💥Cautionary Tales💥

Updates: American Tire Distributors + ExacTech. Filings: iM3NY + Biora Therapeutics.

Dovetailing nicely with Andrew Glenn’s Notice of Appearance on Wednesday …

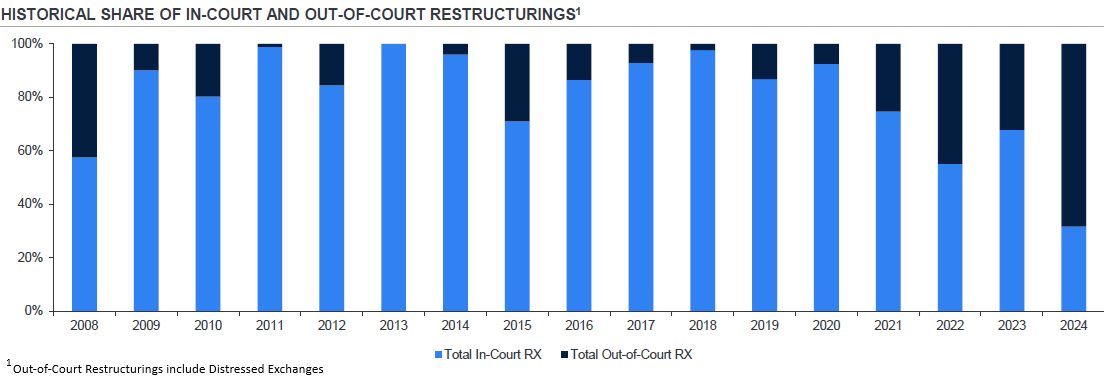

… we found these data points, courtesy of the fine folks over at J.P. Morgan Credit Research (“JPM”) and Akin Gump Strauss Hauer & Feld LLP (“Akin”), to be worth a read. This first one in particular illustrates Andrew’s cautionary tale quite well.

For the first time ever, out-of-court restructurings, including liability management exercises (“LMEs,” but penned as “distressed exchanges” in JPM’s materials), outpaced their in-court brethren in ‘24, coming in at over 60% of all dollars restructured. Perhaps at $2,650/hr, clients are looking more and more to avoid the standard fee gorging associated with in-court restructuring. The list goes on and on, but easy pickins include (i) early and unnecessary “first day” prep and burdensome diligence months, or even years, ahead of any realistic filing, all of which will go stale and need to be redone, (ii) endless tailored decks when off-the-shelf materials would serve just fine and cover 99%+ of use cases (fiduciary duty decks are especially egregious), (iii) needless board meetings at the behest of hourly billers to “update” the board that nothing of note had happened, (iv) overly long, unasked-for, and, frankly, questionable “research” memos digging down to bedrock on topics any restructuring professional worth his or her salt ought to know offhand, and (v) absolutely pencil-f*cked corporate minutes that every other legal practice group finds a way to do without (and, in any event, don’t stop litigants from seeking discovery).

Whatever the reason, LMEs are not only here to stay but trending upward.

Zooming back out, in- and out-of-court ‘24 restructuring activity addressed ~$84b of funded debt, with healthcare (22%), industrials (18%), tech (17%), and media and comms (14%) accounting for a hefty 71% of it.