💥The Prepack Ain't Prepacking💥

Plus updates: West Marine Inc. + Xerox Corporation ($XRX) + SIMAD Holdings Ltd./DAMIS Holdings LLC.

Let’s dive into the big recent chapter 11 filing and get into some updates. LFG!

💥New Chapter 11 Bankruptcy Filing - DISH DBS Corporation and DISH Wireless L.L.C.💥

What even is a “prepack”? At one point, Johnny thought he knew — a filing that was expected to go smooth as butter on account of prebaked widespread support.

More and more though, he isn’t sure.

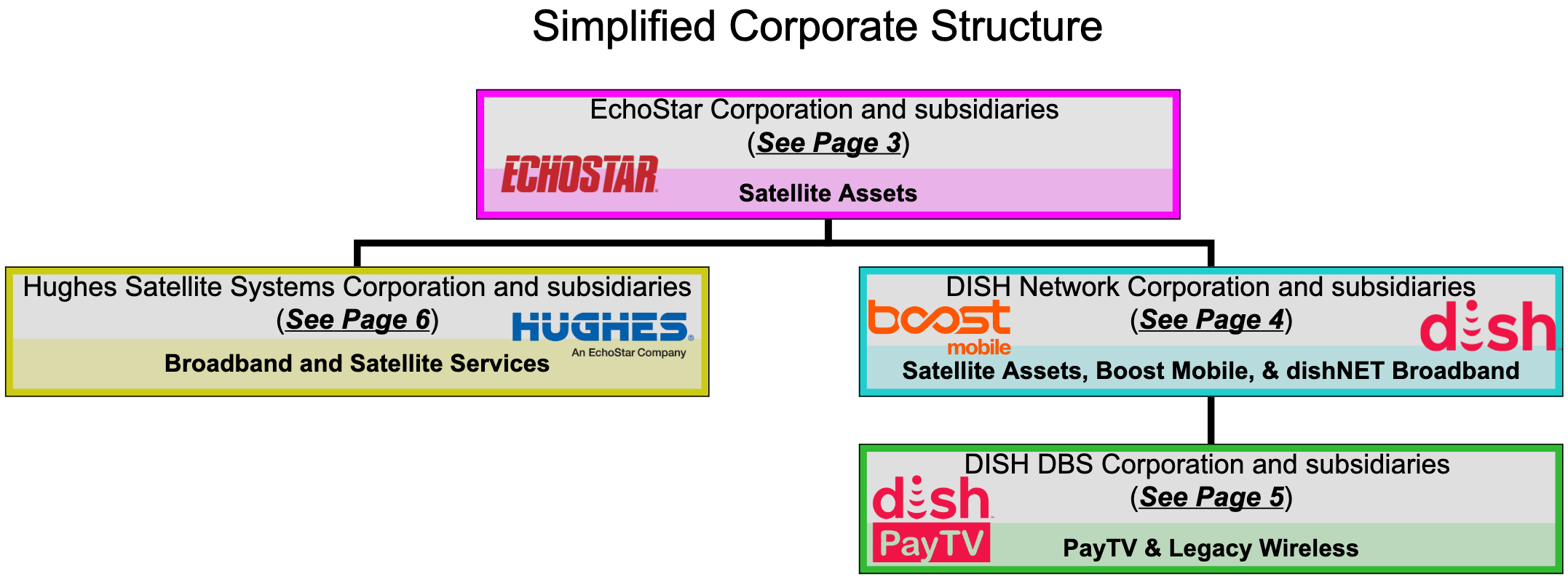

Case in point. On June 30, 2026, EchoStar Corporation ($ECHO)-owned, Englewood, CO-based DISH DBS Corporation (“DBS”), DISH Wireless L.L.C. (“DWLLC”), and sixteen affiliates (collectively, together with DBS and DWLLC, the “debtors” and together with their non-debtor affiliates, the “company”) filed chapter 11 bankruptcy cases in the Southern District of Texas (Judge Lopez).

Cases, which, debtors’ counsel White & Case LLP (“W&C”) says are prepackaged. Here’s the plan and here’s the disclosure statement.

We’ll assume some familiarity with the company. It’s a well-known pay-TV, wireless, and internet service provider, and the debtors constitute two of its business segments. That is, DWLLC and four debtors (collectively, the “wireless debtors”) built out (PETITION NOTE: key tense there) the company’s nationwide 5G mobile network infrastructure following its antitrust-driven acquisition of Sprint Corporation’s Boost Mobile in ‘20. All in, the company dumped ~$46b into that op before, following an “… unusual …” — first day declarant and COO John Swieringa’s words — investigation by the US Federal Communications Commission (the “FCC”) in spring ‘25, (i) agreeing to sell its spectrum to AT&T Mobility II LLC (“AT&T”) and Space Exploration Technologies Corp. ($SPCX) (“SpaceX”) for ~$42b, a figure roughly $12b more than the company paid for the spectrum, and (ii) calling a FCC-inspired force-majeure event under its agreements under its tower leases and infrastructure and vendor agreements, which in turn prompted lawsuits to rain down. Now, those entities don’t operate.

Meanwhile, DBS and its subsidiaries (collectively, but excluding the wireless debtors, the “DBS debtors”) do. They run the TV segment, including Sling TV,* and with respect to those entities, we agree with W&C. This is a prepack. After two+ years of litigation relating to a liability-managing, asset-shuffling transaction,** they hammered out a restructuring support agreement (the “RSA”) in March ‘26 — you know, 3-ish months before the petition date — with an ad hoc group of the DBS debtors’ funded debt holders (the “ad hoc group”), represented by Milbank LLP and Lazard Frères & Co. ($LAZ).

Importantly, the DBS debtors and the wireless debtors have wholly-different capital structures. DBS has that third-party funded debt ☝️, and had they filed on their own, the DBS debtors would fly through chapter 11. In fact, no one on that side of the house is even taking a haircut. The notes will be amended and paid in full, and every other class — including general unsecured claims — will pass through the bankruptcy unimpaired.

Easy peasy. In principle.

Unfortunately for the ad hoc group, the DBS debtors filed alongside the wireless debtors, which aside from intercompany “loans” (discussed 👇), are burdened by contingent creditors — i.e., litigants in the lawsuits demanding billions in damages, which the company disputes. AKA there’ll be a lot of painful, long-lived bankruptcy litigation.

So, no matter how hard W&C’s Tom Lauria floats around the term “prepackaged,” the wireless debtors’ cases are not. Hearing length illustrates that. In a real prepack, everybody’s singing kumbaya and praises abound — the hearings are damn quick and (mostly) efficient. As they should be.

The debtors’ July 1, 2026 first day hearing was not that. It ran — holy hell — ~3.5 hours …

… which still wasn’t enough.

July 8 served as the second first-day hearing, which ran another three hours. For an aggregate 6.5 hours of judicial oversight to get standard-a$$ first-day relief.

Relief that, btw, did not include the debtors’ emergency ask for conditional approval of the DS.

LOL, “prepack.”

Now seems a good time to introduce the disruptors. They’re Crown Castle, repped by Paul, Weiss, Rifkind, Wharton & Garrison LLP (“PW”), American Towers LLC and its affiliates, repped by Ropes & Gray LLP, and DPI Retail, GGP Services Inc., Landmark Dividend, and LBA Realty, LLC, repped by Allen Matkins Leck Gamble Mallory & Natsis LLP and Kelley Drye & Warren LLP, each of which were burned by the force-majeure call. They sure as sh*t ain’t signed off on the plan with respect to the wireless debtors. To illuminate, here’s PW’s Brian Hermann:

“The [wireless debtors’ path], to be fair, is a freefall Chapter 11 through which the DISH Wireless Debtors will liquidate and its creditors are projected by DISH to receive 1 to 2 cents on the dollar. I take issue with Mr. Lauria’s characterization of that as a classic prepack. Unsecured creditors who were not spoken with during the two years that the company has been moving assets around and doing all kinds of things to restructure, are our client and I think the creditors that are similarly situated to our client have not been spoken with about the restructuring and this is not a prepack.”

LMAO, a “prepack” lacking key creditor input, 🤣.

Wait, somebody had to have been solicited, right? Oh, somebody was. Back to Mr. Hermann:

“… as you heard, Mr. Lauria would like to carry the class of unsecured claims [at the wireless debtors] with an inter-company claim that was possessed up until recently by an insider affiliate. That’s an $8.8 billion claim that resided at DISH Network Corporation that they then transferred to DBS, and then they inexplicably transferred to a trust for the benefit of creditors who are otherwise being paid in full under the DBS Plan.”

The company calls that claim a loan, but PW clearly intends to put it under the microscope. The company documented the “loan” in August ‘25 for amounts “borrowed” by the wireless debtors dating back to ‘20 and, even though the company trades publicly, never reported it. Anyway, Mr. Hermann goes on:

“Your Honor, while I don’t know this to be true sitting here today because I don’t have access to discovery, I can say pretty confidently that this is a contrived mechanism to take what is an insider claim and give it the appearance of a third party claim.”

Yeah, that sounds right, Mr. Hermann. “Prepack.”

Johnny’s starting to experience semantic satiation.

Anyway, what exactly is driving ECHO’s decision-making here? Simple. We’ll point you to the $42b sale of spectrum and go back to Mr. Hermann one last time:

“I would point out that that’s $12 billion more than they paid for the spectrum only five years earlier, so they did so at a substantial profit. And candidly I think what the DISH Wireless case is all about is how much of that can they keep for themselves, so how much can EchoStar’s non-Debtor keep, as opposed to having to share it with the creditors of DISH Wireless.”

Now we get it. Even though its approach to the plan is “novel,” ECHO intends to effectuate that outcome without reinventing the wheel. It has a $300mm stalking horse 363 bid set up for the wireless debtors’ assets,*** including, duh, claims against ECHO and its affiliates, offset by a credit bid of ECHO’s proposed $85mm wireless debtor DIP.****

The debtors will take a shot at that DIP, the DS motion (again), and less controversial second-day relief on July 23 at 9am CT, followed by a vote estimation motion for the disruptors and SBA Telecommunications, LLC in mid-August.

We’ll be sure our 🍿 is good and buttered for both.

The debtors are represented by W&C (Thomas Lauria, David Turetsky, Samuel Hershey, Andrea Amulic, Matthew Linder, Laura Baccash, Ronald Gorsich, Doah Kim, Charles Koster) as legal counsel, FTI Consulting, Inc. ($FCN) as financial advisor, and FCN-affiliate FCN’s FTI Capital Advisors, LLC (Glenn Tobias, Douglas Edelman) as investment banker. The debtors’ special committee is composed of Gerard Uzzi and Vikram Jindal and is represented by Dentons US LLP (Van Durrer II, David Shim) as legal counsel. The ad hoc group is represented by Milbank LLP (Dennis Dunne, Lisa Laukitis, Abigail Debold, Andrew Leblanc) and Howley Law PLLC (Tom Howley, Eric Terry) as legal counsel and LAZ as investment banker. Crown Castle is represented by PW (Brian Hermann, Kyle Kimpler, Jeffrey Recher, Grace Hotz) and Porter Hedges LLP (John Higgins, M. Shane Johnson, Megan Young-John, Jack Eiband) as legal counsel. American Towers LLC is represented by Ropes & Gray LLP (Daniel Forman, David Hennes, Andrew Todres, Casey Kyung-Se Lee, Margaret Alden, William Roberts) and Hunton Andrews Kurth LLP (Tad Davidson II, Ashley Harper, Philip Guffy) as legal counsel. DPI Retail, GGP Services Inc., Landmark Dividend, and LBA Realty, LLC is represented by Allen Matkins Leck Gamble Mallory & Natsis LLP (Ivan Gold) and Kelley Drye & Warren LLP (Robert LeHane, Jennifer Raviele, Charles Fendrych) as legal counsel. ECHO is represented by Morris, Nichols, Arsht & Tunnell LLP (Robert Dehney, Sr., Eric Schwartz, Matthew Harvey, Daniel Butz, Sophie Rogers Churchill, Luke Brzozowski) as legal counsel. SBA Telecommunications, LLC and its affiliates are represented by Akerman LLP (Lucian Murley, Laura Taveras) as legal counsel.

*These really are distinct businesses too. In ‘25, the DBS debtors booked operating income of $2.4b on revenue of $9.7b. Compare that to the wireless debtors, which in ‘24 — their last full year of operation — brought home negative $477mm in operating income on revenue of $3.6b.

**Here’s the gist of the January ‘24 LME, courtesy of Milbank’s Dennis Dunne:

“In January of 2024 DISH DBS moved a substantial amount of our collateral and other value out of the DBS obligor’s on our debt, specifically DBS transferred 4.7 billion of intercompany loan receivables to a wholly owned subsidiary of EchoStar for zero consideration, they transferred 3 million DISH TV subscribers to a newly formed unrestricted subsidiary and they designated its Sling TV subsidiaries as unrestricted subsidiaries thereby placing the Sling TV business beyond the reach of the DBS bond holders.

In addition, DBS effectuated a series of cash advances from DBS to DISH Network totaling over time more than $2 billion. Around the same time DBS launched an exchange offer for the bonds, the exchange offer was priced at what we believe were unattractive levels. Our group entered into a cooperation agreement and the exchange offer failed and was ultimately withdrawn.”

Defeat notwithstanding, the company didn’t return the assets to DBS, so the ad hoc group sued.

***Which doesn’t carry any bid protections.

****The DIP isn’t up for hearing yet. DWLLC has sufficient cash to trudge along, so the debtors put the DIP on ordinary notice. The would-be DIP proposes to pay 11.5% PIK interest and has no fees. It’s also proposed to be subordinate to an April ‘26, $75mm DBS-to-DWLLC secured loan, which we assume Mr. Hermann will also be scrutinizing.

🚤Update - West Marine Inc.🚤

Back on May 17, 2026, West Marine, Inc. and seven affiliates, retailers of, among other things, boating supplies, fishing gear, marine equipment (collectively, the “debtors”), filed prearranged chapter 11 bankruptcy cases in the District of Delaware (Judge Owens). The upshot of the filing was that the debtors had a restructuring support agreement (the “RSA”) with substantial support from (most) parties in interest and that the restructuring would dramatically reduce leverage …

… by, among other things, equitizing that there 👆 ‘28 term loan facility held by a variety of sophisticated lenders. There was — as one might expect from a Kirkland & Ellis LLP (“Kirkland”) RSA — a toggle option, about which we wrote the following:

This, we should note, was the continuation of a tepid marketing process pre-petition, during which Portage Point had reached out to five potential purchasers.

So? Was our skepticism warranted?

It appears so. Seems the debtors drew scant interest.