🤞, you don’t need a lawyer to tell you to do that.

Anyway, we’ll peg the appeal as a certainty — even if this ends in settlement, as it likely will, there’s no reason for the favored lenders not to.

See you in another 1.5 years.

*The excluded lenders included funds owned or managed by Angelo Gordon, Ascribe, Columbia, Contrarian, Gamut, Apollo, Alcentra, and Z Capital. Which had some … 👇 … perplexed:

**Specifically, (i) an “unclean hands” argument focused on the excluded lenders having offered a competing, but rejected, LME and (ii) their failure to mitigate due to, you know, the practical absence of a market for their loans.

***If you’re thirsting for even more opinions, here is McDonald Hopkins LLP’s Scott Opincar throwing in his two cents. And here is the Creditor Rights Coalition offering a slate of views.

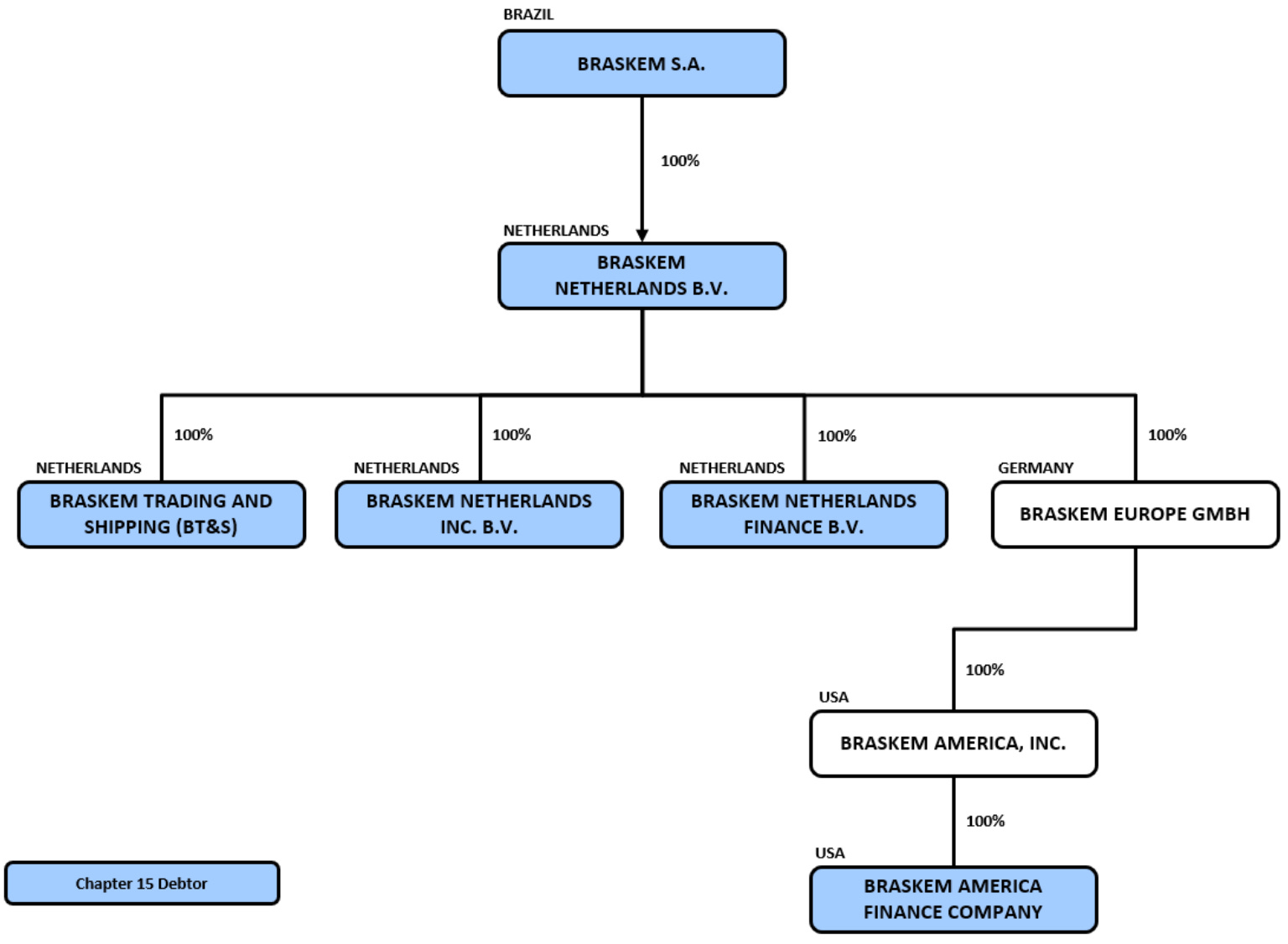

💥New Chapter 15 Filing - Braskem S.A.💥

Back on June 26, 2026, Braskem S.A. and five affiliates (collectively, the “debtors” and together with their non-debtor affiliates, the “company”) filed long-anticipated chapter 15 recognition proceedings through their foreign representative Antonio Reinaldo Rabelo Filho (the “foreign rep”) in the Southern District of New York (Judge Wiles). A growing trend!

The company is the Americas’ largest producer of thermoplastic resins and petrochemical products, servicing customers in over seventy countries, generating 80b+ BRL (or ~$15.5b) in net revenue in ‘24, and employing ~8k individuals, who, after July 5, 2026, were able to get back to focusing on work and less on soccer.

Low blow, we know.

In fairness, the Norwegians are a world-renowned powerhouse in the sport, 😂.

Anyway. Brazil is by far the company’s largest market, accounting for ~72% of that annual revenue ☝️. However, it’s a global player, and therefore, the company has to deal with global issues … like:

📍Market Downturn. A worldwide downturn in the petrochemical industry, which has been ongoing since ‘22 but really ramped up in ‘25 on account of ever-shrinking spreads. As a result, the company dropped its production in ‘25, and factories went from 72% utilization in ‘24 to 59% one year later. Net revenue joined in on the ride, declining 16% in 4Q’25 to ~$3.1b USD, and cash FLED the business — outflow increased 10x from ~$95.7mm in ‘24 to $1.13b in ‘25.*

📍Rock Salt Well Exploration. In ‘19, the Geological Survey of Brazil released a report linking the company’s rock salt well exploration in the Brazilian state of Alagoas to soil sinking in five neighborhoods of the city Maceió, which necessitated evacuations and the relocation of ~60k people. The company agreed to pay local authorities and, as of ‘25, had spent $2.7b+ USD on account of, as the foreign rep puts it, “… the geological event,” 🤣, with an anticipated $678mm USD to go.

📍 US-Iranian Relations. Here’s one we have and will be seeing; straight from Mr. Rabelo Filho’s mouth:

“… in early 2026, the Debtors began to face new financial and operational challenges due to the escalation of geopolitical tensions in the Middle East related to the conflict involving Iran and the United States. This conflict has driven up the price of oil and its derivatives, including naphtha—the main raw material in the petrochemical industry—directly impacting the Braskem Group’s production costs. Given the scale of the Group’s operations, even small increases in naphtha costs can result in billions in additional operating expenses. International freight rates have also risen substantially, affecting both raw material imports and international distribution costs, while trade route restrictions caused by the closure and blockade of the Strait of Hormuz have further disrupted operations and strained the Company’s financial condition.”

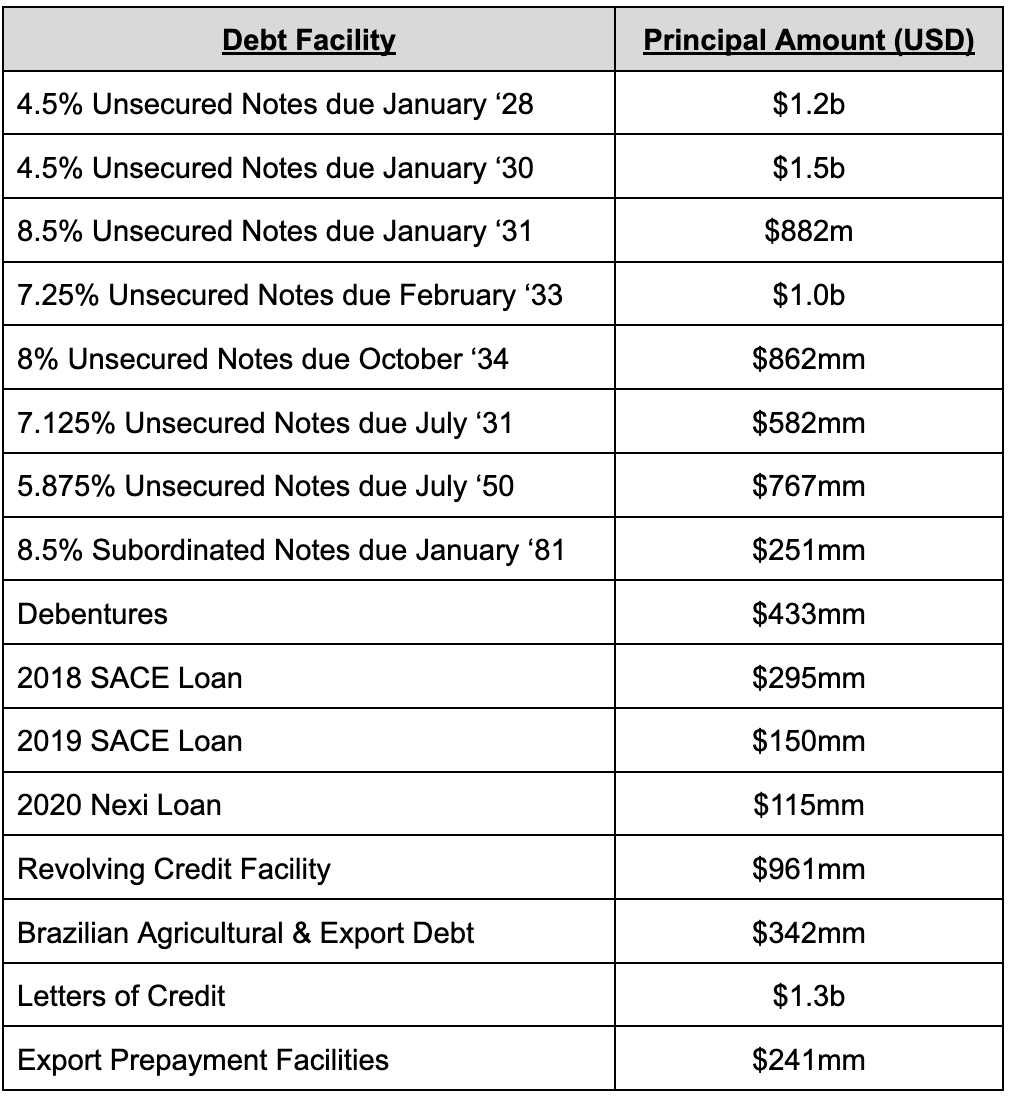

Of course, there are company-specific issues too. Namely, various interest and maturity obligations under funded debt — the straw that broke the camel’s back and which caused the company to file for a court-supervised mediation process in São Paulo on June 24, 2026 in anticipation of either a further Brazilian extrajudicial proceeding or a judicial reorganization. Here’s the ~$11b USD cap stack — most of which is pricing generally in the low 60s as of July 6, 2026:

The resolution of which we guess we’ll mark as “TBD.”

The company asked its creditors to extend credit lines and suspend collection efforts, but in its view, too few were interested.

Two creditor groups had their own take. The first is a Davis Polk & Wardwell LLP (“DPW”)-repped ad hoc group (the “AHG”), which chimed in with a simple reservation of rights decrying the company’s efforts. The AHG formed in the fall of ‘25 and has been clamoring for attention ever since, but the company “… only began any substantive discussion with members of the Ad Hoc Group this month …” — aka June ‘26 — “… and those interactions have so far been limited.”

Typical debtor bullsh*t — acting like 11th hour efforts count the same — but nothing out of the ordinary.

The second, composed of FFI Fund Ltd., FYI Ltd., and Olifant Fund, Ltd. (collectively, the “holders”) and represented by Paul Hastings LLP (“PH”), likely experienced the same. However, the holders didn’t just b*tch; they got us amped for a potential fight.

Sadly, 😩, via another reservation of rights. The foreign rep punted to the future by revising the proposed provisional relief order, 👎.

Anyway, here’s the meat. The company’s ‘41 notes were issued by debtor Braskem America Finance Company (“US FinCo”), which, per the foreign rep’s own words, is “… a wholly owned subsidiary of non-debtor, Braskem America, Inc. [‘Braskem Parent’]…,” “… was formed for the sole purpose of raising and managing funds on international markets to fund the activities of the operational components of the Braskem Group,” and “… is incorporated in Delaware and has its registered office in Wilmington, Delaware.”

Who benefited directly from the issuance? Why, non-debtor obligor Braskem Parent, another US entity with US headquarters, which, per the holders, is “… a solvent operating company that is not before this Court and is not a party to the Brazilian mediation proceeding.”

Therefore, they go on:

“Every objective indicator of US FinCo’s identity points to the United States: its Delaware incorporation; its direct Delaware parent’s headquarters in the United States; its only debt instruments being governed by New York law with a New York forum selection clause with an indenture trustee located in the United States; its assets consisting of intercompany claims against its United States parent.”

Followed by the kicker:

“… the Holders do not believe the Brazilian mediation proceeding—or any subsequent proceeding under Brazilian law—can or will be recognized with respect to US FinCo. The Holders reserve all rights to oppose recognition and to argue that any restructuring of US FinCo should proceed under Chapter 11 of the Bankruptcy Code, where US FinCo’s creditors would have the full protections of Chapter 11 bankruptcy law and the oversight of a U.S. bankruptcy court with jurisdiction over all property of US FinCo’s estate.”

Fun. Interesting too!

For another day though. On June 30, 2026, the court took up and granted then-uncontested provisional relief, and the recognition hearing won’t be happening until September 15, 2026 at the earliest. In the interim, Judge Wiles will hold a status conference on August 18, 2026 at 2pm ET.

The debtors are represented by E. Munhoz Advogados (Ana Elisa Laquimia) as Brazilian legal counsel, while the foreign rep is represented by Cleary Gottlieb Steen & Hamilton, LLP (Richard Cooper, Thomas Kessler, David Schwartz) as US legal counsel. The ad hoc group is represented by DPW (Timothy Graulich, David Schiff, Abraham Bane, Moshe Melcer) as US legal counsel. The holders are represented by PH (Daniel Fliman, Sayan Bhattacharyya, Robert Nussbaum) as legal counsel.

*EBITDA took a hit too. In 4Q’25, recurring EBITDA for the Brazil/South America segment fell 30% from the previous quarter to $143mm USD, while the US and Europe segment recorded, 😬, negative $32mm USD for the same period.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

📤 Notice📤

Adam Driedger (Associate) joined Latham & Watkins LLP from A&O Shearman.

Matthew Milana (Partner) joined Raines Feldman Littrell LLP from Reed Smith LLP.

Sean Monaghan joined King Street in its Cap Markets group from Ducera Partners.

🍾Congratulations to…🍾

DLA Piper LLP (James Muenker, Dennis O’Donnell, Roxanne Eastes, Rod Kazempour) for securing the legal mandate on behalf of the official committee of unsecured creditors in the U.S. TelePacific Corp. chapter 11 cases.

Houlihan Lokey Capital Inc. (David Hilty) for securing the investment banker mandate on behalf of the debtors in the GoldenPeaks Poland Holding Limited chapter 11 bankruptcy cases.

Orrick Herrington & Sutcliffe LLP (Mark Franke, Jacob Herz) and Morris James LLP (Eric Monzo, Jason Levin) for securing the legal mandate on behalf of an ad hoc group of equity holders in the Sangamo Therapeutics Inc. chapter 11 case.

Sherwood Partners on the firm’s combination with EisnerAmper.

😢Our Condolences😢

To the family, friends and colleagues of Lenard Parkins of Parkins & Rubio LLP.

🔥Hiring🔥

We’re seeking a freelance social media manager to give life to PETITION’s accounts on Instagram and potentially other platforms. The ideal candidate has experience managing social for a media brand or creator, is fluent in Canva and/or Illustrator, can adapt newsletter content into sharp, on-brand social posts (feed, stories, reels), and understands and enjoys financial storytelling. If you’re interested, please send your portfolio, relevant social handles, and a short note about your availability to petition@petition11.com.