💥The Canary?💥

The One Big Beautiful Bill Begets Two Big Beautiful Bankruptcies + More.

Today we discuss, among other things, two recent chapter 11 filings. But make no mistake: both bankruptcy activity and liability management action remain depressed, even if there are some small signs that things could pick up.

For one thing, here is Bloomberg with a report that liability management exercises, after a YOY lull, are on the verge of a relative comeback:

“A growing number of companies are trying to negotiate out-of-court deals that reshuffle repayment priorities, extend due dates and coax lenders to provide a fresh injection of cash. That allows their private equity owners to preserve money and keep their options open.

‘There is a bit of a K-shaped market for companies facing 2028/2029 maturities,’ said Damian Schaible, co-head of restructuring at Davis Polk & Wardwell. ‘Companies facing near-term maturities seem to be divided into easy refinancing stories and tougher ones.’

There were almost 50 LMEs globally in 2024 before dropping to fewer than 35 last year, according to data compiled by Bloomberg. But these transactions are picking up again as lenders exploit loose credit documents and assert themselves. While only seven LMEs were completed in the first quarter, nine more could commence soon, the data shows.” (emphasis added)

The article goes on to cite (i) Medical Solutions, a healthcare staffing firm owned by Centerbridge Partners LP and Caisse de Depot et Placement du Quebec, (ii) Platinum Equity-owned Cabinetworks, (iii) L Catterton-backed RealTruck Group, (iv) publicly-traded Vivid Seats Inc. ($SEAT, see more below) and (v) Clearlake Capital and Francisco Partners-backed Perforce Software, as participants — some active, some recently completed — in the LME realm.

Not cited, but reported on elsewhere in the Bloomberg universe, was (a) CDK Global, a Brookfield Business Partners software-to-car-dealerships provider, whose creditors have signed a cooperation agreement to get out ahead of any potential debt deal and (b) West Marine Inc., a boating-supply and fishing-focused retailer owned by Oaktree Capital Management and L Catterton that finds itself teetering just a few years after an earlier liability management deal but is, more likely than not, out of out-of-court options and headed for a bankruptcy court near you.

For its part, Pitchbook noted the following:

“While the headline [leveraged loan] default rate remains relatively contained, at 1.43% as of March 31, the distress ratio — the share of loans priced below 80 cents on the dollar — climbed to 7.23% by month-end, its highest level since December 2022. And in an LCD survey of market professionals conducted in March, 92% of respondents said they expect default levels to increase at least slightly over the next six months, up sharply from 67% in December.”

The fine folks there go on to point out that the 7.23% distress ratio cited ☝️compares to 4.34% at the end of ‘25; they note further that the dual-track default rate including LMEs is 3.48%, “...more than double the payment-only rate, another reminder that liability management exercises are doing significant work to keep formal defaults suppressed.”

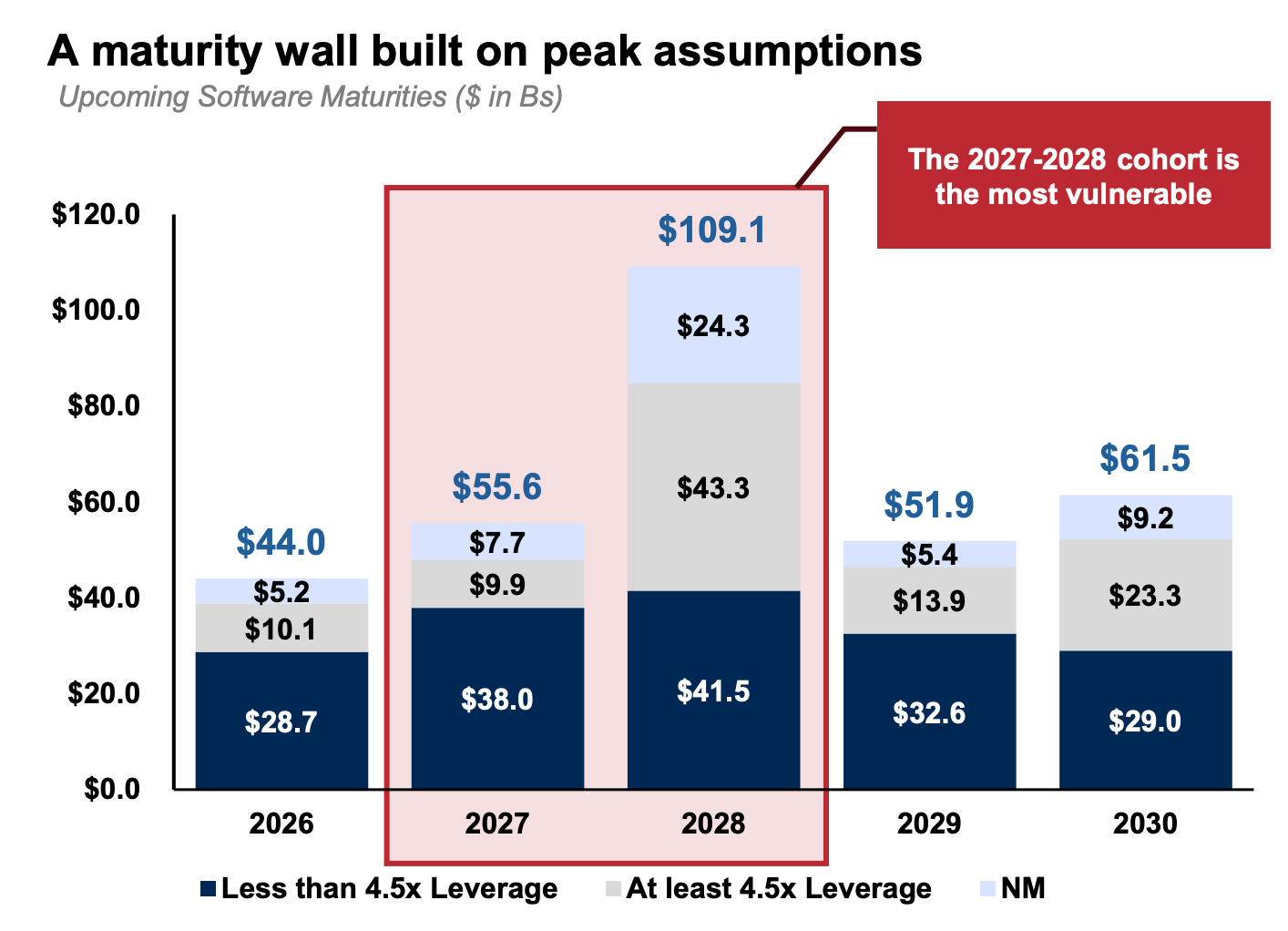

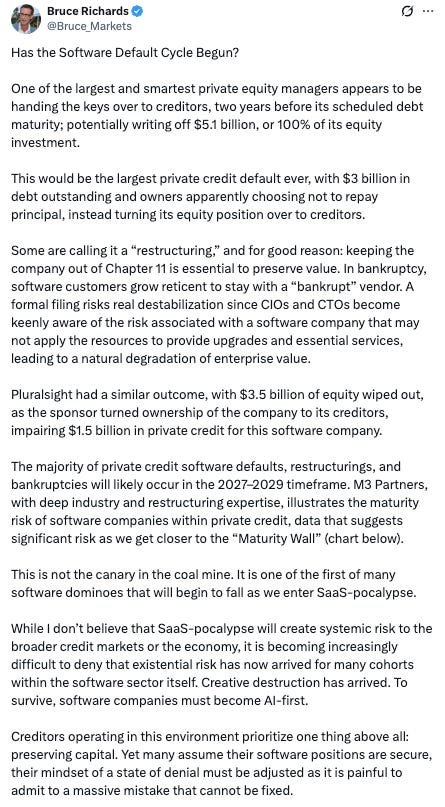

Tee up Marathon Asset Management’s Bruce Richards as one of those who likely agrees that default levels are on the verge of increasing. Citing this chart from M3 Partners …

… he tweeted:

And this response seems directionally on point:

But note Richards’ time horizon, 🤔. Not to sound like a broken record …

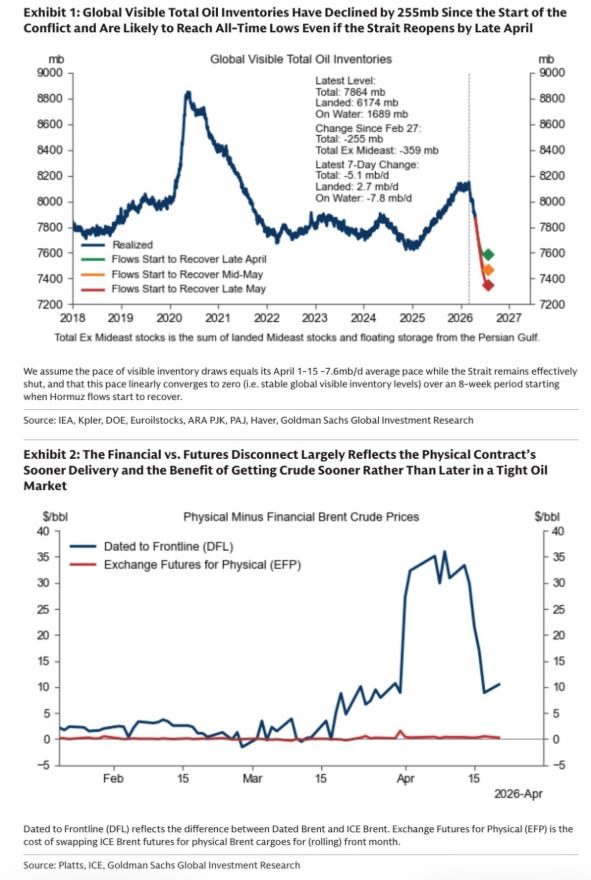

… but we (and you) could be forgiven for thinking that things should be a lot busier NOW, rather than looking out to ‘27. On that point, here are a number of things we found interesting from the past week — all of which have to deal with fallout from Iran.

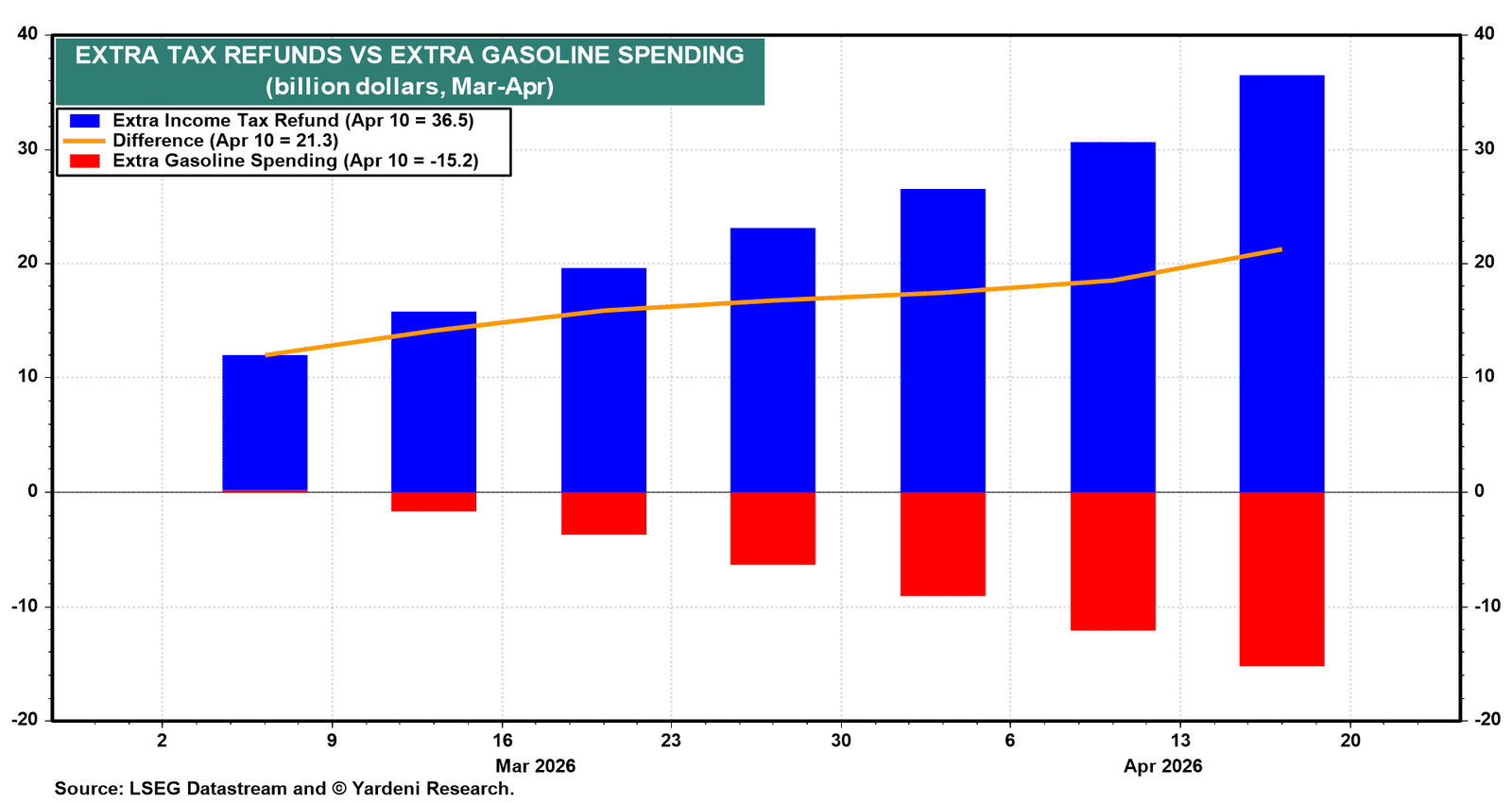

First, from Yardeni Research (paywalled), "Our in-house analysis shows that the increase in income tax refunds from the One Big Beautiful Bill Act more than offsets the rise in gasoline spending since the outbreak of the war. We estimate that the refund tailwind exceeds the gasoline headwind by more than $20 billion as of early April."

But that can’t persist forever. And sooner rather than later the demand side of the equation will have to meet supply.

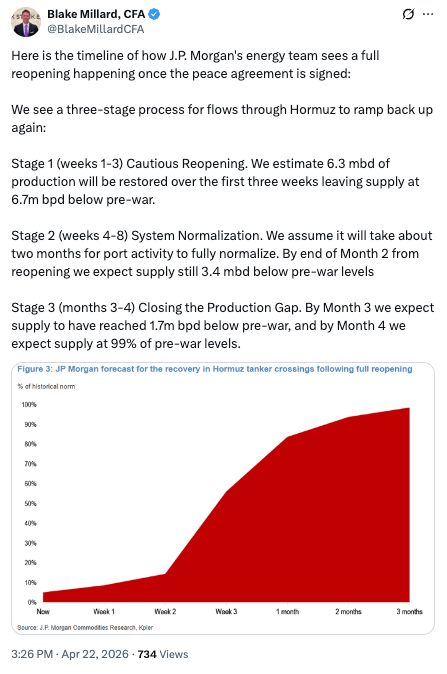

All of that is just the appetizer, though. This 👇 is the main course (worth clicking through for a JPMorgan research note that made the rounds late this week):

Here is a summary in case X isn’t your jam:

Which brings us back to Mr. Richards. There’s been a lot of talk about cockroaches in the private credit space serving as the canary in the coal mine — the precursor to much more distress in the market. But given the administration’s failure to truly reopen the Strait and the consequent outlook for oil, will Spirit Airlines end up being the real canary, 🤔?

⏩One to Watch: Vivid Seats Inc. ($SEAT)⏩