💥Another Failed Liability Management Exercise (Trinseo)💥

New Filings: Trinseo PLC + West Marine LLC

We spent some time over the holiday taking stock of where things sit. The S&P 500 Index ripped over the several weeks heading into the holiday weekend — concerns about the Strait of Hormuz, higher gas prices, declining consumer confidence,* higher inflation, and about a thousand other factors that might otherwise indicate a lower market be damned. It’s up, as of market close on May 26, 2026, 9.63% YTD.

Why? Earnings have been feeding the beast. Q1 earnings crushed analyst expectations by 2x, and analysts are now playing catch up. Big tech and AI are leading the charge: the S&P 500 Index has been powered by a 28.7% EPS increase.** Narrowing the aperture, the iShares Semiconductor ETF ($SOXX) is up a staggering 172% — OVER THE PAST YEAR, 🤯.

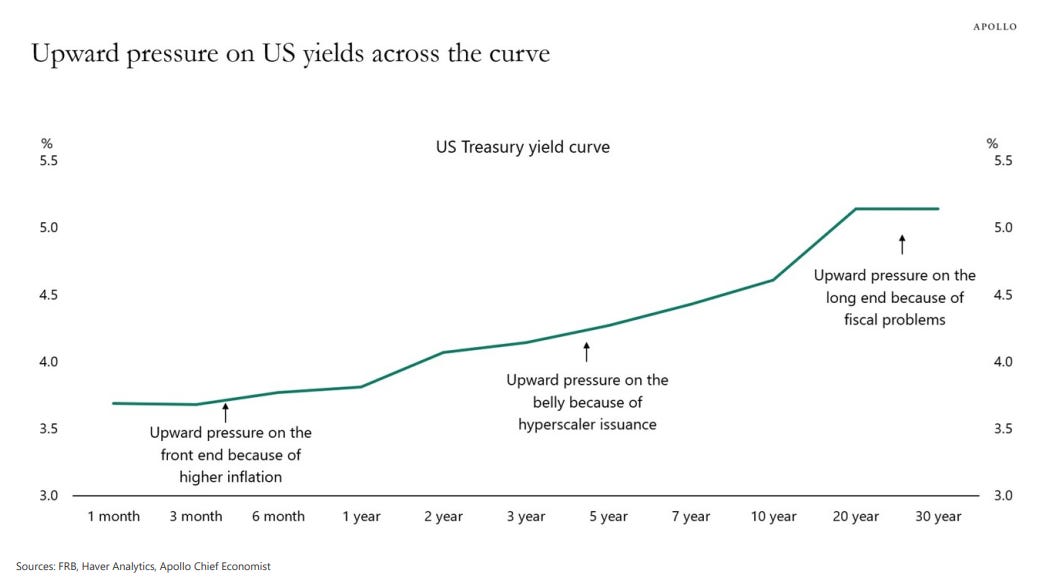

The bond market, however, be hiding in the corner waving red flags. The 30Y Treasury powered past the dreaded 5% level, hitting 5.18%, its highest mark since July of … wait for it … ‘07.

Interestingly, the Fed Reserve is turning over at precisely the time that it’s becoming clear just how badly Jerome POW-ell & the Gang failed to ever get the economy down to the Fed’s 2% inflation goal. US inflation has been over that target for five+ years running. Repeat: five+ years running. Nothing to see here folks! There’s no reason to think inflation is going down anytime soon either — especially as long as the situation with the Iranian regime persists. Even a “deal” — allegedly happening as we write this — appears to kick the can on some of the more fraught issues, e.g., nuclear enrichment and ballistic missile production. Reminder: the Strait was supposed to open after the last ceasefire. We all know how that played out.

The next Fed meeting — new Chairman Kevin Warsh’s first — is on June 17, 2026, and nobody should expect lower rates as a Father’s Day present given where inflation is.

The market is currently pricing in an over a 99% probability that rates remain stable. From there, things get interesting. The market is pricing in a not-insignificant ~11% chance of a 25bps rate INCREASE in July and, if not then, 28.3% for September and 34.5% for October. The market is also pricing in a ~4.4% chance increase to 400-425bps in October and, if not then, 10.6% chance it hits that level by December. That is NOT at all what President Trump had hoped for but that is, seemingly, what his war with the regime has gotten him.

And so we’ll cut the Fed a small break: it’s quite obvious that POW-ell and the gang didn’t have a war with the Iranian regime on their bingo card.

*****

As for the world of RX, things still sit … pretty quietly. Today we cover two situations everyone saw coming: Trinseo PLC and West Marine Inc. Let’s dig in.

*Notably, the University of Michigan index has never been this low. On Tuesday, The Conference Board released its consumer confidence index and it, too, showed that consumers are increasingly pessimistic.

**There’s been some — probably not enough — chatter about how this figure is in turn powered by profits from a select few companies, i.e., Meta Platforms Inc. ($META), Alphabet Inc. ($GOOG), and Amazon Inc. ($AMZN), while, all three companies marked holdings in AI companies at significant gains. Those positions aren’t liquid, however, and so there are some naysayers out there pointing to the fact that a bubble pop could reverberate through to these large players and, by extension, the Index.

💥New Chapter 11 Bankruptcy Filing - Trinseo PLC💥

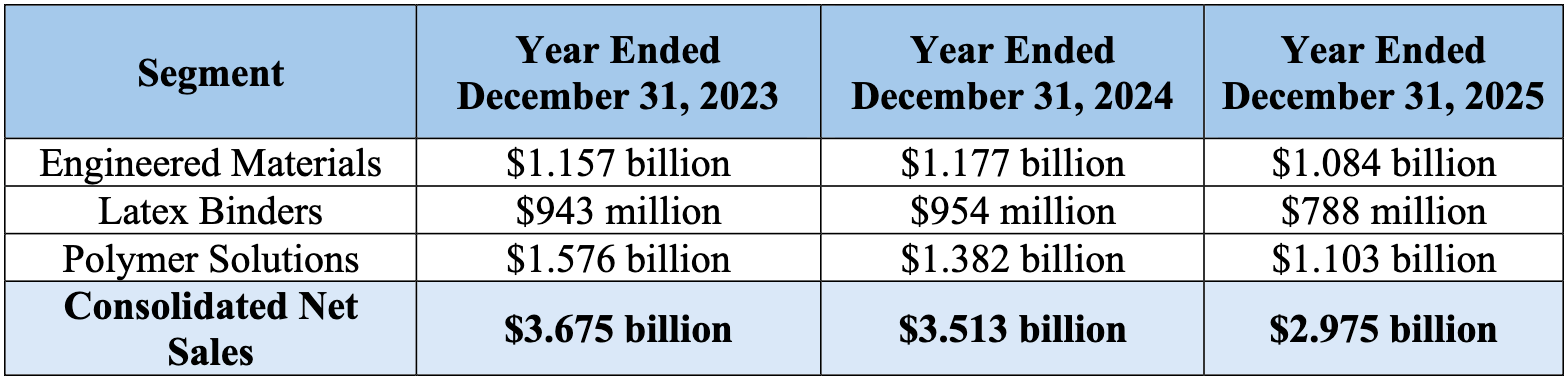

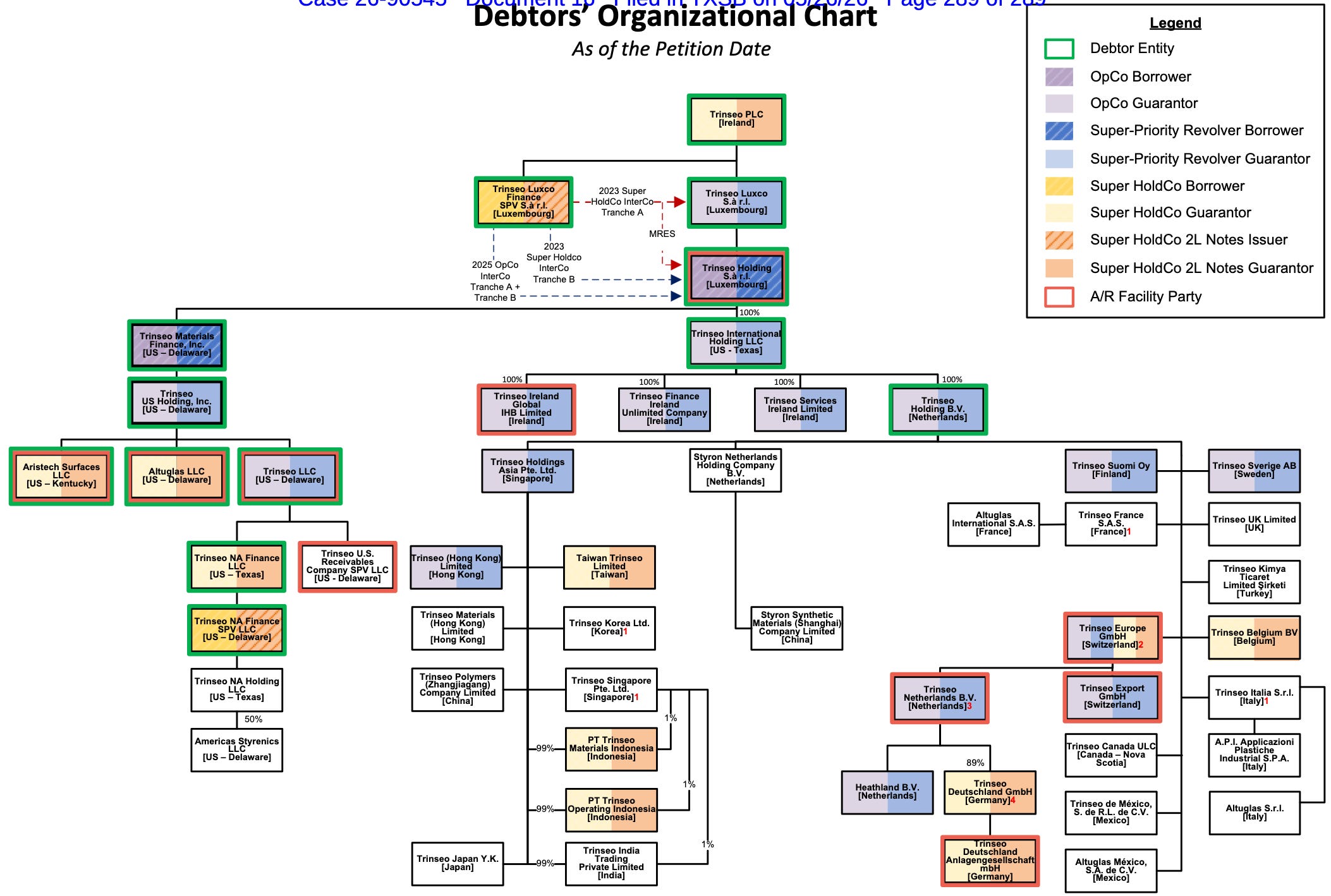

Welp, it’s time. After announcing entry into a restructuring support agreement (the “RSA”) earlier in the month, on May 26, 2026, Pennsylvania-based Trinseo PLC ($TSEOF) and twelve affiliates (collectively, the “debtors” and together with their non-debtor affiliates, the “company”) filed “prepackaged” chapter 11 bankruptcy cases in the Southern District of Texas (Judge Lopez). The company is a chemical manufacturer that makes plastics and latex binders used in everyday products and, since January ‘24, reports across three segments: (i) engineered materials, (ii) latex binders, and (iii) polymer solutions.*

The last few years, though, have been going the wrong direction … 📉:

Which is also reflected in the share price:

Overcapacity, fluctuating demand, tariffs, geopolitical conflict, rising interest rates, and energy pricing volatility are the company’s chosen culprits. Um … sure, that’s fine — we’ve read it all before and don’t really care tbh; the excuses ain’t interesting.

You know what is? This, per CRO Alan Boyko’s first day declaration:

“Although it was formerly a member of the ad hoc group of 2028 OpCo Term Loan holders that executed the RSA, CastleKnight Management LP (‘CastleKnight’), a holder of 2028 OpCo Term Loans and 2L 2029 Notes, has not executed the RSA and has advised that it will object to plan confirmation.”

In the first day dec no less.

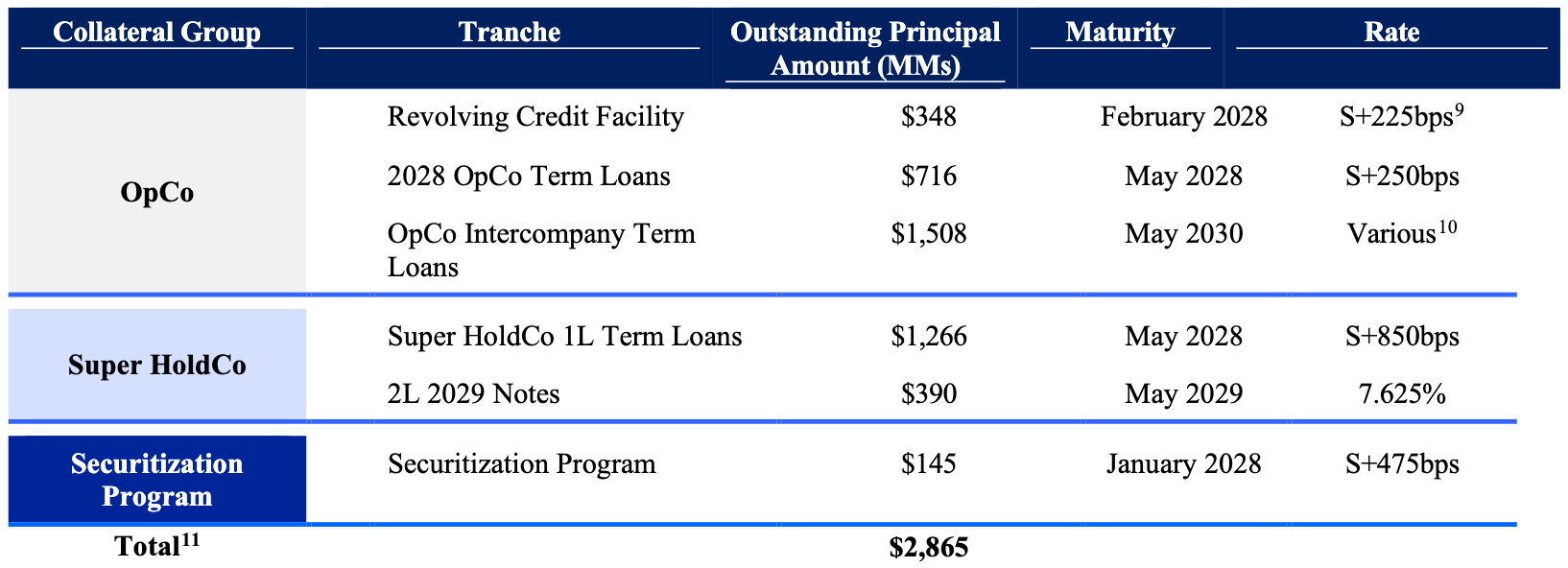

But why CastleKnight be beefing?** For that, let’s jump into the debt stack 👇:

Which is the result of two separate LMEs*** … creating a messy, messy capital structure:

The first LME occurred in September ‘23 when debtors Trinseo Luxco Finance SPV S.à r.l and Trinseo NA Finance SPV LLC (collectively, the “super holdco borrowers”) borrowed ~$1.1b and immediately on-lent ~$948mm of it via a double-dipping secured intercompany loan (the “interco opco TL”) to Trinseo Holding S.à r.l and Trinseo Materials Finance, Inc. (collectively, the “opco borrowers”), which sits pari with the already-issued ‘28 opco term loans noted above (the “‘28 opco TL,” and together with the interco opco TL, the “opco TLs”). The opco borrowers used the proceeds to (i) repay a then-existing $600mm term loan, (ii) pay down $385mm of $500mm (77%) of unsecured notes due September ‘25, and (iii) take care of professionals (💰).

The next came ~1.25 years later. In January ‘25, the company (i) refinanced its revolver into the one ☝️, allegedly elevating it above the opco TL in the process, (ii) redeemed the opco borrowers’ stub ‘25 notes left out in the earlier LME, which was financed by increasing the interco opco TL by $115mm, and (iii) exchanged ~$446.5mm in then-existing unsecured notes due ‘29, issued by the opco borrowers, for ~$379.5mm in new second-lien secured notes ‘due 29, issued by the super holdco borrowers (the “2L notes”).

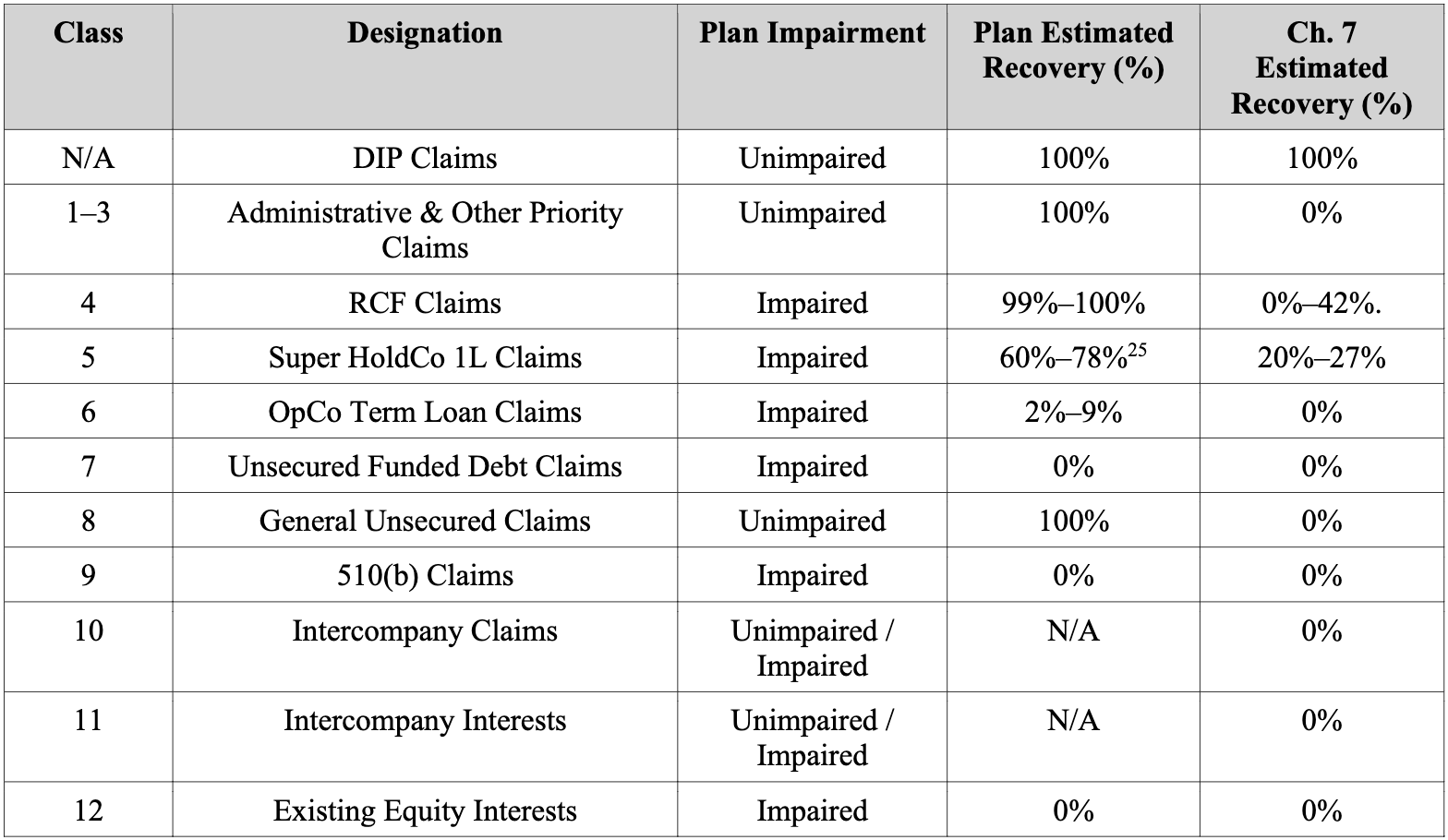

Hahahaha, lotta good the lien did. Here are the recoveries under the RSA, corresponding chapter 11 plan, and corresponding disclosure statement (the “DS”):

0% for the “unsecured funded debt” 2L notes. Adding insult to injury, junior GUCs go fully unimpaired. All ~$32.4mm of them.

Setting CastleKnight, which owns ~$271.8mm of the ‘28 opco TL and ~$93.5mm of the 2L notes, aside though, the RSA enjoys a sh*tload of support — 100% of the RCF, ~99.9% of the super holdco claims, and ~86% of the opco TLs, inclusive of ~57% of the ‘28 opco TLs — and provides:

📍DIP Financing. The funding of the cases through two DIP facilities. The first is a $157.5mm facility issued by the super holdco borrowers, composed of $52.5mm in new money ($35mm interim) and a 2:1, $105mm roll-up of the super holdco 1L term loans held by the DIP’s lenders.**** The second is a $270mm facility to be incurred by the opco borrowers, composed of $90mm in new money ($60mm interim) and a 2:1, $180mm roll-up of the prepetition RCF claims held by the DIP’s lenders.*****

📍Replacement of Securitization Program. The debtors create liquidity by selling A/R under a securitization program, and under the RSA, certain of the RSA parties agreed to refinance it, although the debtors did leave in the option for it to convert into an exit facility.

📍Equity Rights Offering. The economic main event. The debtors will offer $450mm in an equity rights offering (the “ERO”). 36.99% of it will go to super holdco TL claims, for an aggregate all-in price of $209.25mm, while 10.74% of it will go to opco TL creditors — including RSA-signing super holdco lenders via the double-dip — for $60.75mm.

Meanwhile, RSA parties — i.e., not CastleKnight — will have the opportunity to backstop their respective slice of the ERO. For that service, (i) super holdco backstoppers will receive $5mm in takeback loans, an aggregate 6.66% of the reorg equity, and have 24.66% of the ERO reserved exclusively for them at a $139.5mm purchase price and, and (ii) opco backstop parties will receive an aggregate 3.79% of the reorg equity and have dibs on 7.16% of the ERO at a $40.50mm purchase price.

📍Plan Recovery. If you mathed above, you’d notice those figures only add up to 90% of the go-forward equity. The lingering 10% is in the super holdco creditors’ plan recovery, along with ~$810mm in take-back paper and, of course, their subscription rights. Meanwhile, alongside their respective ERO options, opco TL lenders will receive $35mm in take-back paper … provided that any allotment on account of the interco opco TL will be “gifted” to RSA parties on account of their ‘28 opco TL claims.

📍Exit Financing. The takeback debt will be incurred under a $850mm exit term loan facility and a post-exit revolver providing at least $200mm.

📍Intercompany Settlement. The legal big one. No double-dipping, double-LME case would be complete without a settlement of the interco opco TL and the two years of financial shenanigans. For that, you need *wink wink* independents, which for the opco obligors meant Elizabeth Abrams and Alan Carr and for the super holdco meant Jill Frizzley and Carol Flaton. Anyway, the settlement allows the interco opco LT claim, which flows through to the super holdco lenders, in the amount of ~$1.5b and grants releases all around. Well mostly. CastleKnight is explicitly carved out, lol. What a 🖕.

📍Milestones. The RSA requires entry of the final DIP order by June 30, 2026, entry of the confirmation order by July 25, 2026, and emergence by November 22, 2026.

All of which, if it goes off without a hitch, will wipe ~$2b of debt off the debtors’ balance sheet.

But it won’t, and it’s definitely enough time for CastleKnight and the other “excluded lenders” represented by Pallas Partners (US) LLP and Gray Reed (the “excluded AHG”) to start a fight. In fact, they already have. Late on the petition date, the excluded AHG filed its objection to DS approval, accompanied by an adversary proceeding (the “AP”). From the objection:

“The Excluded OpCo Term Lenders have commenced the Adversary Proceeding, taking direct aim at each one of these prepetition transactions that underpin the proposed Plan. If any one of them is found invalid, the proposed Plan falls apart.”

The AP is where the real action will take place. The excluded AHG seeks to unwind the two LMEs, recharacterize or equitably subordinate the interco opco TLs, and subordinate the “elevated” RCF.

For their part, the debtors will argue the loser-lenders are prohibited from objecting under various, LME-concocted intercreditor agreements, but hot damn, these cases are about to be contentious. And we all know Johnny is just here for the fireworks.

The first ones will go off later today. The first day hearing is scheduled for 1pm CT.

The debtors are represented by Latham & Watkins LLP (Ray Schrock, Ryan Preston Dahl, Benjamin Rhode, George Klidonas, Jonathan Weichselbaum, Jennifer Zhang, Brian Herskowitz, Sarah Burack, Hayden Cresson, James Scavone, Mitchell Levy, Margaret-Ann Toms) and Hunton Andrews Kurth LLP (Timothy “Tad” Davidson II, Philip Guffy) as legal counsel, FTI Consulting, Inc. ($FCN) (Alan Boyko) as CRO and financial advisor, and Centerview Partners LLC (Karn Chopra) as investment banker. The opco independent managers are Elizabeth Abrams and Alan Carr and are represented by Quinn Emanuel Urquhart & Sullivan, LLP as legal counsel and the suddenly busy Portage Point Partners LLC as financial advisor. The super holdco independent managers are Jill Frizzley and Carol Flaton and are represented by McDermott Will & Schulte LLP (Bradley Giordano, James Kapp III, Julia M. Beskin, Charles Gibbs) as legal counsel. Deutsche Bank AG New York Branch, as RCF agent, is represented by White & Case LLP (Scott Greissman, Joseph Brazil, Rob Bennett, Andrew Zatz) as legal counsel. GLAS USA LLC and GLAS Americas LLC, as the securitization program agent, is represented by Reed Smith LLP (Nicholas Vislocky, Richard Solow, Paul Moak, Tristan Sierra) as legal counsel. The securitization programs’ lenders, Angelo, Gordon & Co., L.P. and Oaktree Capital Management, L.P., are represented by Orrick Herrington & Sutcliffe LLP (Robert Trust, Jacob Herz, Nicholas Sabatino) as legal counsel. An ad hoc group of senior secured lenders is represented by Paul Hastings LLP (Kristopher Hansen, Christopher Guhin, Matthew Garofalo, Jason Pierce, Charles Persons, Schlea Masanz) as legal counsel and PJT Partners as investment banker. An ad hoc group of term lenders is represented by Gibson, Dunn & Crutcher LLP (Stephen Silverman, Keith Martorana, Jonathan Dunworth, Adeola Adeyosoye) and Howley Law LLP (Tom Howley, Eric Terry) as legal counsel and Lazard Frères & Co. as investment banker. An ad hoc group of 2L noteholders is represented by Paul, Weiss, Rifkind, Wharton & Garrison LLP as legal counsel and Perella Weinberg Partners LP as investment banker. Finally, the excluded AHG is represented by Pallas Partners (US) LLP (Duane Loft, Jill Forster, Brianna Simopoulos) and Gray Reed (Jason Brookner, Lydia Webb) as legal counsel.

*Through non-Debtor Trinseo NA Holding LLC, the company also owns a 50% stake in AmSty, a joint venture co-owned with Chevron Phillips Chemical Company LP and “… leading …” producer of styrene and polystyrene. That stake, which per CastleKnight produced “… average adjusted EBITDA of approximately $100 million per year and [paid] average annual dividends of $85 million …” is tied up in the LMEs too.

**Not just here. CastleKnight beefed from minority positions in this year’s United Site Services, Inc. and The LYCRA Company LLC too.

***In between the two LMEs, in July ‘24, certain of the debtors started selling their A/R to a non-debtor third party under the securitization program.

****The super holdco DIP bears interest at term SOFR + 9% (new money) or term SOFR + 8.5% (roll-up) and features a 3.5% PIK commitment fee and a 7.5% PIK put-option premium.

*****The opco DIP bears interest at term SOFR + 9% (new money) or term SOFR + 2.25% (RCF roll-up) and also features a 3.5% PIK commitment fee and a 7.5% PIK put-option premium.

🚤New Chapter 11 Bankruptcy Filing - West Marine, Inc.🚤

On May 17, 2026, West Marine, Inc. and seven affiliates (collectively, the “debtors”) filed prearranged chapter 11 bankruptcy cases in the District of Delaware (Judge Owens). The debtors are a retailer for boating supplies, fishing gear, marine equipment, etc, dating all the way back ‘68 when, per CEO Paulee Day, “… Randy Repass, a man who loved boating—but loved taking care of people even more— …”

“… took his father’s East Coast ropes business West …”

And while “[t]he early days of [the business] faced choppy waters …”

… Mr. Repass persisted, found success, and the debtors grew. At their height, they had ~287 locations, fueled by add-on acquisitions and the opening of ever-larger stores, including a — holy hell — 50,000 ft² Fort Lauderdale “superstore.”

Anyway, let’s jump forward to 2020. Predictable sh*t unfolded. Back to Mr. Day:

“… during the COVID-19 pandemic, the Company accelerated its growth strategy to meet increased demand driven by a shift toward outdoor recreation. The Company expanded its product assortment to include lifestyle and discretionary products that supported life on the water, including apparel, footwear, accessories, and water toys in a larger abundance than ever before. This expanded assortment marked a divergence from the core marine focus on which the Company was founded.”

But uh-oh:

“Soon after this expansion, however, consumer discretionary spending contracted. The Company experienced supply chain disruptions, and frequent, severe weather during peak boating seasons dampened demand, leaving the Company with aging inventory across a wide footprint.”

To address its then-existing capital structure, in March ‘23, the debtors executed a recapitalization with 100% of their then-existing lenders, which brought in ~$150mm in new money.

That bought the debtors, oh, about six months or so.

By September ‘23, they had burnt through the new cash, which necessitated another recap, again with 100% lender support, and brought in another ~$125mm.*

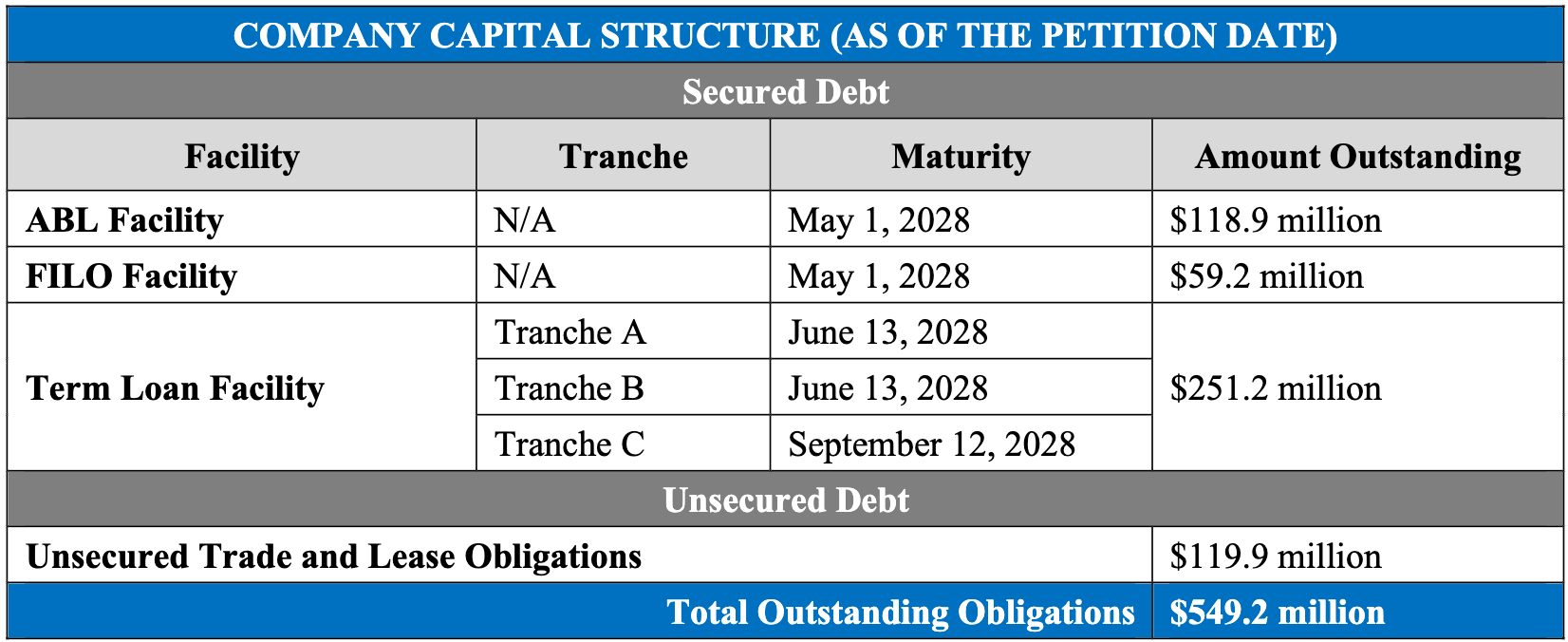

Sure as sh*t, the debtors burned through that too. So there were more and more borrowings via incremental ABL and term loan amendments in the nine-ish months leading up to the filing. As of the petition date, the debt stack looks like 👇:

Which, obviously, the debtors intend to restructure in chapter 11.

No, not by liquidating the retailer.

The debtors have a going-concern restructuring support agreement (the “RSA”). A well-liked one; the RSA — as well as the related chapter 11 plan and disclosure statement (the “DS”) — has the support of 100% of the FILO lenders, 96.2% of the term loan lenders, and 93.9% of equity interests and provides:

📍Payment of Claims. The equitization of 100% of the term loans in exchange for 100% of the reorg equity, subject to dilution by a MIP, and the payment in full of the ABL claims and the FILO claims or their conversion into not-quite-agreed exit facilities. If GUCs play along and vote in favor of the plan, they’ll also be treated to their pro rata split of $250k.**

📍New Money. Access to a committed, 🥜-sized $7.5mm post-emergence exit facility, which can be upsized another $2.5mm and has built-in capacity for up to another $15mm post-emergence.

📍Cash Collateral Usage. The consent of the debtors’ prepetition ABL agent and lender, Eclipse Business Capital LLC (“Eclipse”) for the usage of cash collateral during the cases, which, per the budget, is expected to be paid down ~$68.7mm by mid-August. That’s right, ladies and gentlemen, there’s no DIP here.

📍Marketing Process. Make no mistake: equitization is the default path, but the debtors, with the assistance of Triple P Securities, LLC d/b/a Portage Point (“Portage Point”), will try their hand at a marketing process and, if it bears fruit, toggle to a sale.

📍Timeline. “Try their hand” is generous. If Portage Point sources a bidder who diligences this thing we’ll be shocked: bids for any sales will be due by June 26, 2026, and the debtors will need to obtain either a confirmation order or a sale order by August 5, 2026, with the transaction closing no later than August 20. During that period, Hilco Merchant Resources, LLC and Hilco Real Estate, LLC (collectively, “Hilco”) will strong-arm landlords into lease concessions*** and liquidate any stores that don’t make it.

The court held the first-day hearing on May 19, 2026, which was, you know, supes uneventful. It clocked it at ~1.25 hours, during which Judge Owens granted all requested relief and scheduled the second-day and conditional DS approval hearings for June 11, 2026 at 2pm ET.

The debtors are represented by Kirkland & Ellis LLP (Joshua Sussberg, Matthew Fagen, Brian Nakhaimousa, Trevor Eck, Michael Esser) and Young Conaway Stargatt & Taylor, LLP (Michael Nestor, Kara Hammond Coyle, Shella Borovinskaya, Kristin Cardoza) as legal counsel, FTI Consulting, Inc. ($FCN) (Amir Agam) as financial advisor, Triple P Securities, LLC d/b/a Portage Point (Tosh Dhanala, Stephen Golmont, Steve Bremer, Ethan Retcher, Christopher Lukens) as investment banker, and Hilco (Eric Kaup) as real estate advisor and inventory liquidator. In turn, Hilco is represented by Womble Bond Dickinson (US) LLP (Marcy McLaughlin Smith). Matthew Kahn and Hugh Charvat are the debtors’ independent directors. An ad hoc group of consenting stakeholders is represented by Milbank LLP (Matthew Brod, Benjamin Schak), Otterbourg P.C. (Antonio Aguilera, Daniel Fiorillo, Nicholas Palazzolo, Matt Stockl) and Richards, Layton & Finger, P.A. (Michael Merchant, Brendan Schlauch, Zachary Javorsky) as legal counsel. Eclipse, as prepetition ABL agent and lender, is represented by Reimer & Braunstein LLP (Steven Fox, Janine Figueiredo) and Ashby & Geddes, P.A. (Gregory Taylor) as legal counsel and AlixPartners LLP (Kent Percy, Rodi Blokh, James Shen) as financial advisor. Wilmington Savings Fund Society, FSB, as prepetition term loan agent, is represented by ArentFox Schiff LLP (Jeffrey Gleit, Matthew Bentley, Justin Kesselman) and Morris James LLP (Eric Monzo, Jason Levin) as legal counsel.

*All-in, the two back-to-back LMEs equitized ~$660mm of then-existing debt, which led to a 36-page-long list of equity holders. While we won’t list them all, holders include AEA, Barclays, Crescent Capital, Evolution, Golden Tree, ICG, Oaktree, Onex Credit Partners, Octagon Investment Partners, Octagon Investment Partners, PIMCO, Rockford Tower, Silver Rock, Sound Point, SVP, and MJX.

**The debtors don’t seem particularly beholden to this figure. At the May 19, 2026 first-day hearing, K&E told the court that “… that’s kind of an opening negotiation with a creditors’ committee that we’re sure will be appointed.”

***As of the petition date, the debtors have ~200 leases that carry a collective ~$50mm in annual obligations.

📚Resources📚

We have compiled a list of a$$-kicking resources on the topics of restructuring, tech, finance, investing, and disruption. 💥You can find it here💥.

📤 Notice📤

Carl Comstock (Director) joined Cascadia from Intrepid Investment Bankers.

Don Clarke (Partner) joined Pashman Stein Walder Hayden PC from Genova Burns LLC.

Immanuel Zacharias Vorbach (Associate) joined Gibson Dunn & Crutcher LLP from Weil Gotshal & Manges LLP.

Justin Forlenza (Counsel) joined Latham & Watkins LLP from Kirkland & Ellis LLP.

Lorie Beers (Head of Restructuring and Special Situations) joined Cascadia from Intrepid Investment Bankers.

🍾Congratulations to…🍾

AlixPartners LLP on its acquisition of Canadian restructuring advisory boutique, KSV Advisory Inc.

Fox Rothschild LLP (John Penn, Gordon Gouveia, Michael Sweet, Stephanie Slater Ward) for securing the legal mandate on behalf of the official committee of unsecured creditors in the Wiser Solutions, Inc. chapter 11 bankruptcy cases.

Jessica Lauria (Director & Senior Advisor) for joining the Board of Directors of Ensis Partners.

Marc Beilinson (Director & Senior Advisor) for joining the Board of Directors of Ensis Partners.