📻New Chapter 22 Bankruptcy Filing - Cumulus Media Inc.📻

Audio-first media company files second chapter 11 case

On March 4 and 5, 2026, Cumulus Media Inc. (“CMI”) and forty affiliates (collectively, together with CMI, the “debtors” and together with their non-debtor affiliates, the “company”) filed widely-supported prepackaged chapter 22 bankruptcy cases in the Southern District of Texas (Judge Perez). The filing comes just shy of one year since our last update …

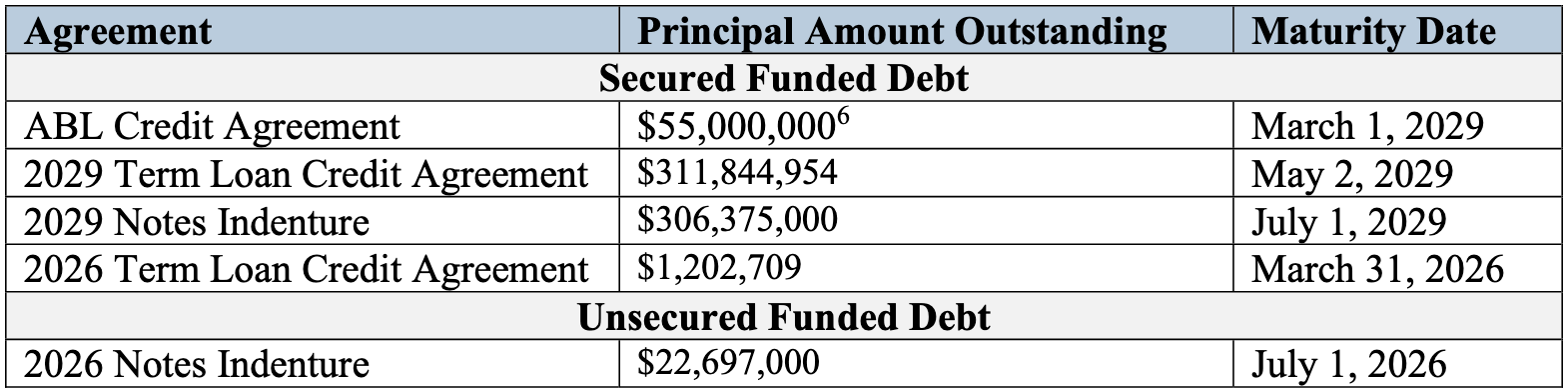

… about the “audio-first” media company, which not quite two years ago transformed its capital structure through a slight-discount-capturing and maturity pushing liability management exercise (“LME”) that converted (i) ~97% of an old ‘26 term loan into a senior ‘29 term loan (the “‘29 term loan”) and (ii) ~94% of unsecured notes due ‘26 into new senior secured notes due ‘29 (together with the ‘29 term loan, the “‘29 debt”), leaving the following petition-date debt stack:

Alas, radio and podcasts we’d never heard of …

… haven’t surged in popularity in the post-LME, post-COVID, WFH era.

In FY’24, the company reported ~$827.1mm in net revenue primarily derived from selling ad spots, a net loss of ~$283.2mm (including a $221.8mm impairment charge), and adjusted EBITDA of ~$82.7mm, all worse YoY from FY’23.

FY’25 looks to have been keeping with the trend. In the first nine months of the year, the company booked net revenue of ~$553.6mm (⬇️ ~9% YoY), a net loss of ~$65.6mm (⬆️ ~25.7% YoY), and adjusted EBITDA of $42.5mm (⬇️ ~26.2% YoY).

And it may get bleaker.

In late ‘24, Nielsen Audio (“Nielsen”), per CFO and first-day declarant Francisco Lopez-Balboa, “… the radio broadcast industry’s principal ratings service … [and] exclusive provider of national radio ratings data,” implemented a new “network tying” policy in a transparent attempt to gouge customers. Under it, customers with national network and local radio stations — e.g., the company — are required to purchase local ratings data in all markets in which they operate in order to fully access Nielsen’s national data. Data on which the company relies to sell its ad slots.

Obviously, this was no bueno for the company. A lot of its local markets aren’t economical, so outside of being forced into it, it would never purchase all that sh*t. The company attempted for a while to get Nielsen to give it a better deal, but nothing ever came from it. So in October ‘25, the company filed an antitrust suit in the Southern District of New York, which showed some signs of success. On December 30, 2025, the court entered a preliminary injunction against Nielsen, allowing the company to continue purchasing only what it needed. But then Nielsen appealed, and on February 3, 2026, the Second Circuit granted its request for a stay, reverting the two to their post-tying posture while the litigation trickles through the trial court.

Regardless, it’s probably fair to say that Nielsen is only a mitigating factor in the company’s need to file. The upcoming maturities on the ‘26 debt is likely the real driver, so here’s the plan to delever. Under a restructuring support agreement (the “RSA”) with an hoc group of holders of 72.05% of the 2029 debt* and exit ABL commitment papers with the lenders under the existing Fifth Third Bank, N.A. ($FITB)-agented facility, the company will:

📍Exit ABL. Roll the prepetition ABL into a $100mm exit ABL dollar-for-dollar. Note that there’s no intermediate DIP — we’ll get to that in a blip.

📍’29 Debt. For the secured portion of its claim,** each holder of ‘29 debt will receive its pro rata share of (i) $50mm in exit convertible notes, which pay interest, at the company’s election, at 10% PIK or 8% cash, and (ii) new common stock and special warrants — to be issued “… solely to the extent necessary to obtain the Federal Communications Commission’s approval of the Restructuring Transactions …” — that will constitute 95% of the reorg equity in the company, subject to dilution by a 10% management incentive plan. The debtors attribute a 96.5% recovery to this treatment.