💥Welcome to Camp Catastrophe💥

Terra Property Trust, Inc. ($TPTA) + SIMAD Holdings, Ltd and DAMIS Holdings LLC

💥New Chapter 11 Bankruptcy Filings - SIMAD Holdings, Ltd and DAMIS Holdings LLC💥

On June 4, 2026, Trumbull, CT-based (i) SIMAD Holdings Ltd. (“SIMAD holdings”) and sixty affiliates (collectively, together with SIMAD holdings, the “SIMAD debtors”) and (ii) DAMIS Holdings LLC and eighty-nine affiliates (collectively, the “DAMIS debtors” and together with the SIMAD debtors, the “debtors”) filed separately-administered, equally-urgent chapter 11 bankruptcy cases in the District of New Jersey (Judge Gravelle for each).

The SIMAD debtors own and operator 30 summer camps around the US — eight day, 22 sleepaway — for ~20.5k kiddos per year. Each camp is separately branded and staffed and has a focus, be it sports, academics, art, tech, religion, etc. — the SIMAD debtors undoubtedly offer a camp your dude or dudette would dig, getting them out of the sweltering NYC heat (and your hair) for a couple of glorious weeks.

Meanwhile, the DAMIS debtors are in the business of multifamily properties, offices, hotels, and retail space.* Which is pretty far flung from summer campin’ but 🤷♀️.

So… why are we talking about the filings together?

For one, Cole Schotz PC (“Cole Schotz”) (Michael Sirota, Warren Usatine, David Bass, Felice Yudkin, Daniel Harris) filed each set. Which didn’t last. Within a week — presumably because of future conflict issues — it headed for the DAMIS debtors’ door and Faegre Drinker Biddle & Reath LLP (Michael Pompeo, Patrick Jackson, Ian Bambrick) stepped in as replacement counsel.

For two, they’re all affiliated. Both sets are 50/50 owned by brothers David and Michael Shabsels, who have also filed their own chapter 11 cases with the same court … and appear to have committed some light corporate theft.

No, it’s not express in SIMAD CRO Assaf Ravid’s first-day declaration or DAMIS CRO Perry Mandarino’s first … sh*t … he still hasn’t filed one.** Rather, Mr. Ravid provides key context clues:

“Prior to the Petition Date, SIMAD Holdings Ltd., a BVI Holding Company and the ultimate parent company of each of the SIMAD Debtors, raised bonds on the Tel Aviv Stock Exchange [‘TASE’] in December 2025 …

… The principal payments of the Debentures (Series A) were to be made annually on November 30 each year from 2026 through 2030. The interest of the Debentures (Series A) was to be paid semi-annually on May 31 and November 30 from 2026 through 2030. The SIMAD Debtors defaulted in making the first interest payment of the Debentures (Series A) due on May 31, 2026 …”

“Were to be made.” “Was to be paid.” You picking up on a theme? LOL, not a dime was ever paid, so Mr. Ravid goes on:

“As of the date hereof, the principal amount of the outstanding Debentures (Series A) is approximately $214 million using the exchange rate as of the Petition Date.”

Holly hell, that’s a nice chunk of change. The damage, however, wasn’t limited to bond debt. Two paragraphs later, Mr. Ravid tosses this in:

“In the weeks and months leading up to the Petition Date, the SIMAD Debtors became obligated on short-term loans (the ‘MCA Loans’) provided by approximately forty-two (42) merchant cash advance and short-term funders and lenders (the ‘MCA Lenders’). As of the Petition Date, the MCA Loans total in excess of $100 million in the aggregate.”

~$314mm incurred in the last seven months.***

In late May ‘26, Simad’s board disclosed to the Tel Aviv Stock Exchange that ~$34mm had disappeared into private businesses owned by the Shabsels. Obviously without authority. Apparently as the cash hit the debtors’ bank accounts, the bros be like:

So claw backs are def on the table. Probably more.

Without the cash, the SIMAD debtors couldn’t service the bonds’ May 31 interest payment, so the board did the natural thing and ordered the bros to repay it.

They agreed!

LOL, for a day!

Then they came back, said they didn’t have it and didn’t know when they would, making all campers be like …

… and giving us the chapter 11 petitions.

Per Globes, though, it seems the bros didn’t limit themselves to a one-time pilfering:

“It is not inconceivable that this is the tip of the iceberg. At the beginning of this week, Simad Holdings reported that besides the withdrawal of cash from the company the owners took on personal financial commitments ‘in significant amounts, secured on the assets and cash flows of the company’s subsidiaries.’”

That’ll take a bit, though. The debtors be wallowing in the process, and the cases have, understandably, been moving slow as sh*t as lenders/mortgage holders — and potential buyers — get up to speed. Sure, there’s been some progress — e.g., the eventually-consensual use of cash collateral and the SIMAD debtors received a $500k loan to keep one of their camps operating — but not a lot.****

Really, keeping the camps running has been the focus to date. Everyone wants it. By far most of all, Kirkland & Ellis LLP’s Joshua Sussberg, who seems to have forgotten he’s merely repping an ad hoc group of “… 20 of the camp directors/owners whose camps are part of these chapter 11 cases [] and Excelsior Camps, LLC” and showed up at a June 17 hearing with an entire first-day schtick and, 🙄, a deck(!) ready to rip.

And rip through that deck he did. For about fifteen minutes straight, where he enlightened us:

“… my life has been a function of what I learned at camp, and I put my camp resume together. It goes back a long time. I went to Camp Samoset. I started in 1988. I finished as a camper in ‘93. I was a counselor at Camp Samoset all the way through college, 1998.

I even had an opportunity to appear on a reality TV show on the Disney Channel, Bug Juice Season 3, where I was the director of a summer camp in New Mexico. And then my kids go to Camp Wayne, and I’ll explain why in a minute, and I’ve weaseled my way into coming up there each summer for four nights to referee color war.

And I say all that because, while I am not an expert in the camping business and the operations like many of my clients are, I do know how important it is and the traditions and the value, and you’ll see in that … color war picture when I had the privilege of being a general and the colors are maroon and gray and I wore a gray suit and the closest thing to a maroon tie that I could wear today, even if it doesn’t match…

Here are some pictures from my camping days with a lot of friends who still remain friends to this day. Even in those little pictures, notwithstanding that my cousin was in my bunk, I still speak to a lot of these people, and the relationships that you forge at camp last an absolute lifetime. Here’s a reference to the Bug Juice Season 3. I’m sure people can find a video out there online.”

We’re cutting him off there and sparing you the visuals, but you get the gist. Judge Gravelle said she found the spiel “… informational, ”😂. Inside, however, she was no doubt thinking this:

And here are live shots of the rest of the participants at the hearing, other than the fine folks at Cole Schotz:

Why is Cole Schotz excluded from the eyeroll extravaganza? Because they were all expending every ounce of energy to keep their eyes in place thinking, “hold it together, hold it together, we depend on this schtick-ster for business”:

The Zoom video itself may have even eyerolled … we’re not sure.

Anyway, those Bug Juice videos? Not even a challenge: Johnny found them in ~20 seconds.

Nice 💪, Josh.

Anyway, full case financing and bidding procedures will presumably make their way onto both dockets in due course — or mortgage lenders on the DAMIS side will move to foreclose. But we hope not. Notwithstanding Mr. Sussberg’s verbosity, we couldn’t agree with him more: the camps and the kids are the more important side of the endeavor.

On which, TBD. There aren’t any hearings on schedule at the moment.**** We’ll circle back to this one when it gets more interesting (aka somebody sue the Shabsels already).

The SIMAD debtors are represented by the aforementioned Cole Schotz (Michael Sirota, Warren Usatine, David Bass, Felice Yudkin, Daniel Harris) as legal counsel, FTI Consulting, Inc. ($FCN) as financial advisor, and their CRO and assistant CRO are Assaf Ravid and Daniel Sasson. The DAMIS debtors are represented by Faegre Drinker Biddle & Reath LLP (Michael Sirota, Warren Usatine, David Bass, Felice Yudkin, Daniel Harris, Ian Bambrick) as legal counsel and B. Riley Securities Inc. (Perry Mandarino) as financial advisor, investment banker, and CRO. Bernard Katz and Jill Frizzley are the DAMIS debtors’ independent managers. Mishmeret Trust Company Ltd. as bond trustee is represented by Chapman & Cutler LLP (Michael Friedman, Jorge Eric Coronel Hamilton, Stephen Richard Tetro II) and Riker Danzig LLP (Joseph Schwartz, Daniel Bloom) as legal counsel. The ad hoc camp committee is represented by Kirkland & Ellis LLP (Joshua Sussberg, Joshua Feltman, Joshua Greenblatt, Jeffrey Goldfine, Ciara Foster, Ravi Shankar, Robert Jacobson) and Duane Morris LLP (Morris Bauer, Drew McGehrin) as legal counsel. Prepetition secured lender First Financial Bank is represented by Blank Rome LLP (Regina Stango Kelbon, Matthew Kaslow) and Vorys, Sater, Seymour and Pease LLP (Kari Balog Coniglio, Carrie Mae Brosius) as legal counsel, while Mitchell Black and Camping Management Corporation is represented by another Blank Rome LLP team (Michael Schaedle, Josef Mintz, Lawrence Thomas III) as legal counsel. TriState Capital Bank is represented by Cullen and Dykman LLP (Kyriaki Christodoulou) as legal counsel. Bank of New Hampshire is represented by Mintz, Levin, Cohn, Ferris, Glovsky and Popeo, P.C. (Kaitlin Walsh, Donald Clarke, Megan Preusker) as legal counsel. Metropolitan Partners Group and related funds are represented by Pachulski Stang Ziehl & Jones LLP (Bradford Sandler, Robert Feinstein, Maxim Litvak), Wilentz Goldman & Spitzer PA (David Stein, Andrew Broome) and Polsinelli PC (David Karp, Brett Goodman) as legal counsel.

*It’s not a perfectly clean cut as between the debtors. For some reason, the SIMAD debtors own an office in NOLA.

**Which makes the debt stack less clear at those boxes. The petition lists $500mm-$1b in liabilities, and through resolved objections, motions to prohibit the use of cash collateral, and reservations of rights, mortgage lenders holding >$100mm in aggregate amounts have placed their gripes on the docket.

***To be clear, not all of the debt is sus. Certain of the SIMAD debtors owe ~$29mm to the Bank of New Hampshire, which they incurred in December ‘21 and July ‘23, and the SIMAD half of the sh*tshow has ~$2.7mm in general unsecured claims.

****Global also reports that Klirmark Capital is offering a $220mm DIP ($80 new money, the rest roll-up) and the hearing was supposedly going forward on Monday (June 22). As of writing, there’s nothing on the docket about any of that.

🔥On Shaky Terra: Terra Property Trust, Inc. ($TPTA)🔥

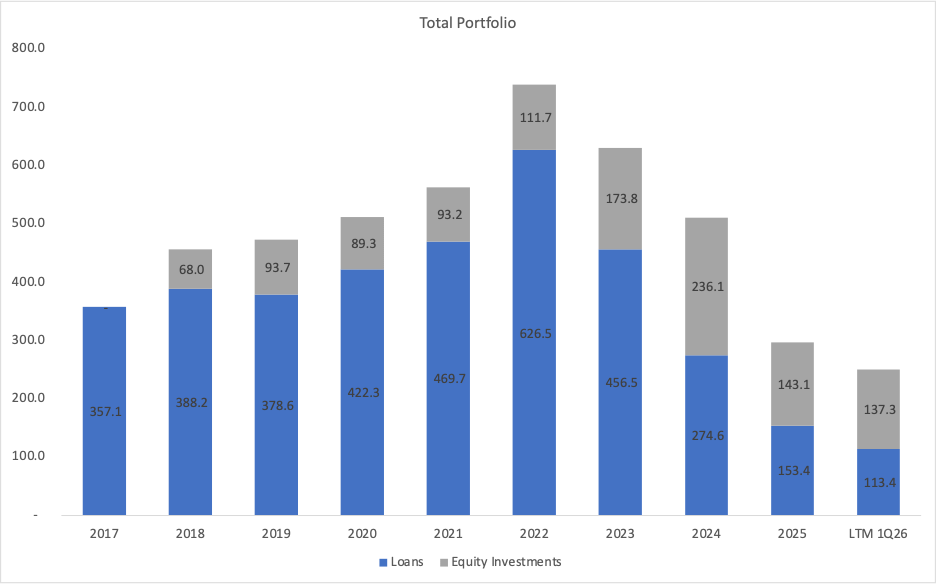

Terra Property Trust, Inc. ($TPTA)(“Terra” or the “company”) is an NYC-based REIT that invests primarily in commercial real estate; it lends into the middle market with $10-50mm checks up and down its target’s cap stacks. As of March 31, 2026, the company’s loan portfolio consisted of nine loans with a total carrying value of $133mm, split 49% into first mortgage loans, 23% into mezz, and 29% into pref equity. The real estate underpinning the loan portfolio is a mix of infill land (37%), office (33%), mixed use (20%), industrial (6%) and multifamily (5%) properties across California, Georgia, New Jersey, Arizona, New York and Massachusetts.

Terra’s equity portfolio, historically a much smaller proportion of its holdings, is now as large as its loan portfolio. As of March 31, 2026, it consisted of one industrial property in Texas and a multifamily property in California.

Before we get into what’s going on with the portfolio currently, let’s take a step back and discuss how we got here.

Bruce Batkin and Simon Mildé founded Terra Capital Partners (“TCP”), the company’s sponsor, back in ’01. Under its founders’ leadership, TCP could boast:

“In the lead up to the global financial crisis in 2007, believing that the risks associated with commercial real estate markets had grown out of proportion to the potential returns from such markets, Terra Capital Partners sold 100% of its investment management interests prior to the global financial crisis.”

The firm re-entered the lending market in July ’09, consolidated its existing funds into a REIT in ’16, and through June ’19, had not lost money on a single loan.

There was a changing of the guard in ’18, when Axar Capital Management L.P. (“Axar”) purchased TCP. Axar installed its real estate team at TCP, with Vikram Uppal taking the helm as CEO, a position he still holds. Mr. Batkin remained on the board for several years following the Axar sale, and his deputies, CFO Gregory Pinkus and Chief Origination Officer Daniel Cooperman have stayed in their roles to this day.

In ’21, Vikram Uppal via his own new firm, Mavik Capital Management, LP (“Mavik”), bought out Axar and became the sole owner of TCP. Blackstone Group Inc. ($BX) also took a 20% passive minority stake in Mavik via its secondaries group. Reporting from Bloomberg at that time noted that TCP had deployed more than $2.5b of capital since ’09 and generated a greater than 21% realized gross IRR.

But this is PETITION, so you already know that that praiseworthy performance did not hold up.

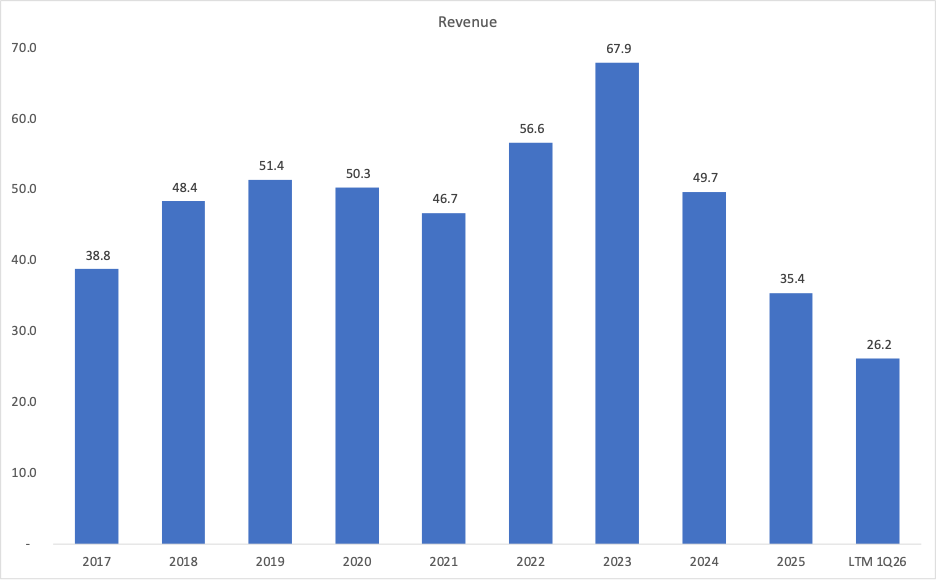

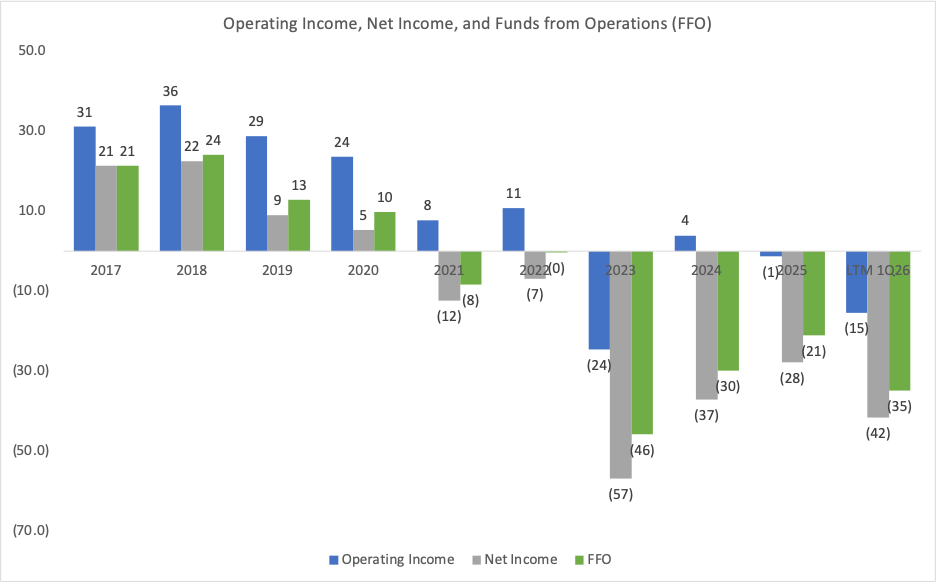

Terra’s revenues have steadily fallen since ’23, and earnings have been consistently negative. Terra’s portfolio has been shrinking over that period as well.

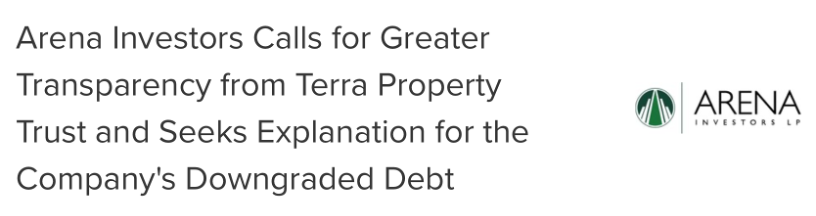

Terra does not disclose much more than high level stats about its portfolio and provides nowhere near enough detail to track the performance of individual investments.

We’re definitely not the first to complain about this lack of transparency either. Noteholder Arena Investors LP was alarmed by the explosion of non-performing loans in ’23 and ’24 and frustrated with Terra’s brush-offs:

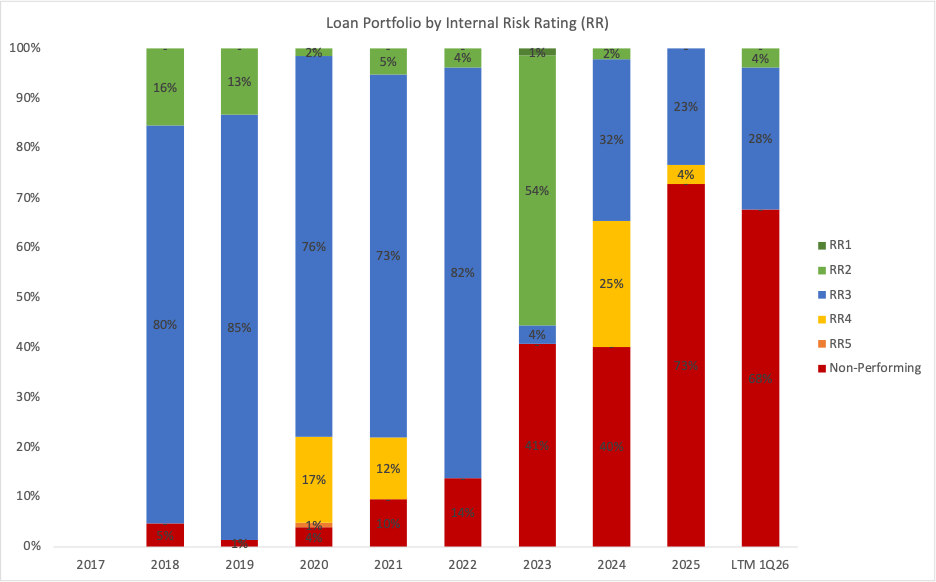

The information that Terra does provide shows that the proportion of the portfolio that is non-performing skyrocketed again in ’25.

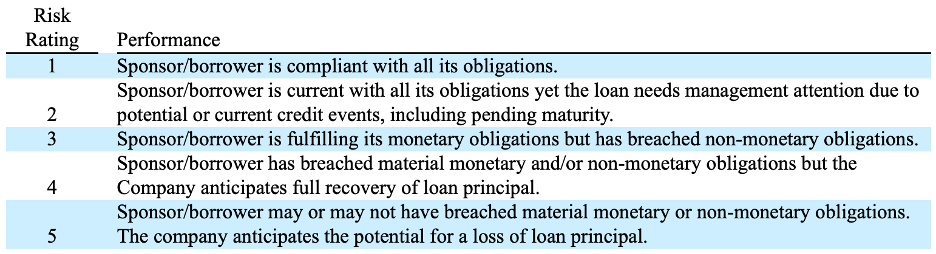

Terra assigns a risk rating to the “performing” loans in the portfolio from 1 to 5, and somehow never anticipates less than a full recovery of principal.

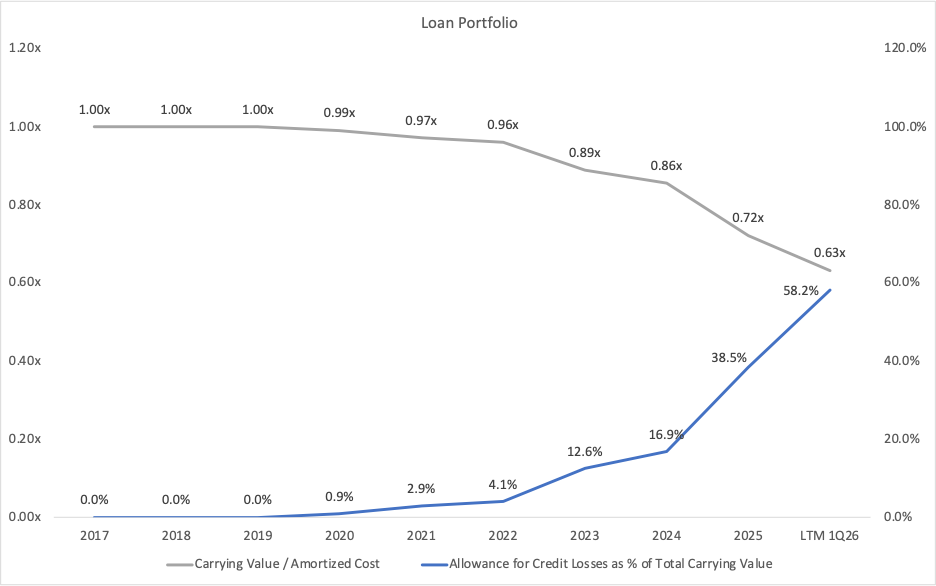

Even by its own marks, however, the value of the loan portfolio has been falling steadily and its allowance for credit losses has shot up.

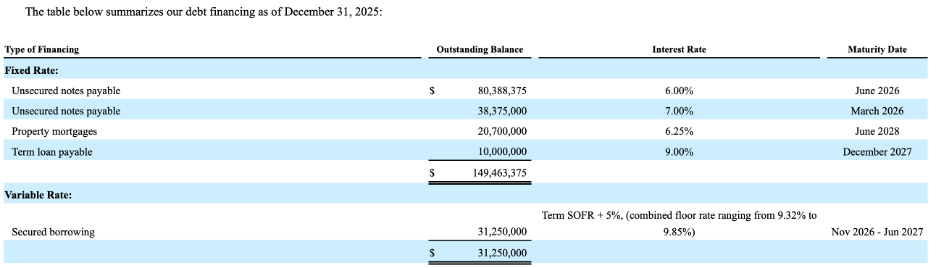

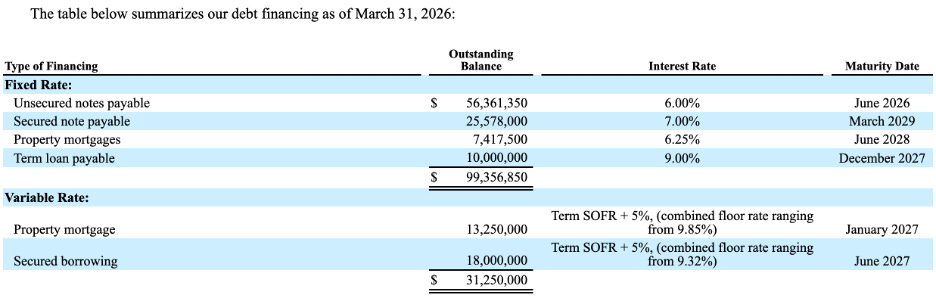

There is back-leverage too, of course. Terra ended the year with $180mm of debt outstanding, including $38mm of 7% senior unsecured notes due March ’26 (the “March ’26 unsecureds”) and $80mm of 6% senior notes due June ’26 (the “June ’26 unsecureds”).

In February ’26, Terra launched an offer to exchange any and all of the March ’26 unsecureds and the June ’26 unsecureds for new 7% Senior Secured Notes due ’29 at 100c on the dollar. Only $2mm of March ’26 unsecureds and $24mm of the June ’26 unsecureds took the company up on its offer. The company then paid off the remaining $36mm of March ’26 notes in full at maturity.

This left the company with only $5mm of unrestricted cash on hand as of March 31, 2026 and $56mm of bonds coming due in June. The full capital stack as of March was the following.

On May 8, 2026, Terra launched a second exchange offer, proposing to exchange any and all of the outstanding June ’26 unsecureds for a combination of new 8% senior secured notes due December ’28 (later moved forward to July ’27) and cash, split 80/20 between the new notes and cash for a total of 100c on dollar.

On June 10, 2026, the Company improved its offer, raising the proposed interest rate by 300bps (to 11% for those who cannot add) and moving the maturity date up six months. It also extended the deadline of this new and improved offer to June 25, 2026.

On Monday, June 22, 2026, Terra amended the terms of its offer again, increasing the cash portion of its offer from 20% to 25%. The updated offer will now expire on June 26, 2026 (Friday!).

In its announcement, Terra noted that some $36mm (66%) of existing noteholders had provided non-binding letters of intent regarding participation in the exchange. Without broader participation, the company expects to face $52mm of cash outflows over the next two quarters vs. only $47mm of inflows. Full participation in the exchange would bring that projected outflow down to $38mm. Terra also disclosed that it has lined up, but not officially secured, a $25mm 18-month 11% term loan from an undisclosed lender to cover the cash portion of the exchange or repay any existing notes.

Either way, something will have to give before the month is out. The June ’26 unsecureds mature on June 30, just four days after the expiration of the latest exchange offer.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

📤 Notice📤

Alexander Tate (Associate) has joined SierraConstellation Partners from Anderson Growth Partners.

Eva Marquis (Senior Associate) has joined SierraConstellation Partners from Atlantic Union Bank.

James Sprayregen (Partner) is reportedly joining Paul Weiss from Hilco.

Kyle Herman (Principal and Co-Founder) rejoined his old firm Exigent Partners LLC from Hilco Corporate Finance.

Michael Schneidereit (Partner) joined Gibson Dunn & Crutcher LLP from Jones Day.

Mitch Ryan (Senior Director - Business Development) joined Tiger Capital Group LLC.

🍾Congratulations to…🍾

Derek Pitts for joining Ensis Partners as a Senior Advisor.

Lowenstein Sandler LLP (Jeffrey Cohen, Gianfranco Finizio, Christopher Ward, Michael DiPietro) for securing the legal mandate on behalf of the official committee of unsecured creditors in the SiFi Networks America, LLC chapter 11 bankruptcy cases.

Lowenstein Sandler LLP (Jeffrey Cohen, Gianfranco Finizio, Eric Seltzer, Shanti Katona, Michael DiPietro) for securing the legal mandate on behalf of the official committee of unsecured creditors in the Simply Interior Homes, LLC chapter 11 bankruptcy cases.

Province LLC (Michael Atkinson) for securing the financial advisory mandate on behalf of the official committee of unsecured creditors in the CHS FL, LLC chapter 11 bankruptcy cases.

Province LLC (Paul Navid) for securing the financial advisory mandate on behalf of the official committee of unsecured creditors in the FreshRealm Inc. chapter 11 bankruptcy cases.

Womble Bond Dickinson LLP (Wojciech Jung, Edward Schnitzer, Todd Atkinson) for securing the legal mandate on behalf of the official committee of unsecured creditors in the GoldenPeaks Poland Holding Limited chapter 11 bankruptcy cases.