💥 Inflation & Default Rates Rise💥

Sangamo Therapeutics Inc. ($SGMO) Files, Miyoshi America Inc. Proceeds, and Johnny Brings Back Links

As we write this, the United States and the Islamic Republic of Iran are back at it. Putting that itty bitty hiccup to peace aside, 🙄, the big news this week was inflation.

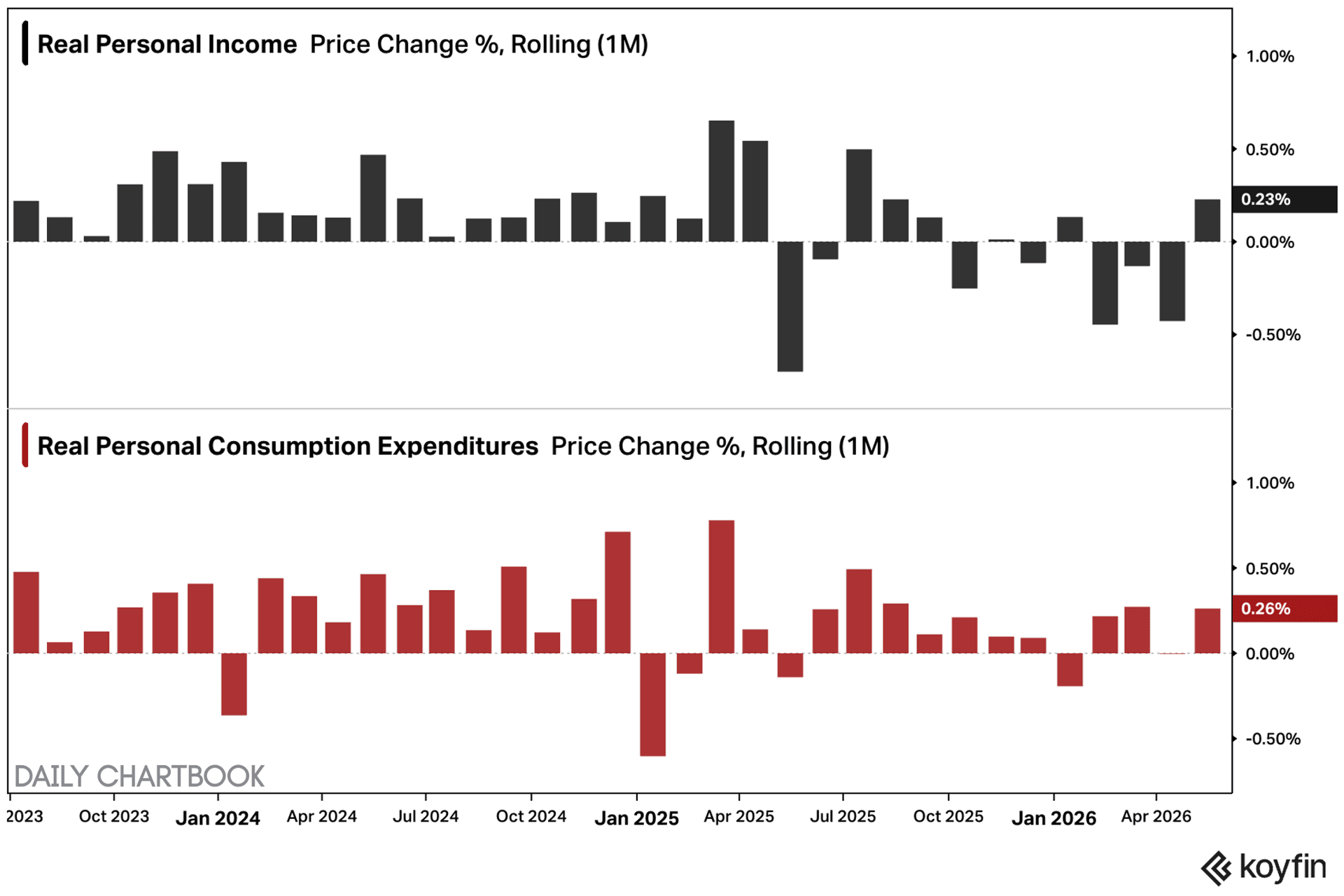

Headline PCE inflation accelerated to its highest reading in roughly three years. For its part, core PCE remained around 3.4% — the persistent f*cker.

Those damn RX fees are contributing to core services increases, 😉.

As noted by Johnny below 👇, the consumer, however, remains resilient and spending and personal income continue to increase, reflecting healthy household demand despite restrictive monetary policy.

The economy is apparently so good that TI models from the future are traveling back in time to feel today’s vibes, lol:

*****

Obviously these 👆 macroeconomic factors continue to contribute to what appears to be a dearth of meaningful RX activity.

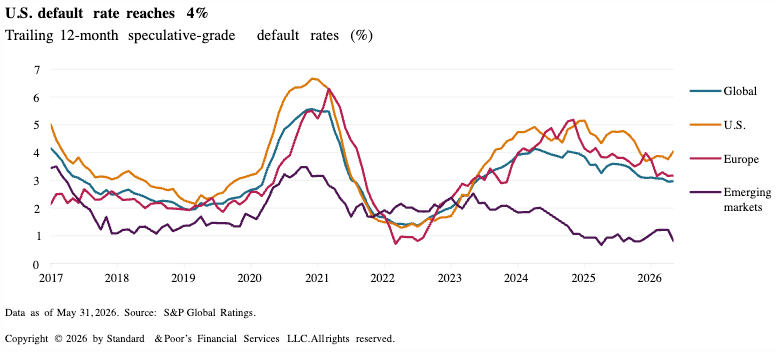

But last week S&P Global Ratings (“S&P”) issued its latest report titled “Default, Transition, and Recovery: Defaults Quadruple in May” and, despite the dearth of in-court activity out there, things are still happening — particularly defaults in the US.* The report states:

“Monthly default counts rose sharply to 17 in May, the highest monthly total since May 2025. This follows a multi-year monthly low of only four defaults in April (a level last seen in May 2022) and reverses a three-month declining trend. The spike in May coincided with a surge in U.S. defaults, which quadrupled to 12 from three in April, while European defaults also increased to four from one.

Despite the monthly spike, the year-to-date total of 45 remains below the five-year average of 54 and lower than the 53 defaults recorded over the same period last year. For now the data suggests volatility rather than a sustained spike though we expect global defaults to rise to 3.8% through March 2027.

Regionally, the U.S. is the only area where defaults have increased year over year, edging up to 32 year to date from 30 over the same period last year.”

The TTM US speculative grade default rate rose to 4% in May, up from 3.8% in April …

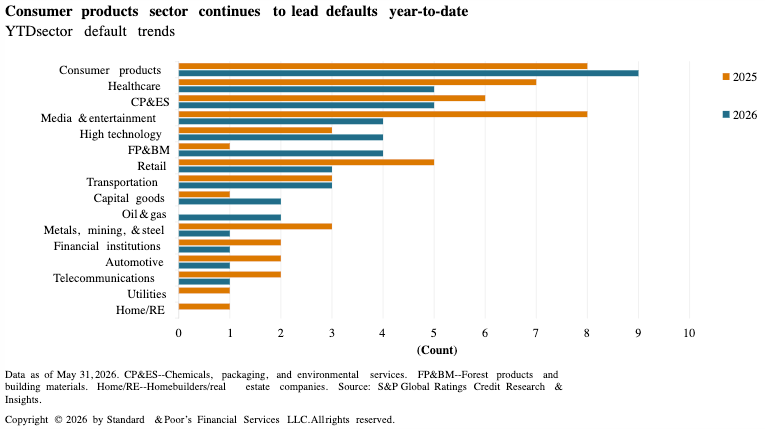

… buy May introduced a broader spectrum of affected industries:

Of course distressed exchanges are driving an obnoxiously large portion of the defaults. Per S&P:

“Distressed exchanges remained the leading cause of defaults in May, accounting for 47% of the total, followed by missed payments at 41%. The year-to-date pattern is similar, with distressed exchanges remaining the primary driver of defaults, representing 44% of total defaults. However, the share of distressed exchanges has declined compared with the same period last year (58%). This reflects a drop in the number of distressed exchanges to 20 over the first five months of 2026, from 31 during the same period last year.

There were six repeat defaults in May, 35% of the total defaults, the highest monthly number since December 2025. There were four repeat defaults in the U.S., spread across four different sectors. Year-to-date, the count of repeat defaults is 19, accounting for 42% of the total defaults, the highest proportion since 2019.”

This ought to provide ammo to those who increasingly believe LMEs are a waste of motherf*cking time and money.

*The US defaults included Jeeps RealTruck Inc., United PF Holdings LLC (a Planet Fitness franchisee), Sensience Inc., West Technology Group LLC, BW Homecare Holdings LLC, Cabinetworks Group Inc., Oscar AcquisitionCo LLC, Emerald Technologies AcquisitionCo., Ingenovis Health Inc., Conair Holdings LLC, and Optiv Inc. Fitch Ratings also observed the action.

💥New Chapter 11 Bankruptcy Filing - Sangamo Therapeutics Inc. ($SGMO)💥

On June 23, 2026, Cali-based neurology-focused genomic medicine company Sangamo Therapeutics ($SGMO) (the “debtor” and along with three wholly-owned non-debtor subsidiaries, the “company”) filed a chapter 11 sale case — with two stalking horses teed up! — in the District of Delaware (Judge Goldblatt). You know we love these science-y cases!!

Actually, in case you don’t really remember: we don’t.

We REALLY don’t.

In fact, we hate these types of cases so much that we’re going to let that there 👆description of the company — yes, those five lonely words, “neurology-focused genomic medicine company” — be the sum total of our company-description. Though 👏🏼 to Cooley LLP’s Cullen Speckhart for providing as comprehensible an explanation of the debtor’s history, product line and future prospects at the June 24th first day hearing as humanly possible. Want to know more? Want to be a buyer? Read this. And spare Johnny a therapy appointment (or three).

The upshot is that this filing is teed up to be a series of sales. One, there’s a proposed sale of what the debtor calls its “Technology Platforms” and the “Prion Disease Program” to Eli Lilly and Company ($LLY)(“Lilly”) as stalking horse for $50mm (via a wholly-owned acquisition sub dubbed Merope Acquisition Sub LLC). Two, there’s a proposed sale of what the debtor has dubbed its “Fabry Disease Program” to Astellas Gene Therapies, Inc. (“Astellas”) for $25mm upfront plus a potential $25mm upon the debtor hitting certain milestones. And, three, there’s everything else (the debtor’s Chronic Neuropathic Pain Program, Hemophilia A Program, the Sickle Cell Disease Program, and the Tregs Platform). There’ll be a post-petition sale and marketing process for the whole kitten caboodle pursuant to a bidding procedures motion the debtor already has on file (on attempted shortened notice to boot, discussed 👇). That said, the debtor, as Ms. Speckhart put it, “…is open to all potential restructuring pathways, including reorganization structures and M&A transactions, and we will begin to assess [the debtor’s] options through the sale process where Lilly and Astellas will help us set the floor for what we anticipate will be a competitive bidding environment.”

To power this process, the debtor has a $30mm new money DIP term loan committed to by Northridge ATM LLC (“Northridge”)($10.5mm interim).* Great, right? Even better is that there are competing DIP proposals here that teed up quite a bit of 11th hour drama for the debtor and Ms. Speckhart’s team in the days leading up to the filing. Indeed, a company called Future Solutions Investments LLC (“FSI”) reached out, initially with a non-binding DIP term sheet, but the company’s restructuring committee ultimately decided that it was too late and too risky to change DIP lenders at that late juncture — particularly in light of the intertwined sequencing of APAs with Lilly and Astrellas, and the debtor’s dire cash position.** After the cases filed, however, the committee re-engaged with FSI (at FSI’s request) and FSI provided a binding term sheet, redlining its offer against what the debtor had already filed with the court re: Northridge with some improved economics (discussed 👇).

FSI allegedly wasn’t done; it also indicated, at least according to Ms. Speckhart, that it would be interested in becoming the owner of 100% of the debtor’s equity — in part to take advantage of the company’s significant net operating losses. Hence the statement, “open to all potential restructuring pathways.”

Given this, a good portion of the first day hearing dealt with the DIP motion. After a clean if not somewhat robotic presentation by Cooley’s Olya Antle in which, among other things, Ms. Antle noted DIP economics that include, as highlights, a 12% interest rate (cash, monthly), a 2% commitment fee (or $600k, upon interim), a 5% exit fee (or $1.5mm, upon interim) and a $75k one-time work fee that had already been paid prior to the petition date,*** FSI’s counsel, KTBS Law LLP’s Nir Maoz first took issue with Ms. Antle’s contention that the debtor’s had run a truly competitive DIP process before subsequently (even-more-robotically) delving into how he believed that FSI’s DIP proposal was “better.” Specifically, he noted a reduced interest rate from the proposed 12% to 11% and the elimination of the commitment and exit fees ($2.1mm in savings — BOOM!); he also indicated willingness on FSI’s part to waive any mandatory pre-payment premium which would, of course, provide the debtor with the flexibility it clearly desires to run its process.****

Game over, right?

Not so fast. Sh*t be intertwined, remember? Also, as a third-party with no other interest in the case, FSI didn’t exactly have the best standing argument to pursue some sort of objection.

But still — there were those interim fees! They could prejudice the process!! And before an official committee got appointed!!! And so Judge Goldblatt took issue with the commitment and exit fees sought as final relief at the interim stage. He said he could grant them but that they’d be subject to reversal later. Which, uh, kind of perplexed people a bit about the meaning of “final.”

And so a back-and-forth ensued between Ms. Antle, the United States Trustee (“UST”), Judge Goldblatt and the winner in all of this, Norton Rose Fulbright US LLP’s Robert Hirsh, who, reading the tea leaves on behalf of Northridge, acted quickly on his feet, and suggested that the $600k commitment fee and the 5% exit fee both be approved on a final basis, but the latter only with respect to the $10.5mm amount granted on an interim basis. After a brief break, Judge Goldblatt was (kinda sorta) cool with that, made his findings, and approved the interim DIP as modified. An order hit the docket a day later on June 25, 2026.

The last order of business was the motion to shorten time on the bid procedures which the UST had an issue with — again, due to a lack of committee. Sympathetic to the UST’s view, Judge Goldblatt asked counsel to cite a case where bid procedures were approved on shortened notice so early in a case and before committee formation and Ms. Antle be like …

… to which Judge Goldblatt be like …