💥QVC: 'C' for Confirmation?💥

Updates: QVC Group Inc. + First Brands Group LLC

⚡️Update: QVC Group Inc.⚡️

We’ve previously covered this name here, here, here, here, here and here — which, admittedly is a lot in a compressed amount of time but the cases have been moving quickly.

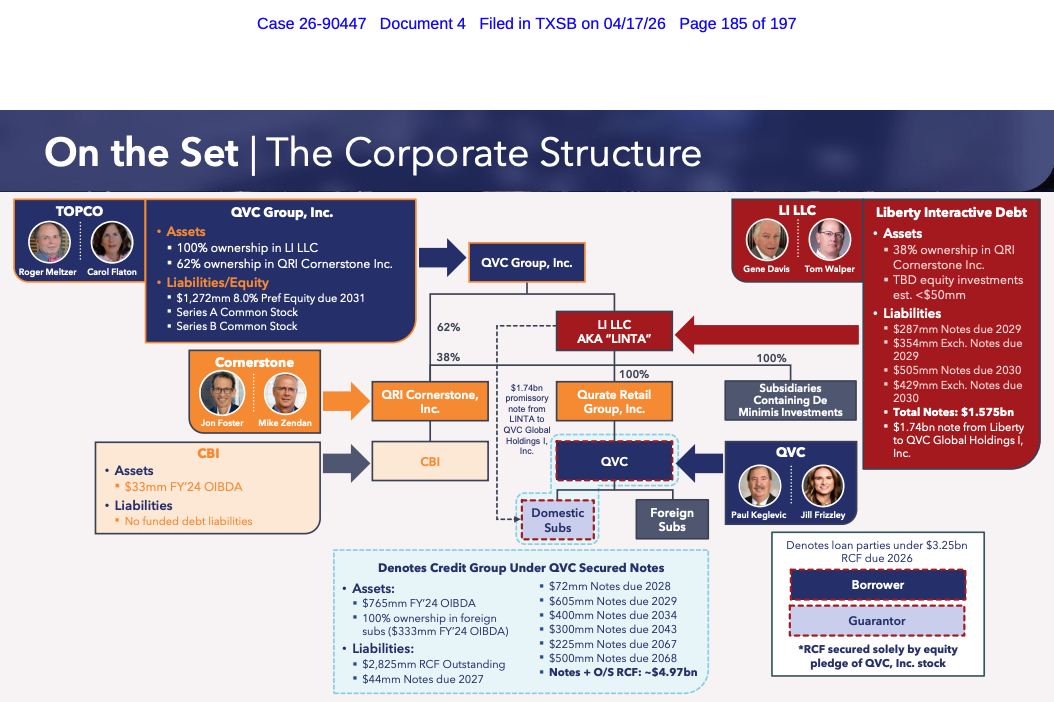

By way of refresher, you may recall that back on April 16, 2026, QVC Group Inc. (“QVCG,” a/k/a Qurate Retail Inc.) and 73 subsidiaries including QVC Inc. and Cornerstone Brands Inc. (“Cornerstone,” collectively with QVC Inc. and the other filing subsidiaries, the “debtors”) filed chapter 11 bankruptcy cases in the Southern District of Texas (Judge Perez). The (relevant) debtors’ petition date corporate structure looked like this …

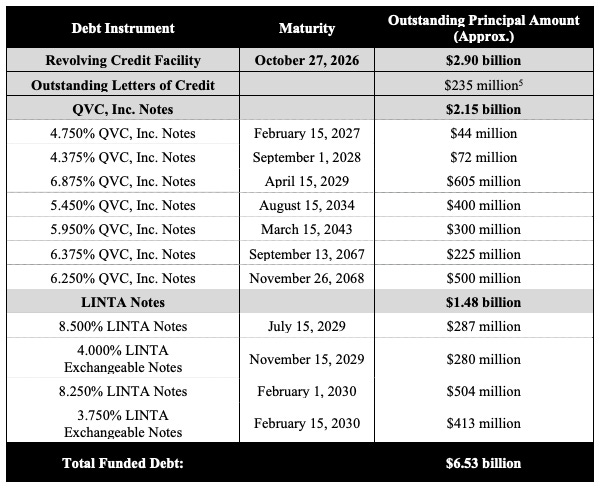

… and the debtors’ godforsaken capital structure like this …

… and both charts ought to increase your anxiety levels.

It certainly did for the holders of preferred equity at the QVCG level.

Those dudes weren’t so thrilled with the debtors’ plan (and Plan, defined below) to fast pace this b*atch through bankruptcy and reorganize around the revolving credit facility* and QVC Inc. notes** as the fulcrum security — not necessarily because they had an issue per se with the elimination of a billions of debt from the cap stack nor necessarily because they beefed with general unsecured creditors getting paid in full. No, rather, they were pissed because they saw a $400mm inter-company claims “settlement” that they viewed as … how do we put this delicately … complete and utter f*cking …

… because it took a big pile of cash sitting at the QVCG box ($195mm) plus that there 👆 62% equity ownership in Cornerstone and, in their view, just gave it away to QVC Inc., leaving them with basically nothing to glom onto despite having ~$1.3b of pref outstanding against 0️⃣ funded debt.

You’ll therefore also recall that, from there, there were a bunch of separate pref holders with separate counsel vying to establish an official committee before ultimately consolidating amongst themselves and with counsel sans “official” status (the “pref group”). Meanwhile, while all of that was transpiring, the prefs became a trade; they hit a high of $7.36 on May 11, 2026 and declined and became range bound around $5 for a few weeks thereafter. But they’ve slowly crept up since.

Still, the emboldened pref group, powered by consolidated counsel, filed a May 8th 2026 motion to terminate exclusivity with respect to QVCG only (the “exclusivity motion”) and, from there, the litigation process took off. Confis and protective orders, 😴, more confis and protective orders, 😴, yada yada yada.

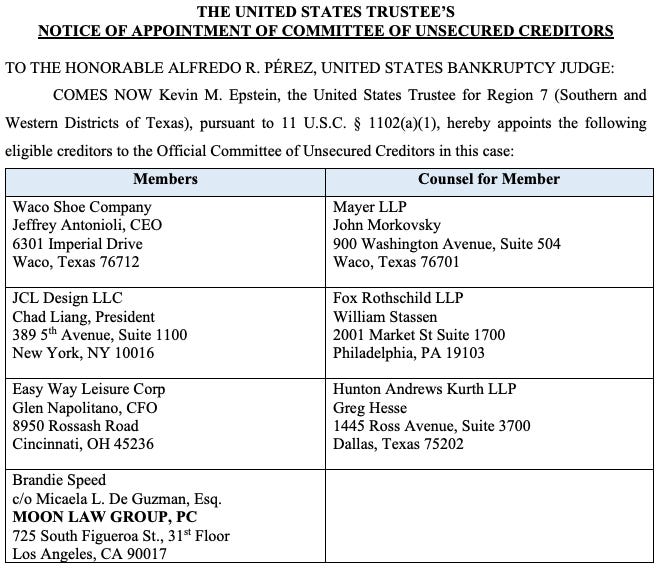

Contemporaneously — and perhaps much to the chagrin of Kirkland & Ellis LLP, counsel to the debtors and renowned defenders of thrifty chapter 11 processes, 🙄 — the Office of the United States Trustee (“UST”) went ahead and appointed an official committee of unsecured creditors (“UCC”), 🙈. Welcome to the party pals:

The UCC then turned around and hired Pachulski Stang Ziehl & Jones LLP (Robert Feinstein, Bradford Sandler, Michael Warner, Alan Kornfeld, Tavi Flanagan) to … like … do … stuff?

You can tell UCC formation wasn’t exactly on K&E’s bingo card — after all, the general unsecured creditors are supposed to ride through at 100c — by the fact that they had to amend the proposed plan of reorganization (“Plan”) to account for it:

Which, LOL, was, other than a few words relating to treatment of the LINTA Notes and payment of statutory fees, the only revision to the Plan.

Amended or not, you could bet your a$$ the Plan would see it’s share of objections. The UST led off with an objection pertaining to third party releases. Ok, fine, whatever. Zero points for originality there, UST.

But then there came the pref group with a 862-page redacted objection to Plan confirmation. You all already know the arguments. The Plan wasn’t filed in good faith, the pref group argues, and “[w]hile the Plan purports to ‘settle’ intercompany claims, it is a complete capitulation by QVCG and its fiduciaries” where “[e]very procedural safeguard that might protect the [pref group and prefs generally] has been brazenly and methodically eliminated or ignored.” The pref group states:

“The intercompany settlement does not satisfy the Rule 9019 standard because the alleged intercompany claims lack merit, QVCG’s investigation was inadequate, the process was not at arm’s length, and the agreed upon resolution clearly falls outside the range of reasonableness as evidenced by the existence of a better alternative. As a result of these substantive and procedural infirmities, the intercompany settlement must be reviewed under an entire fairness standard, not business judgment.”

Wait. Lack merit? That’s right. The pref group loaded the docket it up with thousands of pages of exhibits, the lion’s share of which were SEC filings of QVCG and QVC Inc. that failed to disclose any “…known litigation claims…” against one another. Why the lack of disclosure? Because they — claims of (i) fraudulent conveyance emanating out of ~$800mm distributed from QVC Inc. to QVCG in connection with a 2022 cash management plan and ~$343mm in post-2022 dividends transferred from QVC Inc. to QVCG and (ii) alleged tax claims — were just conjured up out of thin air, the pref group says, and blessed by a management team incentivized by a rich management incentive plan and directors getting sweet monthlies and releases. For its part, the UCC, the pref group argues, obviously has no incentive to upset the apple cart either: remember, it’s getting that 100c treatment!

For their part, the debtors are having no part of this; they argue the settlement is fair, the Plan is confirmable, and that, even if the Plan doesn’t get confirmed in the first instance, the pref group’s exclusivity motion ought to be denied pursuant to long-standing caselaw.*** They write:

“The Bankruptcy Court should confirm the Plan. Standing in the way are certain preferred equity holders at QVCG. But as will be demonstrated at confirmation, neither the facts nor the law support—in any way—their objections.”

They add:

“Central to the Plan is a global settlement of all actual and potential intercompany claims among the four Debtor groups—QVCG, the QVC Debtors, the LINTA Debtors, and the CBI Debtors (as defined in the Plan, the “Intercompany Settlement”). The evidence will unequivocally demonstrate that the Intercompany Settlement satisfies Bankruptcy Rule 9019 per Fifth Circuit precedent that comprehensively considers the following four-part analysis: (a) the process that led to the settlement; (b) the complexity, duration, expense, delay, and inconvenience of litigation as opposed to settlement; (c) the probability of success in litigating the underlying claims; and (d) all other factors bearing on the wisdom of the compromise.”

From there they spend 193 pages arguing the case.**** But, for TL;DR purposes, they basically be saying:

The combined hearing for approval of the disclosure statement and the Plan is currently set for tomorrow, June 4, 2026 at 1pm. As things stand now, absent an 11th hour settlement, it will not end on June 4. The pref group intends to offer up all kinds of evidence and potential testimony to support its objection. The debtors will counter. This will take a lot of time. And we’ll be eating a lot of 🍿.

*The RCF lender group has changed a bit from April 30 when it first filed a 2019 statement to May 29 when it filed its first supplemental statement. The total RCF commitment represented by the group declined by $344mm. It seems certain RCF loans were sold to members of the QVC noteholder group. Several banks are no longer part of the group, e.g., Bank of America, BNP Paribas, Citibank NA, Credit Agricole, JPMorgan (as lender, rather than agent), Societe Generale. Collectively, these institutions represented ~$907mm. For its part, Silver Point Capital increased its holdings by $112mm. Meanwhile Strategic Value Partners upped its QVC fandom by $450mm, making it the largest beneficiary of loan transfers. Traditional banks out, sophisticated distressed debt investors in, 🤔.

**The QVC noteholder group also changed a bit. BlackRock Financial Management Inc. dropped off. Goldentree Asset Management LP added to its position across a variety of issuances. Similarly, Whitebox Advisors LLC appears to have increased its holdings across a number of maturities.

***As you might expect, both the RCF lender group and QVC noteholder group have joined on to the Debtors’ opposition to the exclusivity motion.

****And of course there’s filed support by every other constituency in the case other than the pref group. For its part, the UCC filed a three paragraph statement in support. Such a f*cking waste, lol.

⚡Update 3: First Brands Group, LLC⚡

We last touched base on the First Brands Group LLC and its 111 affiliates (collectively, the “debtors”), whose cases are pending in the Southern District of Texas (Judge Lopez), in mid-March ‘26 …

… and concluded with:

“… [I]f we had to place our bets today, we’d put our money on this dumpster fire eventually being some chapter 7 trustee’s job to ultimately clean up.”

That appears to be the way it’ll go.*

Less than two weeks after our prior coverage, on March 23, the debtors lit the kindling …

… which caught flame and, of course, further expanded to include each and every business unit.**

Checks out, but more to the point, though, on May 13, 2026, the US Trustee (the “UST”) got feisty and slapped this bad boy here on the docket:

Better late than never, but we won’t digress. The impetus for the filing was the debtors’ April 28, 2026 chapter 11 plan and disclosure statement (“DS”).

Wait — did we say “debtors’”? LOL, our bad. Call it a force of habit!

We meant to say exclusively debtor Premier Marketing Group, LLC’s (the “plan debtor” and the debtors excluding the plan debtor, the “FBG debtors”) plan and DS — latest versions here and here — which 100% don’t apply to the FBG debtors.

Why, you ask?

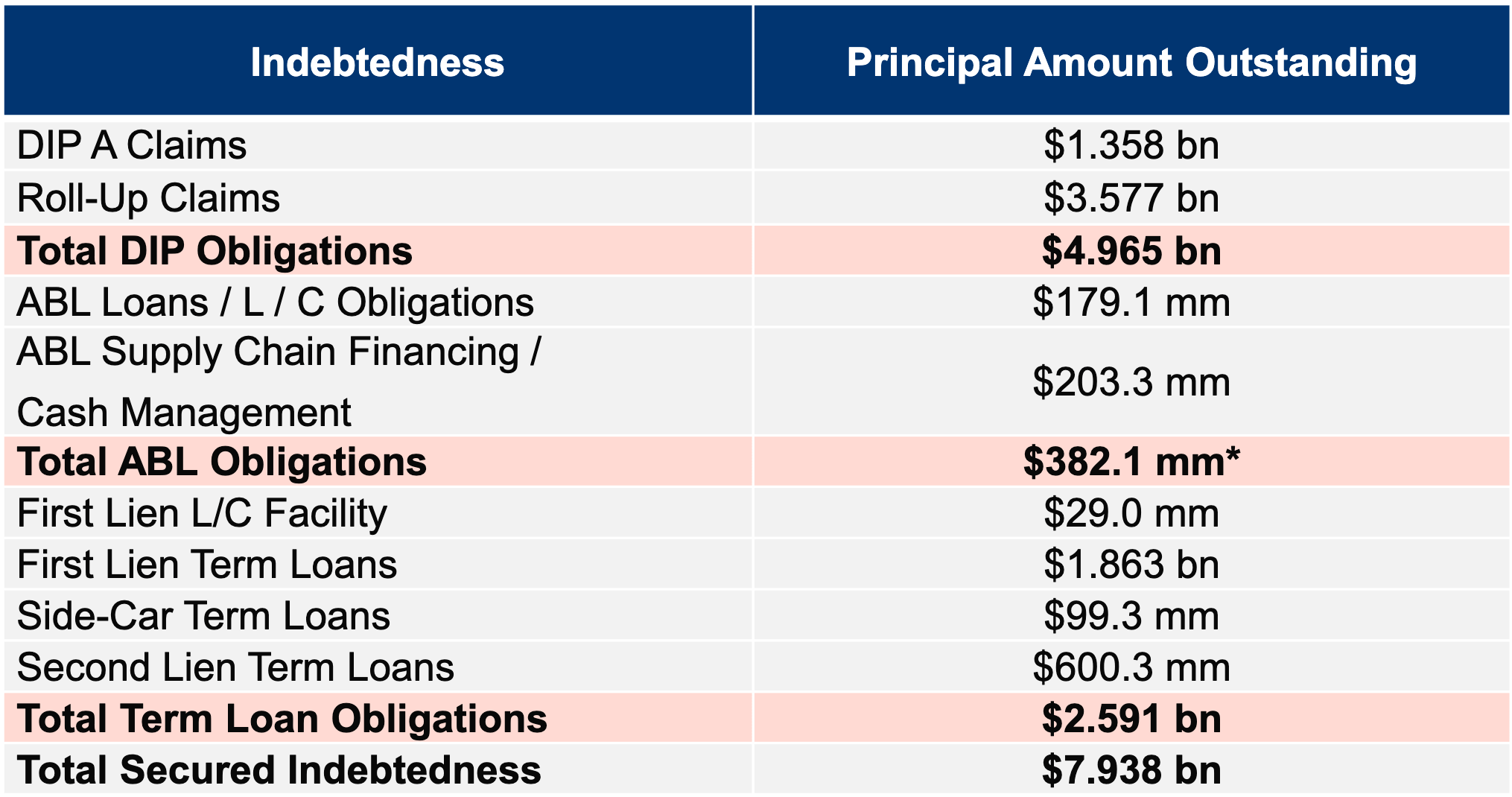

Well, the DS discloses that the debtors have an estimated “… $223 million in Administrative Expense Claims …” and “… the DIP Obligations (totaling no less than $5 billion) are set to mature on June 29, 2026 and the DIP Loan Parties and Parent Guarantors do not have sufficient funds to indefeasibly pay the DIP Obligations in full in Cash.”*** Therefore, these debtors be fully cooked. To a crisp.

But the plan debtor itself. It’s a box lacking any known admin or priority claims of its own — other than, you know, admin expenses like debtors’ counsel Weil, Gotshal & Manges LLP’s (“Weil”) costs, which gives Weil a shot at getting any confirmation order at all in these cases. We suppose one debtor is better than none, but it’s, oh, 111 short of the goal.

Anyway. Under the plan and a very-intertwined May 26 “global settlement” negotiated with the official committee of unsecured creditors and the DIP-lending, 13-page long ad hoc group, the following will happen (🤞, but not for us):

📍The plan debtor will establish three trusts: a litigation one, a DIP collateral one, and an ABL collateral one.

As to what goes into them, the DIP collateral trust and the ABL collateral trust aren’t hard: respectively, it’s (i) IP, real estate, machinery and equipment, and other DIP collateral and (ii) A/R, inventory, and the ABL’s other priority collateral.

The litigation trust, however, is novel — if the part-and-parcel settlement is approved, the FBG debtors would sell their causes of action and insurance rights to their DIP lenders via a credit bid, who, in turn, will contribute them, as well as potential direct creditor claims,**** to the trust in exchange for interests,***** which would then liquidate the lot using $75mm in funding — $25mm from the balance sheet and $50mm backstopped by DIP lenders — and distribute any proceeds.

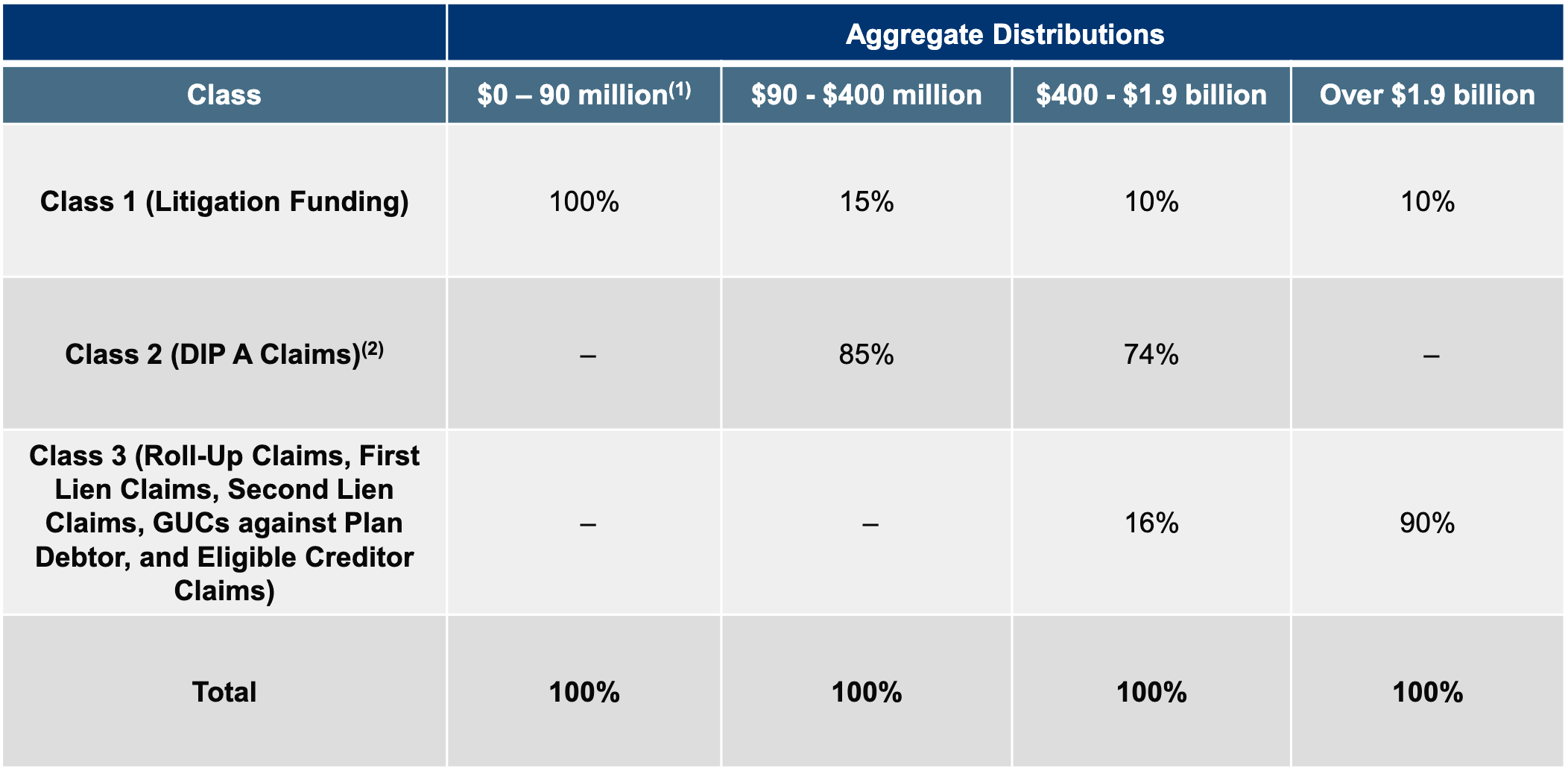

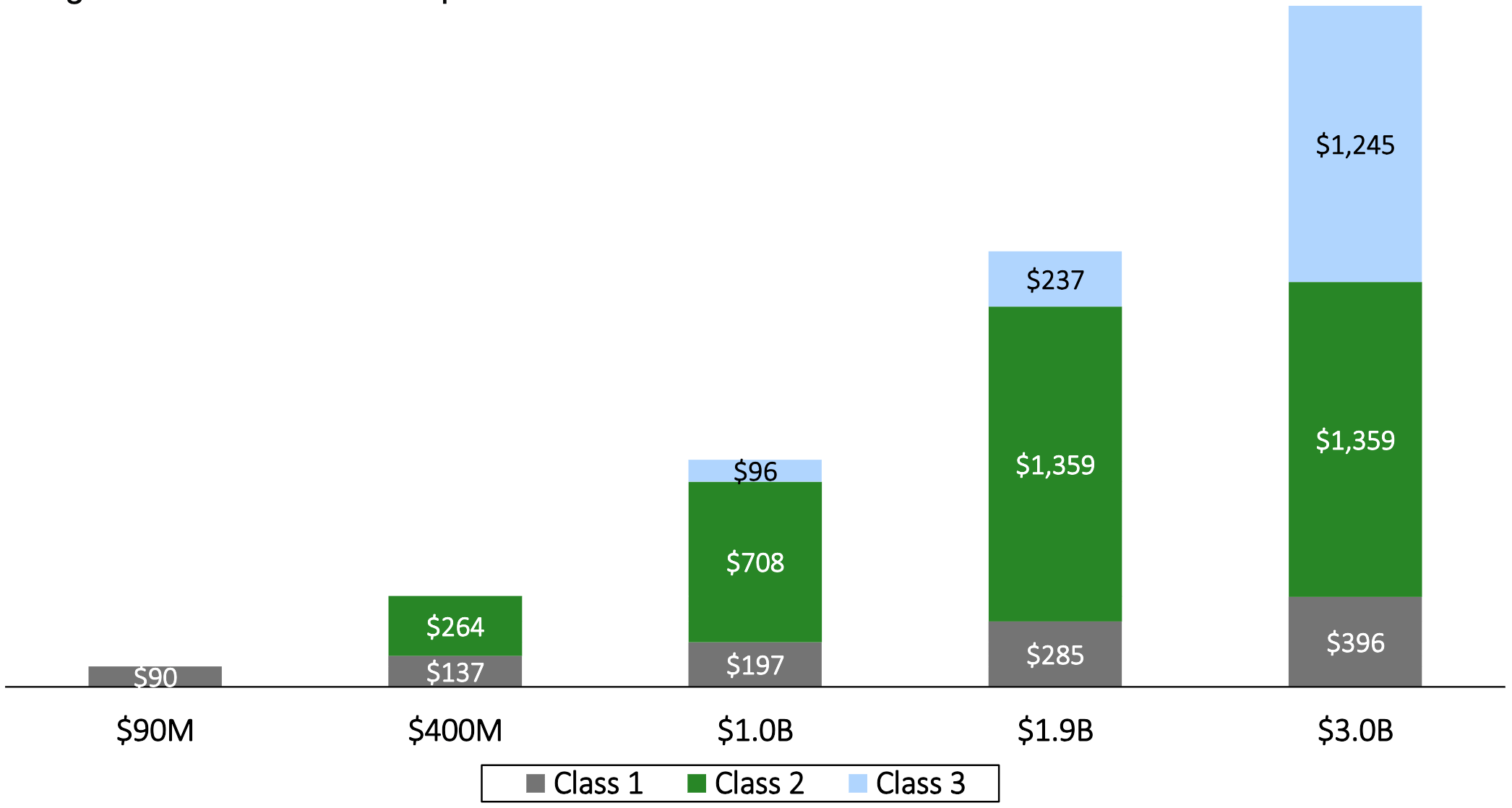

To the extent value ever comes in … Here’s the proposed waterfall:

“Eligible creditors” in class 3 is doing a lot of work here too. It’s the holders of admin claims —all $223mm of them!, other secured claims, priority claims (including tax), and GUCs against the FBG debtors … of which there’s a lot …

📍… but none of whom will be voting on the plan. By design the debtors will only ask for votes from the holders of claims against the plan debtor, which includes roll-up, first-lien, and second-lien holders, plus any GUCs at that box, but let’s not pretend Weil is counting on them.

📍If those votes come in and confirmation happens, the FBG debtors’ cases would kick over to chapter 7 on the effective date … but by then, they’d be asset-less, so it’s not like that would lead to anything. Meanwhile, the trusts would get to work by continuing suits again Patrick James — who’s already been indicted by the US Securities and Exchange Commission — and other First Brands executives and insiders.

You only need about ~$1b in recoveries for that to really matter to class 3.

Honestly, that’s pretty much the plan. And honnnnnnestly, it’s a clever attempt to sidestep wholesale administrative insolvency. That’s more or less the UST’s beef; from its motion:

“The Debtors [] through a proposed sleight of hand, attempt to avoid the Bankruptcy Code’s requirements to pay all administrative claimants on the Effective Date. The FBG Debtors propose a so-called ‘Global Settlement’[] that transfers the most valuable remaining assets, the Estate Claims, from each FBG Debtor to the Plan Debtor without any consideration, while leaving the FBG Debtors with their respective liabilities.”

We wouldn’t call the argument a slam dunk.

We’d say the same about the debtors too. On May 26, Judge Lopez had this to stay about their request for conditional approval of the DS to start soliciting:

“The debtors are proposing a plan. It’s novel, and it’s incredibly complicated at the same time. They want conditional approval today. There’s a related global settlement motion that’s intertwined and inextricable from the plan, and it was filed this morning…

The plan supplement filing deadline is proposed to be June 12 and then they’d be a kind of combined voting and objection deadline on June 23rd. That leaves parties fewer than twelve days …

By Johnny’s count it’s eleven. In any event …

… “to study three trust agreements, asset schedules, credit bid asset purchase agreement, the identity of at least several post confirmation fiduciaries, an emergent steps memorandum, and a non-exhaustive schedule of non-released parties…

It’s not a list of ministerial exhibits; it’s the operational architecture of a structure that’s going to govern the disposition of billions in assets across 111 converting debtors. It’s not enough time for creditors — many of them trade creditors — to evaluate these documents and make decisions that may be irrevocable…

I’m not comfortable using conditional approval here because everything is so intertwined given the concerns that I have over the structure of the global settlement and what the global settlement seeks to accomplish. I don’t want to approve, proceed on a conditional basis.”

So, denial (without prejudice) was the response.

Although time will go on, a few docs will presumably make their way onto the docket, and the debtors will try again.

Or maybe they won’t have the opportunity. The UST’s fight to convert will take place on June 12, 2026 at 10am CT.

*Or “continue going.” On April 9, and with the consent of the debtors and SPV lender Evolution Credit Partners, the court converted the cases of the latter’s borrowers: Patterson Inventory, LLC, Patterson Inventory Holdings, LLC, Starlight Inventory I, LLC, and Starlight Inventory Holdings I, LLC.

**The debtors approved a few more sales along the way, but as you’ll see, who gives a sh*t? The purchase prices weren’t enough.

***One of whom is going to wind up being Martin De Luca, the debtors’ examiner. He exhausted his $7mm budget by April ‘26, and while he has requested more, nothing has materialized. However, he did file an “interim,” preliminary report in late April ‘26. The results aren’t good:

“the Examiner’s preliminary view is that the Debtors operated as a conventional commercial enterprise sustained by fraudulent financing transactions. The principals used the Debtor and non-Debtor entities interchangeably to further their fraudulent enterprise… With respect to Third-Party Factoring, the evidence indicates that the Debtors engaged in widespread fraud on the Third-Party Factors to generate massive amounts of cash for FBG.”

****Creditors with preference exposure can agree to contribute their claims for waivers and/or modified defenses.

*****The exchange for trust interests is critical. Under the final DIP order, the DIP lenders agreed to carve out $200mm for the debtors’ admin creditors after the new-money piece of the DIP was repaid in full in cash. But trust interests aren’t cash, so the debtors and the DIP lenders are taking the position the carveout isn’t triggered. Fun.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

📤 Notice📤

Brya Keilson (Partner) joined Robinson+Cole from Morris James LLP.

Michael Koch (Associate) joined Simpson Thacher & Bartlett LLP from Kirkland & Ellis LLP.

Marcus Helt (Partner) joined Dechert LLP from McDermott Will & Schulte LLP.

Jack Haake (Partner) joined Dechert LLP from McDermott Will & Schulte LLP.

Jerry Hall (Partner) joined Dechert LLP from McDermott Will & Schulte LLP.

🍾Congratulations to…🍾

Anne Wallice on her promotion to Partner at Sidley Austin LLP.

Clay Taylor on his promotion to Partner at Spencer Fane LLP.

Jason Hufendick on his promotion to Partner at Sidley Austin LLP.

Maegan Quejada on her promotion to Partner at Sidley Austin LLP.

Caplin & Drysdale (Todd Phillips, Kevin Davis, Ariel Hayes, Serafina Concannon) for securing the legal mandate on behalf of the official committee of unsecured creditors in the Miyoshi America, Inc. chapter 11 bankruptcy cases.

Dundon Advisers LLC (Eric Reubel) for securing the financial advisory mandate on behalf of the official committee of unsecured creditors in the Hronis, Inc. chapter 11 bankruptcy cases.