💥New Chapter 15 Filing - Braskem S.A.💥

Another Brazilian megacorp — and a US subsidiary! — seek chapter 15 relief

On June 26, 2026, Braskem S.A. and five affiliates (collectively, the “debtors” and together with their non-debtor affiliates, the “company”) filed long-anticipated chapter 15 recognition proceedings through their foreign representative Antonio Reinaldo Rabelo Filho (the “foreign rep”) in the Southern District of New York (Judge Wiles). A growing trend!

The company is the Americas’ largest producer of thermoplastic resins and petrochemical products, servicing customers in over seventy countries, generating 80b+ BRL (or ~$15.5b) in net revenue in ‘24, and employing ~8k individuals, who, after July 5, 2026, were able to get back to focusing on work and less on soccer.

Low blow, we know.

In fairness, the Norwegians are a world-renowned powerhouse in the sport, 😂.

Anyway. Brazil is by far the company’s largest market, accounting for ~72% of that annual revenue ☝️. However, it’s a global player, and therefore, the company has to deal with global issues … like:

📍Market Downturn. A worldwide downturn in the petrochemical industry, which has been ongoing since ‘22 but really ramped up in ‘25 on account of ever-shrinking spreads. As a result, the company dropped its production in ‘25, and factories went from 72% utilization in ‘24 to 59% one year later. Net revenue joined in on the ride, declining 16% in 4Q’25 to ~$3.1b USD, and cash FLED the business — outflow increased 10x from ~$95.7mm in ‘24 to $1.13b in ‘25.*

📍Rock Salt Well Exploration. In ‘19, the Geological Survey of Brazil released a report linking the company’s rock salt well exploration in the Brazilian state of Alagoas to soil sinking in five neighborhoods of the city Maceió, which necessitated evacuations and the relocation of ~60k people. The company agreed to pay local authorities and, as of ‘25, had spent $2.7b+ USD on account of, as the foreign rep puts it, “… the geological event,” 🤣, with an anticipated $678mm USD to go.

📍 US-Iranian Relations. Here’s one we have and will be seeing; straight from Mr. Rabelo Filho’s mouth:

“… in early 2026, the Debtors began to face new financial and operational challenges due to the escalation of geopolitical tensions in the Middle East related to the conflict involving Iran and the United States. This conflict has driven up the price of oil and its derivatives, including naphtha—the main raw material in the petrochemical industry—directly impacting the Braskem Group’s production costs. Given the scale of the Group’s operations, even small increases in naphtha costs can result in billions in additional operating expenses. International freight rates have also risen substantially, affecting both raw material imports and international distribution costs, while trade route restrictions caused by the closure and blockade of the Strait of Hormuz have further disrupted operations and strained the Company’s financial condition.”

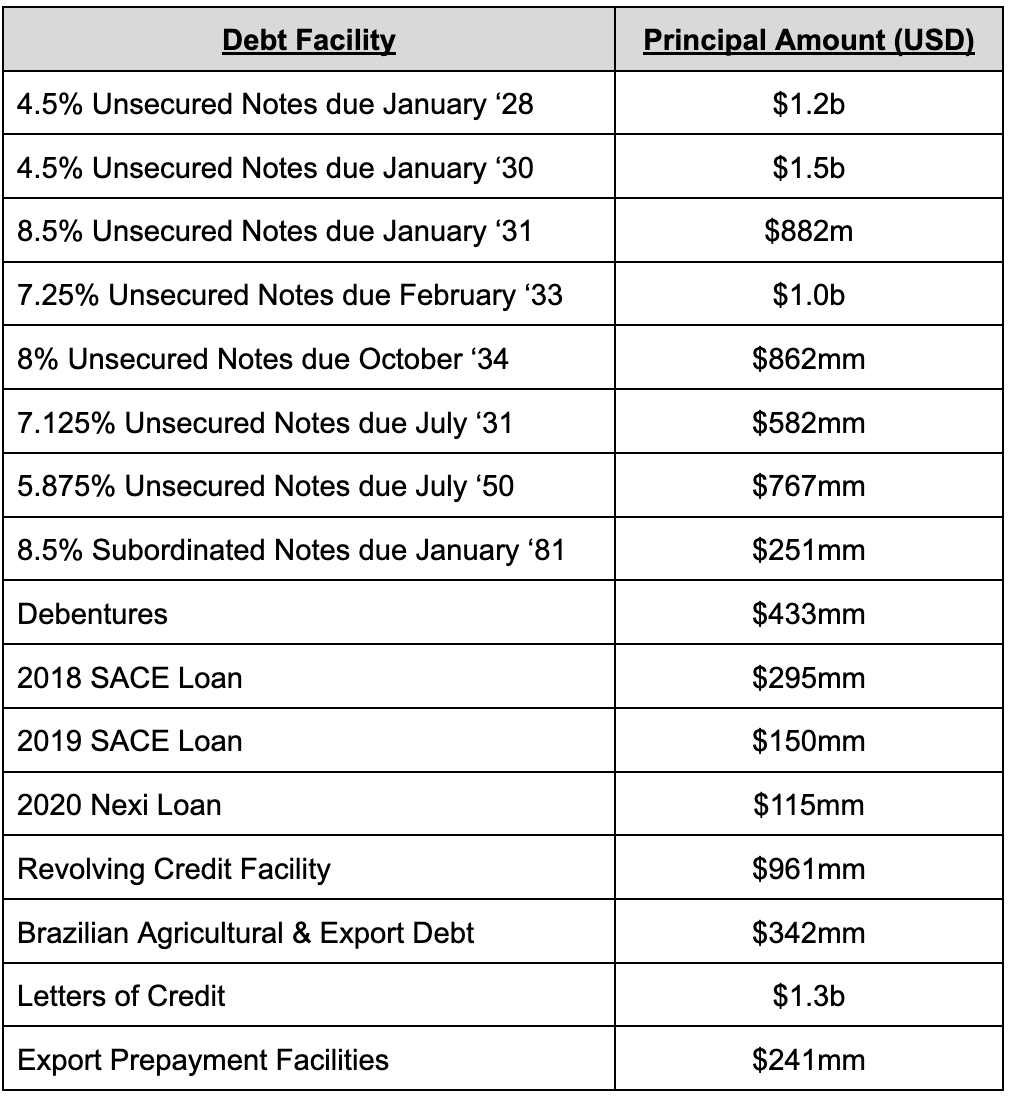

Of course, there are company-specific issues too. Namely, various interest and maturity obligations under funded debt — the straw that broke the camel’s back and which caused the company to file for a court-supervised mediation process in São Paulo on June 24, 2026 in anticipation of either a further Brazilian extrajudicial proceeding or a judicial reorganization. Here’s the ~$11b USD cap stack — most of which is pricing generally in the low 60s as of July 6, 2026:

The resolution of which we guess we’ll mark as “TBD.”

The company asked its creditors to extend credit lines and suspend collection efforts, but in its view, too few were interested.

Two creditor groups had their own take. The first is a Davis Polk & Wardwell LLP (“DPW”)-repped ad hoc group (the “AHG”), which chimed in with a simple reservation of rights decrying the company’s efforts. The AHG formed in the fall of ‘25 and has been clamoring for attention ever since, but the company “… only began any substantive discussion with members of the Ad Hoc Group this month …” — aka June ‘26 — “… and those interactions have so far been limited.”

Typical debtor bullsh*t — acting like 11th hour efforts count the same — but nothing out of the ordinary.

The second, composed of FFI Fund Ltd., FYI Ltd., and Olifant Fund, Ltd. (collectively, the “holders”) and represented by Paul Hastings LLP (“PH”), likely experienced the same. However, the holders didn’t just b*tch; they got us amped for a potential fight.

Sadly, 😩, via another reservation of rights. The foreign rep punted to the future by revising the proposed provisional relief order, 👎.

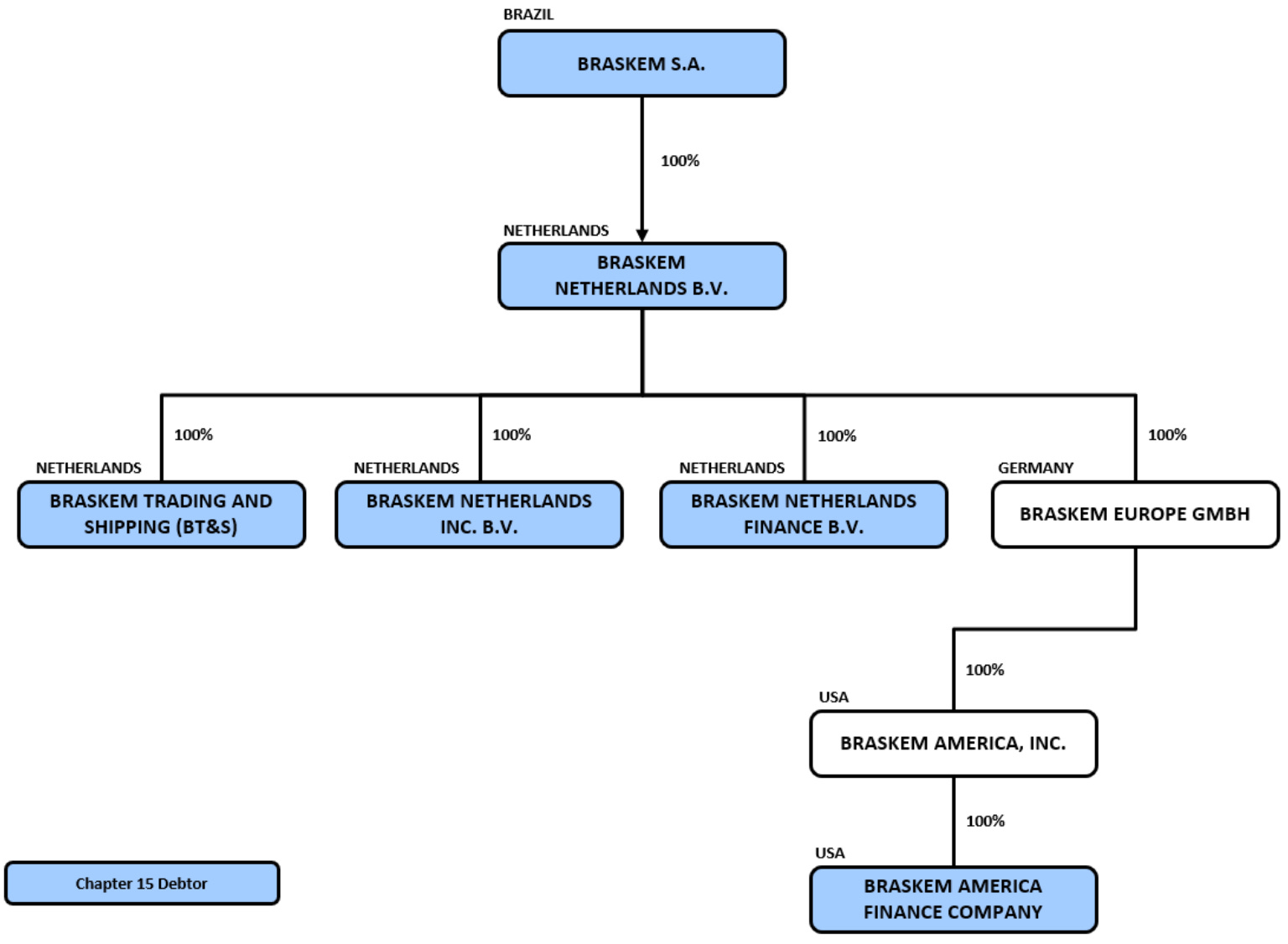

Anyway, here’s the meat. The company’s ‘41 notes were issued by debtor Braskem America Finance Company (“US FinCo”), which, per the foreign rep’s own words, is “… a wholly owned subsidiary of non-debtor, Braskem America, Inc. [‘Braskem Parent’]…,” “… was formed for the sole purpose of raising and managing funds on international markets to fund the activities of the operational components of the Braskem Group,” and “… is incorporated in Delaware and has its registered office in Wilmington, Delaware.”

Who benefited directly from the issuance? Why, non-debtor obligor Braskem Parent, another US entity with US headquarters, which, per the holders, is “… a solvent operating company that is not before this Court and is not a party to the Brazilian mediation proceeding.”

Therefore, they go on:

“Every objective indicator of US FinCo’s identity points to the United States: its Delaware incorporation; its direct Delaware parent’s headquarters in the United States; its only debt instruments being governed by New York law with a New York forum selection clause with an indenture trustee located in the United States; its assets consisting of intercompany claims against its United States parent.”

Followed by the kicker:

“… the Holders do not believe the Brazilian mediation proceeding—or any subsequent proceeding under Brazilian law—can or will be recognized with respect to US FinCo. The Holders reserve all rights to oppose recognition and to argue that any restructuring of US FinCo should proceed under Chapter 11 of the Bankruptcy Code, where US FinCo’s creditors would have the full protections of Chapter 11 bankruptcy law and the oversight of a U.S. bankruptcy court with jurisdiction over all property of US FinCo’s estate.”

Fun. Interesting too!

For another day though. On June 30, 2026, the court took up and granted then-uncontested provisional relief, and the recognition hearing won’t be happening until September 15, 2026 at the earliest. In the interim, Judge Wiles will hold a status conference on August 18, 2026 at 2pm ET.

The debtors are represented by E. Munhoz Advogados (Ana Elisa Laquimia) as Brazilian legal counsel, while the foreign rep is represented by Cleary Gottlieb Steen & Hamilton, LLP (Richard Cooper, Thomas Kessler, David Schwartz) as US legal counsel. The ad hoc group is represented by DPW (Timothy Graulich, David Schiff, Abraham Bane, Moshe Melcer) as US legal counsel. The holders are represented by PH (Daniel Fliman, Sayan Bhattacharyya, Robert Nussbaum) as legal counsel.

*EBITDA took a hit too. In 4Q’25, recurring EBITDA for the Brazil/South America segment fell 30% from the previous quarter to $143mm USD, while the US and Europe segment recorded, 😬, negative $32mm USD for the same period.

Company Parties:

Brazilian Legal: Brazilian Legal: E. Munhoz Advogados (Ana Elisa Laquimia)

Foreign Representative: Antonio Reinaldo Rabelo Filho

US Legal: Cleary Gottlieb Steen & Hamilton, LLP (Richard Cooper, Thomas Kessler, David Schwartz, Timothy Wolfe)

Claims Agent: Epiq (Click here for free docket access)

Other Parties in Interest

Ad Hoc Group of Debtholders

Legal: Davis Polk & Wardwell LLP (Timothy Graulich, David Schiff, Abraham Bane, Moshe Melcer)

Other Debt Holders: FFI Fund Ltd., FYI Ltd., and Olifant Fund, Ltd.

Legal: Paul Hastings LLP (Daniel Fliman, Sayan Bhattacharyya, Robert Nussbaum)