💥Skillsoft's Selling Stuff💥

Updates: Skillsoft Corp. ($SKIL) + Terra Property Trust, Inc. ($TPTA). Camp Mystic LLC files for chapter 11 after tragedy.

The team had been scattered for the holiday and now we’re playing catchup. Let’s dive right in ⬇️ with two short updates and some unfortunate coverage.

⚡️Update: Skillsoft Corp. ($SKIL)⚡️

In March ‘26, we covered Skillsoft Corp. ($SKIL)(”Skillsoft” or the “company”), the New Hampshire-based digital learning platform for enterprises to teach employees about leadership, technology, and compliance. We obviously don’t comply with sh*t over here at PETITION so we obviously don’t force-feed our team the company’s mindless videos and Johnny couldn’t be more thankful. As if he would watch that sh*t anyway.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

We won’t force-feed you all the history here. You can go back and read about the company’s first bankruptcy in ’20, its ’21 de-SPAC, and its ’21-22 acquisition spree👇:

You’ll recall that at the time of 👆 that piece, the company had just axed the entire curriculum team of Codecademy, the learn-to-code platform it purchased for …

… $525mm in ’22, and announced that it was undertaking a strategic review of its much larger and money-losing Global Knowledge (“GK”) business. The GK segment is Skillsoft’s live instructor-led training business, which has been eviscerated by AI.

Since then Skillsoft has reported earnings for FY26 (ended Jan ’26) and 1Q27 (ended April ’26). For the year ended January 31, 2026, Skillsoft revenue ⬇️ 3% due to declines in the GK business. Revenue from the Talent Development Solutions (“TDS”) segment, Skillsoft’s only segment going forward, was flat for the second year in a row. Adj. EBITDA was also flat, but according to Executive Chair and CEO Ron Hovsepian, these results were “strong”:

“This quarter’s strong TDS Segment results, led by TDS enterprise solutions, demonstrate the critical role Skillsoft plays in helping organizations navigate the rapid pace of human and AI change.”

For the quarter ended April 30, 2026, Skillsoft reclassified GK as discontinued operations and excluded it from its results. Revenue declined 5% YOY, and Adj. EBITDA declined 1%. Adj. EBITDA margins improved 110bps YOY to 28%, due to cost cuts across SG&A. The exclusion and eventual sale of the GK business is immediately accretive to margins as well.

There’s more.

On May 20, 2026, the company announced that it had entered into an agreement to sell the GK business to Enduring Ventures. As announced, Skillsoft was to receive $10mm of initial consideration, funded by GK’s own cash, a seller note, and/or third-party financing. Beginning nine months post-closing, Skillsoft will also be entitled to another $8mm deferred consideration, payable in five quarterly installments.* Get that clock started: the company announced that the sale closed on Monday, July 6, 2026. One hiccup though: the initial consideration dipped to $5.4mm in the form of a seller note “…after the application of agreed adjustments based on the estimated working capital, including cash, and indebtedness of the Global Knowledge Business.”

Unfortunately, however, the sale of GK barely moves the needle for the company’s liquidity position. But getting rid of the negative EBITDA business will stop some of the bleeding and should enable the company to focus on its better, but still struggling, TDS business.

The company ended the quarter with $116mm of cash, $580mm outstanding on a First Lien Term Loan B due July ’28 (S+525)(the “1L TLB”), agented by Citibank NA ($C), and $1mm drawn on its $75mm A/R facility from First Citizens BancShares Inc. ($FCNCA). The company has ample liquidity between its cash on hand and availability under its A/R facility ($35mm as of April ’26). Still, the 1L TLB has been ticking downward of late; it was pricing just a hair over 53c on the dollar roughly two months ago and sits just barely over 50c as of July 6, 2026; it was pricing just under 70c back in January. 😬📉

For its part, the stock has traded up from its April ’26 nadir, momentarily bringing its market capitalization back above the $50mm NYSE listing requirement (the company received a delisting notice in March ‘26). Whether it will stay there is another matter — the stock has been roller-coastering over the past several weeks. The market did, however, receive the news of the GK sale well: the stock is up just under 9% since Monday.

With no maturities until ’28 and ample liquidity for the time being, Skillsoft has some runway, but what exactly it plans to do with it is unclear. The sale of GK removes a distraction and improves the profile of the remaining business in the age of AI, but management will no longer be able to deflect problems in their core TDS business by saying it’s at least better than GK.

*Jefferies LLC served as financial advisor to Skillsoft. Skadden, Arps, Slate, Meager & Flom served as legal counsel. We hear through the grapevine that other professionals are involved with respect to restructuring discussions of some kind.

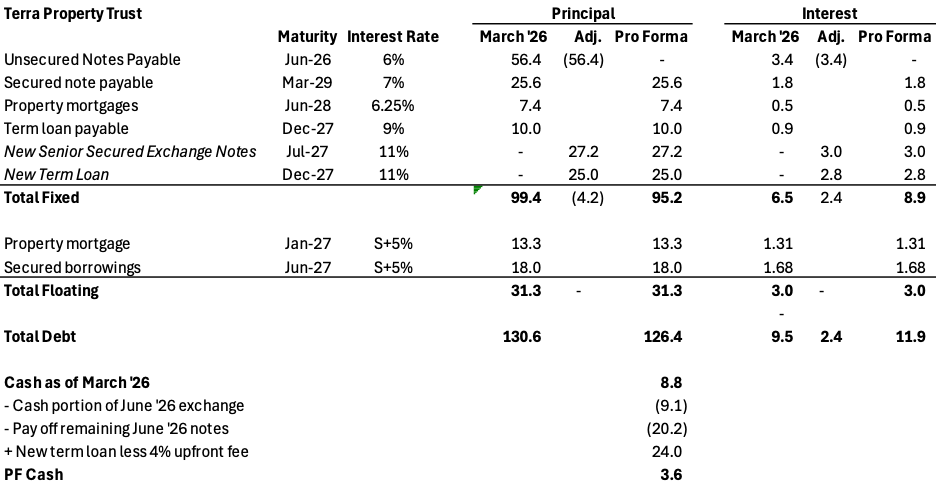

⚡Update 1: Terra Property Trust, Inc. ($TPTA)⚡

We’re back on NYC-based Terra Property Trust, Inc. ($TPTA)(“Terra” or the “company”), the struggling REIT we covered a mere fortnight ago.

Two weeks ago, the company was imploring its creditors to take up its offer to exchange $56mm of its 6% senior notes due June 30, 2026 (the “June ‘26 unsecureds”) for a combination of cash and new senior secured notes equal to 100c on the dollar.

In a bid to secure broader participation, Terra amended its offer twice. First, it raised the rate on the new notes from 8% to 11% and moved up the new maturity date from December ‘27 to July ‘27. Then, it returned to the market again to increase the cash portion of the exchange from 20% to 25%. At the time of the second amended offer, the company noted that 66% of existing noteholders ($36mm of $56mm) had submitted non-bindings letters of intent. It also said that at that participation threshold, expected cash outflows over the next six months would exceed expected inflows ($52mm out vs. $47mm in).

On June 29, 2026, three days after the offer expired, Terra announced the results. It had no more takers than the initial 66% of noteholders it had referenced in its earlier filings.

The company followed up with a second announcement on July 2, 2026, reporting that it had (i) completed the exchange, (ii) paid off the remaining $20mm of June ‘26 unsecureds, and (iii) secured a $25mm 11% term loan due December ‘27 to cover the cash portion of the exchange and repay existing notes. The new term loan lender is Strategic Yieldco LLC, which has been linked to Axar Capital Management L.P. (“Axar”) in past deals. Axar was the last owner of the company’s sponsor, Terra Capital Partners, before current management bought Axar out in ‘21.

With this latest series of transactions, Terra will reduce its overall debt burden by $4.2mm, while adding $2.4mm of additional interest expense annually.

Terra has tackled two maturities (March ‘26 and June ‘26) through exchanges and repayments this year, but these latest deals have not kicked the can very far. The company now has six months until its next maturity ($13mm) and a full $93mm due over the next 18 months. It’s very “TBD” whether the company even makes it that long though: by its own estimates, it’ll be out of cash in the next six months.

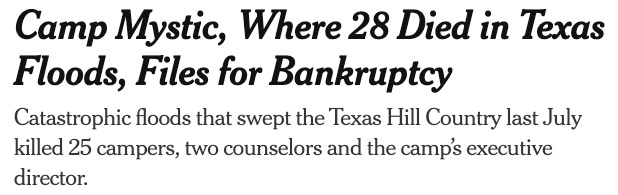

😞New Chapter 11 Bankruptcy Filing - Camp Mystic LLC 😞

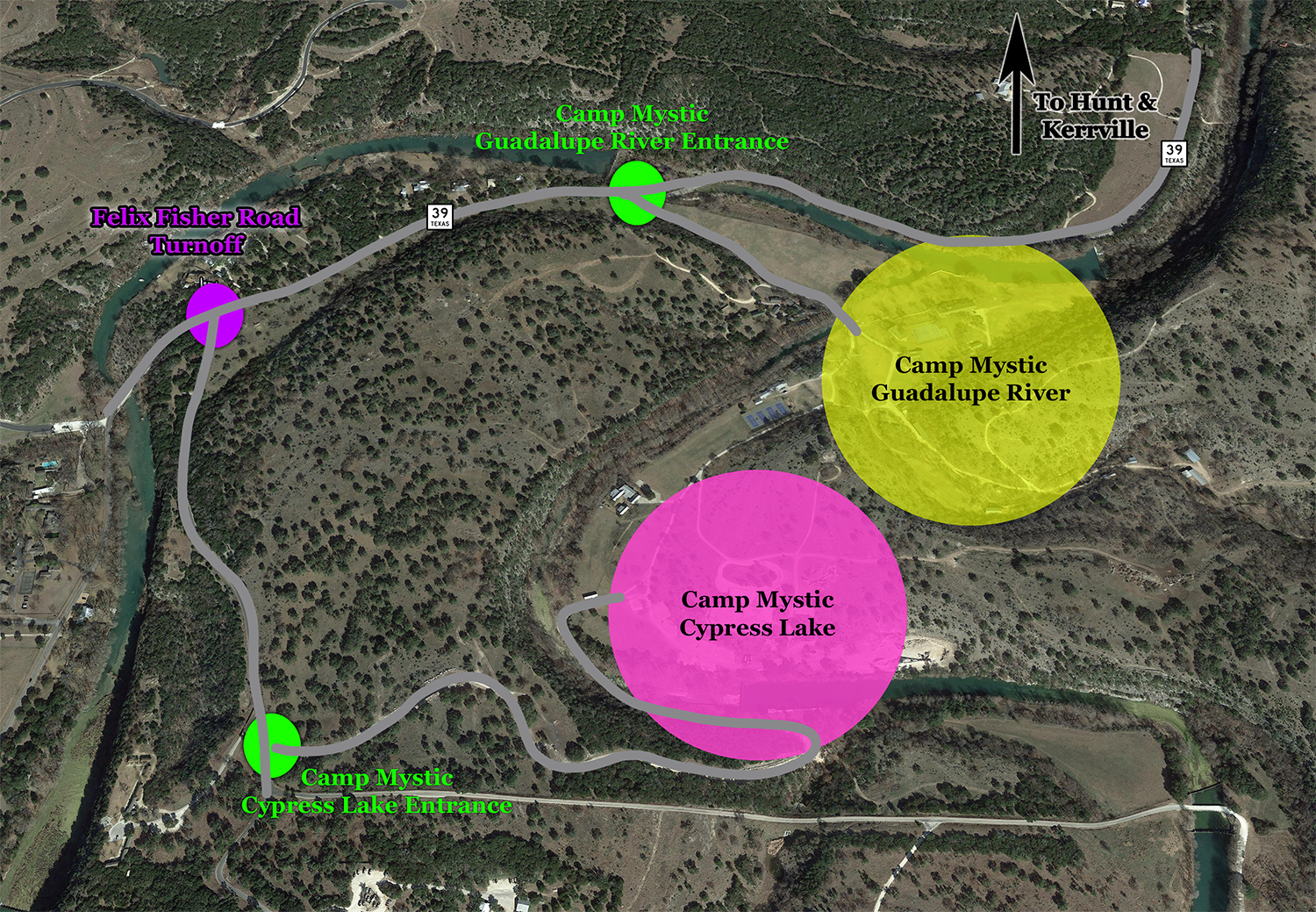

On June 24, 2026, Camp Mystic LLC and three affiliates (the “debtors”) filed chapter 11 bankruptcy cases in the Southern District of Texas (Judge Lopez) and we’re gonna be up front here: we’ve got no jokes for this one.

Originally built in 1926, the debtors own/operate a private Christian girls summer camp named Camp Mystic in the hill country of west-central Texas. You probably (and unfortunately) heard of it:

Heartbreaking, and as good as reason as you’re ever going to have to go hug your kids this very moment.

Kids that, in at least some cases, are home this summer rather than away at camp. The debtors, which filed with an estimated $1-10mm in assets and $10-50mm in liabilities, didn’t open their doors this summer amidst political pressures. Pressure that is entirely understandable — a recent joint report from the Texas legislature suggests much could have been done to prevent the tragedy, a point that an ad hoc group of victim families (the “ad hoc group”), represented by Gray Reed (Jason Brookner, Lydia Webb), raised at the June 30, 2026 first day hearing.

The benefit of hindsight, however, is a day late, a dollar short for the victims’ families, who, along with claims for tuition deposits, compose the debtors’ entire top 30 list, 😔.

As mentioned above, the court held an initial first-day hearing on June 30, 2026, where the only items on the agenda were joint administration and a request to continue paying the debtors’ eleven employees. The latter one was … not well received.

From a legal standpoint, we mean. CRO Karen Nicolaou was retained around “… dusk …” on June 26, 2026 — aka the petition date — and her first day declaration was filed about an hour later. Tucked into it, she tried to form the basis to pay employees and a $2k/month stipend to William Neel Bonner, III, the “… 1099 …” president of debtor Natural Fountains Properties, Inc.

The court did not give authority for the second half of that ask. After Akin Gump Strauss Hauer & Feld LLP’s (“Akin”) Marty Brimmage, on behalf of, 😞, his former colleague and partner and restructuring attorney Lacy Lawrence and her husband John Lawrence — the parents of two children victims to the tragedy — forced Ms. Nicolaou to take the stand and probed her on her position and her general knowledge of the debtors, it became abundantly clear Ms. Nicolaou lacked … erm … let’s just keep it at that … lacked.

Again, we mean no jokes on this one. Suffice it to say, the performance at the hearing did not constitute a good look for the debtors’ pros.

Nor, consequently, was it pleasant. After about 100 minutes of stumbling and fumbling, Judge Lopez had enough. Mr. Bonner’s gonna have to wait on that stipend, he decided, although other employees, not a single one of which could be named by the declarant live, slipped through.

The debtors, however, will have another, hopefully-better-prepped bite at the Mr. Bonner apple tomorrow — July 9th, 2026 (1pm CT) — at a hearing during which the court will also let them shoot their first shot on other customary first-day relief.

Our hearts go out to the Lawrences and the other victims and their families.

The debtors are represented by Vertabedian Katz Hester & Haynes LLP (Martin Sosland, Candice Carson, Jeff Prostok, Emily Chou, Suzanne Rosen, Lynda Lankford, Deirdre Brown, Mary Stanberry) as legal counsel and Harney Partners (Karen Nicolaou) as financial advisor and CRO. The aforementioned ad hoc group is represented by Gray Reed (Jason Brookner, Lydia Webb). Lacy Lawrence and John Lawrence are represented by Akin (Marty Brimmage, Roxanne Tizravesh) as legal counsel.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

📩 Notice 📩

Konstantin Malyshkin (Principal) joined Ensis Partners from Houlihan Lokey.

🍾Congratulations to…🍾

Berkeley Research Group, LLC (Evan Hengel) for securing the financial advisory mandate on behalf of the official committee of unsecured creditors in the Bitcoin Depot Inc. chapter 11 bankruptcy cases.

Dundon Advisers LLC (Joshua Nahas) and Foresight Restructuring LLC (Yi Zhu, Ker Gibbs) for securing financial advisory co-mandates on behalf of the official committee of unsecured creditors in the Simply Interior Homes, LLC chapter 11 bankruptcy cases.

McDermott Will & Schulte LLP (Darren Azman, Kristin Going, David Hurst, Andrew Mark) for securing the legal mandate on behalf of the official committee of unsecured creditors in the Sangamo Therapeutics Inc. chapter 11 bankruptcy case.

Womble Bond Dickinson (US) LLP (Matthew Ward, Lisa Bittle Tancredi, Marcy McLaughlin Smith, Philip Mohr) for securing the legal mandate on behalf of the official committee of unsecured creditors in the Searles Valley Minerals Inc. chapter 11 bankruptcy cases.