💥New Chapter 11 Bankruptcy Filing - U.S. TelePacific Corp.💥

Frankenstein'd IT services co. stumbles into chapter 11 for sale or reorg

On June 28, 2026, Austin-based U.S. TelePacific Corp. and 11 affiliated debtors (collectively, the "debtors") — “national provider[s] of managed IT services spanning connectivity and networking, cybersecurity, communications, and information technology infrastructure services to business customers across the United States” — filed chapter 11 bankruptcy cases in the Southern District of Texas (Judge Perez). Why? Because even though the debtors Frankenstein’d this monstrosity 👇 over the last five-or-so years …

… they discovered that growing the balance sheet is easier than growing the business to service said balance sheet. Or as first day declarant and petition-date-appointed Chief Restructuring Officer Steven Shenker of Portage Point Partners (“Portage Point”) put it, “Although the Company is operationally profitable, growth in recent years did not generate the level of cash flow required to service the Company’s funded debt obligations while also maintaining the minimum liquidity necessary to operate its business.” 🙄.

We briefly covered this company back in early ‘22 — just before it went down the liability management path. Much has happened since then. Let’s get on with it.

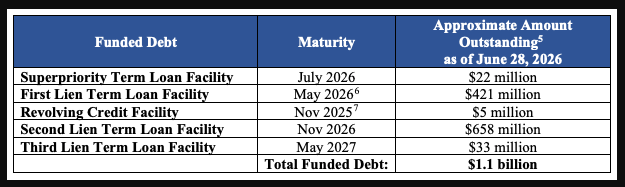

Shortly after our initial coverage, in February ‘22, sponsor Siris Capital Group (“Siris”) ignited $70mm by way of a growth equity investment while simultaneously the debtors refinanced their then-existing long-term funded debt, leaving them with, per Mr. Shenker, “… a term loan facility, in an initial [] principal amount of approximately $580 million and (ii) a revolving credit facility, in an initial aggregate principal amount of approximately $25 million …”

That ☝️ bought sixteen months. On June 1, 2023, the management of liabilities began; that day (i) the debtors offered to refinance 50% of the prior term loan and revolver into a new, super-senior first lien facility (the “first lien TL facility”) and (ii) Siris, through affiliates,* purchased the remaining 50% at some discounted value. Siris then subordinated its half of the debt to the other half and kicked in $65mm of fresh kindling, bundling both into a second lien facility (the “second lien TL facility”). As a kicker to incentivize participation, the debtors gave each participating lender a bonus too; each received a 5% gift of its holdings under the prior facility in the form of a third out facility (the “third lien TL facility”). Only one lender held out, which is why, despite the revolver having matured in November ‘25, there’s still $5mm outstanding under it in the chart above. It sits pari with the first lien TL facility.

The carving up on the cap stack bought the debtors and Siris, oh …

… about eighteen months. Big progress.

By early ‘25, the debtors’ insufficient growth was catching up to them. They engaged advisors — Sidley Austin LLP and PJT Partners LP (“PJT”) — and kicked off negotiations with an ad hoc group of first lien and third lien debt holders (the “ad hoc group”) and Siris. Time goes on, blah, blah, blah, strategic alternatives, blah, blah, “hard fought negotiations,” blah and in the fall of ‘25, the debtors default, a special committee of independents is formed (👋, James Gillis and Anthony Horton), and each tranche of lenders, including Siris as the lender under the second lien TL facility, gives a forbearance.

Nearly a year in, in December ‘25, the debtors and PJT go to market for a sale of the debtors’ assets. More forbearance followed, more independents joined to provide their critical independent thoughts (👋👋, David Aloise and Lloyd Sprung), although we have no idea why you’d ever need or want four.

Anyway. In March ‘26, the ad hoc group and Siris dropped more cash into the company to let its zombie-gait continue. This time, $20mm through a superpriority term loan facility (the “superpriority TL facility”).

Which brings us back to the sale process and Mr. Shenker:

“Following multiple rounds of engagement, the Company received 9 bids; however, the Company and its Advisors determined that none of such bids reflected terms that were sufficiently developed to proceed on an actionable basis at that time.”

Years of bought time — including over a year of strategery and professional fees — to wind up going into chapter 11 with a standard plan of action: a continued sale process and, if that fails, a debt-for-equity-swapping reorg with the ad hoc group and Siris, all subject to a restructuring support agreement supported by 98% of the first-lien holders, 100% of the second-lien holders (duh, it’s Siris), 88% of the third-lien holders, and “… 100% of the Company’s accounts receivable purchasers …,” which are also affiliates of Siris.

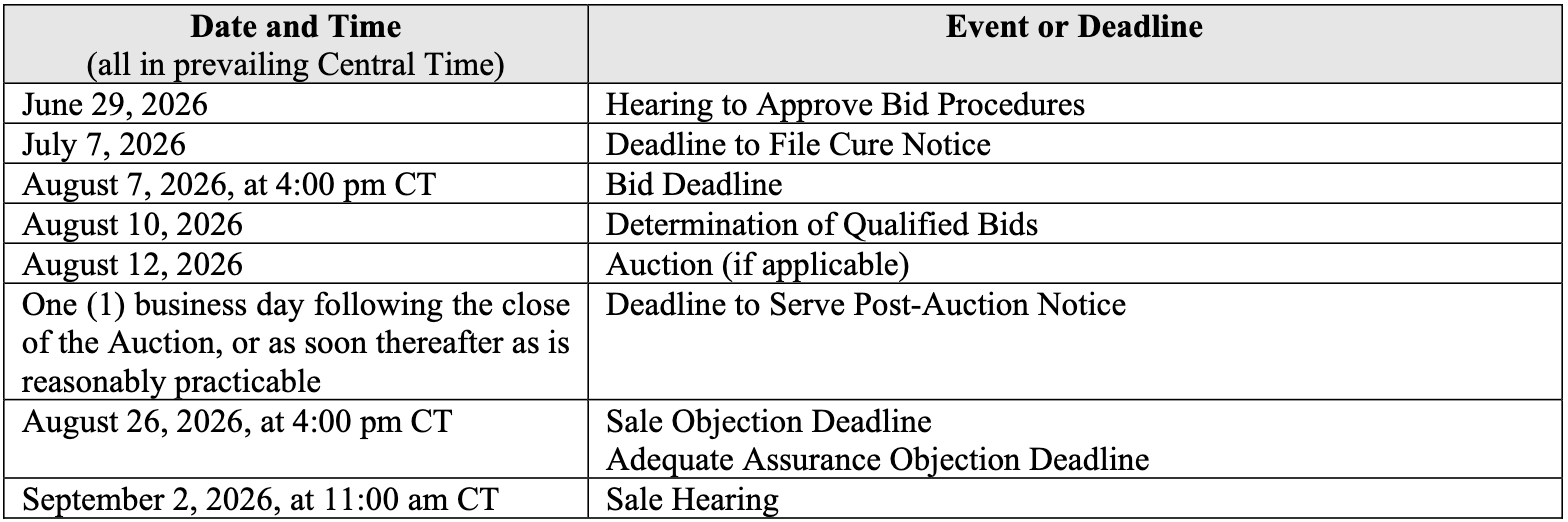

Here’s the sale timeline:

At any which point, the debtors can propose a stalking horse. Assuming they find one.**

If not, they’ll pivot to a pre-wired reorg.

Before we dip our toes into that though, we should address the DIP. It’s a very headline ~$73.5mm term loan facility, composed of (i) $20mm in new money ($10mm interim) and (ii) a ~$53.5mm in roll-ups, which itself bakes in (a) ~$34.7mm of the March ‘26 superpriority TL facility (all interim) (the “bridge rollup”), (b) ~$13.8mm in prepetition unpaid PIK interest on the first lien TL facility (all interim) (the “interest rollup”), and (c) $5mm in principal of the first lien TL facility (on final) (the “principal rollup”).***

Wait. We thought the debtors only owed ~$22mm under the superpriority TL facility?? It’s right there in their own chart ⬆️!

Yeah, the chart is not entirely accurate.**** Yes, there was $22mm in principal and interest, but the facility also includes a 1.75x MOIC, which the DIP is picking up. On interim.

Anyway, the reorg proposes to:

📍Convert the new-money DIP into a first lien exit facility,

📍Roll the bridge rollup into the same exit facility or pay it off with cash,

📍Convert the interest rollup into preferred tranche A shares in the reorg company (more on that below) or, less likely, push into the exit facility too,

📍Transform the principal rollup into exit facility debt,

📍Equitize the unrolled first lien TL facility and the stub revolver or give them some cash to splice up among themselves,

📍Chuck some warrants to holders of the second lien TL facility that, if exercised, would represent ~6% of the undiluted reorg common,

📍Wave a 🖕 to third lien and general unsecured claimants.

Which is fairly straightforward. Except where’s all the cash coming from?

It’s not the balance sheet. Instead, look over at the members of the ad hoc group and Siris, who, together, are providing new and old value for 14%-accruing, convertible preferred tranche A and B equity interests in the reorg debtors. Namely, $51.6mm in new money, the interest rollup, and only applicable to Siris, the contribution of ~$9.8mm of the accounts receivable it purchased from the debtors back to them.*****

That brings us back to the reorg and equitization of the prepetition debt. Recall how the unrolled first lien TL facility and the stub revolver are supposedly getting the reorg equity? Well, that’s on an undiluted basis, and the pref is about to throw a tsunami onto them. As-converted, the tranches represent ~80.3% of the reorg equity.******

The court held a one-hour, eighteen-minute first-day hearing on June 29, 2026 … which besides being longer than Johnny would’ve liked, went well enough. The court granted all requested relief and scheduled the second-day hearing for July 23, 2026 at 11:30am CT.

The debtors are represented by the aforementioned Sidley Austin LLP (Stephen Hessler, Anthony Grossi, Weiru Fang, Duston McFaul, Chelsea McManus, Jason Hufendick, Ryan Fink, Daniela Rakowski) as legal counsel, Portage Point (Steven Shenker, Scott Canna) as financial advisor, and PJT (William Evarts, Michael Cargo, Asher Eddy) as investment banker. The debtors’ slew of independent directors is composed of James Gillis, Anthony Horton, David Aloise, and Lloyd Sprung, and its special committee retained Katten Muchin Rosenman LLP as legal counsel. The ad hoc group is represented by Davis Polk & Wardwell LLP (Damian Schaible, Natasha Tsiouris, Michael Pera, David Kratzer; Kyle Kreider) and Haynes and Boone, LLP as legal counsel and Guggenheim Securities LLC as investment banker. Wilmington Savings Fund Society FSB, as agent under the — good lord — the superpriority TL facility, the first lien TL facility, the second lien TL facility, the third lien TL facility, and DIP, is represented by Goodwin Procter LLP (Andrew Goldman, Benjamin Loveland) as legal counsel.

*It does not matter at all, but for the curious, the affiliates are Tango Private Investments, LLC, Tango Private Holdings I, LLC, and Tango Private Holdings II, LLC.

**We won’t hold our breath, but if so, sale proceeds flow down a waterfall, except that if net proceeds exceed $200mm, 10% of the excess is shared with second lien holders, i.e., Siris.

***The DIP has a host of interest rates. The new money and bridge rollup are at SOFR + 1% cash or SOFR + 10% PIK, while the interest rollup’s is 1% cash and the principal rollup is SOFR + 1% cash or SOFR + 7% PIK. It also features a 2% PIK new money commitment premium and a 1.25x new money MOIC.

****Is the statement “… operationally profitable …” also a stretch? Because the DIP budget estimates a ~$4.2mm loss for the first 13 weeks of the cases. Before accounting for non-op expenses.

*****For which, they’re asking for a $3.7mm commitment fee. Either way, Siris’ contribution will definitely be used to justify a release.

******Tranche A is 75.1%, while tranche B is 5.16%.

Company Professionals:

Legal: Sidley Austin LLP (Stephen Hessler, Anthony Grossi, Weiru Fang, Duston McFaul, Chelsea McManus, Jason Hufendick, Ryan Fink, Daniela Rakowski)

Independent Directors: James Gillis, Anthony Horton, David Aloise, and Lloyd Sprung

Legal: Katten Muchin Rosenman LLP

Financial Advisor/CRO: Triple P TRS LLC aka Portage Point Partners LLC (Steven Shenker, Scott Canna)

Investment Banker: PJT Partners Inc. (William Evarts, Michael Cargo, Asher Eddy)

Claims Agent: Kroll (Click here for free docket access)

Other Parties in Interest:

Prepetition Superpriority Agent, Prepetition 1L Agent, Prepetition 2L Agent, Prepetition 3L Agent, and DIP Agent: Wilmington Savings Fund Society FSB

Legal: Goodwin Procter LLP (Andrew Goldman, Benjamin Loveland)

Ad Hoc Group

Legal: Davis Polk & Wardwell LLP (Damian Schaible, Natasha Tsiouris, Michael Pera, David Kratzer; Kyle Kreider) and Haynes and Boone, LLP

Investment Banker: Guggenheim Securities LLC