💥New Chapter 11 Bankruptcy Filing - GoHealth, Inc.💥

Health insurance marketplace enrolls for prepackaged chapter 11 deleveraging

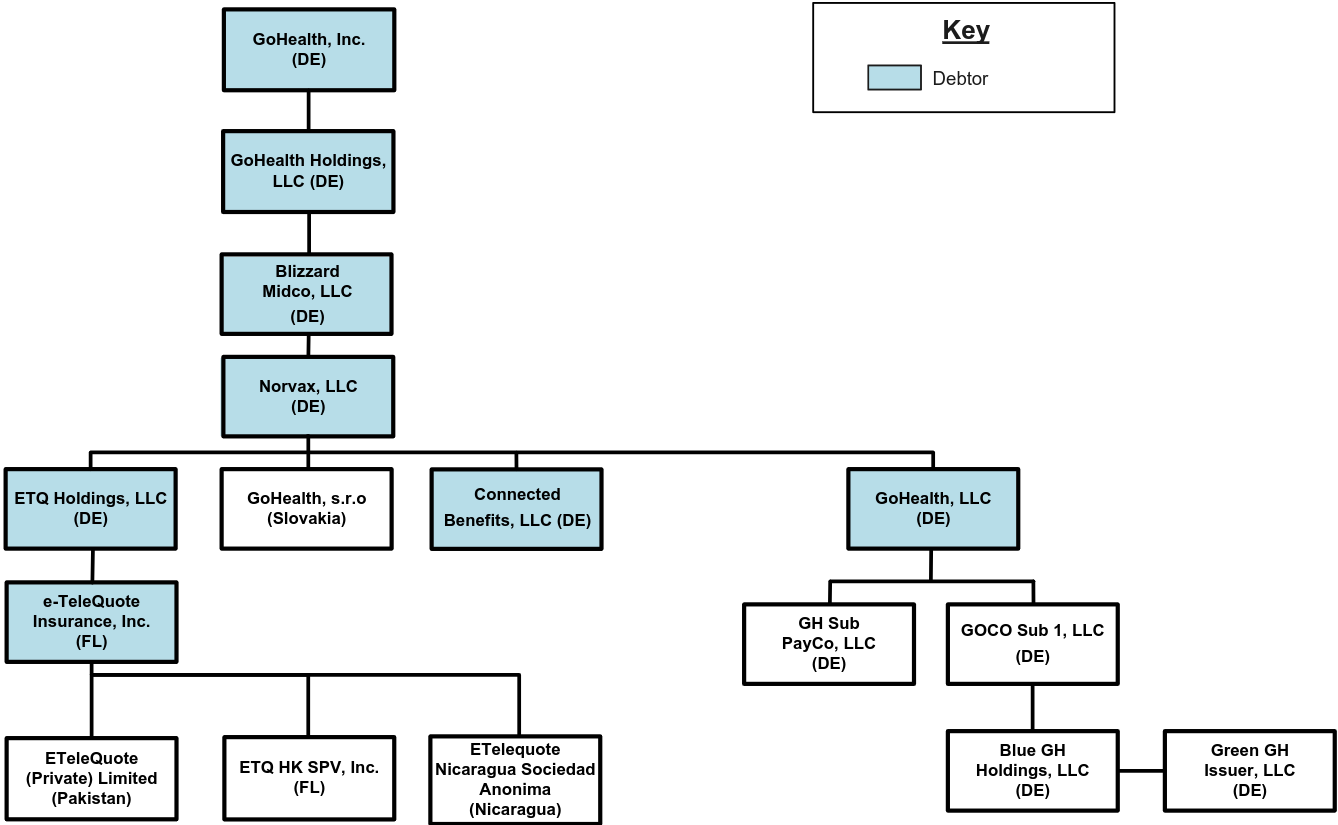

On June 7, 2026, CHI-based GoHealth, Inc. ($GOCO) and seven affiliates (collectively, the “debtors” and together with their non-debtor affiliates, the “company”) filed prepackaged chapter 11 bankruptcy cases in the District of Delaware (Judge Horan). Founded in ‘01, the company has been a health insurance marketplace and “… Medicare-focused digital health company” since ~’12.

In ‘20, the company IPO’d on NASDAQ ($NDAQ). Per CEO Vijay Kotte, that itself is a leading reason for the BK:

“GoHealth raised over $900 million in connection with its IPO, with an initial valuation of approximately $6.6 billion, making it one of the largest healthcare IPOs of the year.

Unfortunately, GoHealth’s very success is what led to its challenges. GoHealth’s successful IPO and lucrative business model inspired a wave of new entrants into the field, escalating competitive pressure.”

You hate to see it.

Too much winning.

With an increase in competition … wellllllllllllll … the coin flipped and the losing started:

The company has, however, taken steps along the way to slow the beckoning of bankruptcy court. In ‘22, it raised ~$50mm by issuing perpetual pref equity (the “pref equity”) to its largest customers and tweaked the business model to incorporate marketing for insurance carriers to acquire new customers.

Sound like a great move? Initially it was … then it trailed off because customer acquisition costs got too high and the cost of keeping those customers covered kept pace.

Bad for business all around, but made worse by the US Department of Justice inserting itself in May ‘25. It sued insurance companies and brokers — including, lol, the company — for that aforementioned marketing, as well as administrative fees, opting to describe ‘em as a “kickback.”

And yeah, yeah, the company denies the allegations, intends to “… vigorously defend …” against them, which is 100% the expected response. Talk is cheap.

You know what ain’t? Actually defending. It led to a going concern (“GC”) qualification in 2Q’25.

That’s when, in June ‘25, Kirkland & Ellis LLP (“K&E”), Alvarez & Marsal North America, LLC (“A&M”), and Moelis & Company ($MC)(“Moelis”) — the last of which is conspicuously absent in the BK* — stepped in. Two months later, in early August ‘25, they “helped” the company LME its capital structure, adding $82mm in new cash to the balance sheet and rolling up ~$35mm of already-existing revolver debts, which was, apparently, a sufficient “… show of stability …,” 🙄, to drop the GC qualification the next quarter.

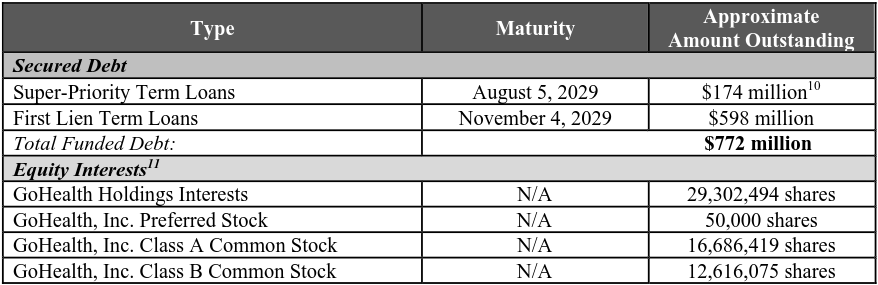

That “show of stability” lasted … um … until year end. Come 1Q’26 — ten months post-LME — the qualification reappeared, and the company filed with this petition-date capital structure 👇:

Miraculously, though, this ain’t your typical, 🍩-doling chapter 11. The debtors’ BK proposition has the support of 100% of their prepetition lenders, 61% of their class A common stock holders, and 99%+ of the holders of equity in GoHealth Holdings, LLC (“holdings”), which is a roundabout ways to say the co.’s pre-IPO equity holders, and under the debtors’ proposed chapter 11 plan and disclosure statement, the following will transpire: