☠️Judge Isgur Doesn't Dig the DeathTrap☠️

Texas Judge Signals a Potentially Worse Outcome for $WPG Common

Maybe, just not the way this ⬆️ schmo means….

For those of you who are new to us, Washington Prime Group Inc. ($WPG) is an owner, developer and manager of retail real estate, including enclosed and open air malls. Set up as a real estate investment trust (“REIT”), the company’s portfolio includes 102 shopping centers across the US, totaling 52mm square feet. You can find a whole bunch of previous coverage on it here…

…but the general upshot is that even pre-COVID-19, this sucker was struggling. Ultimately the pandemic was the icing on the cake and, well, here we are talking about a chapter 11 bankruptcy case.

The bankruptcy case is predicated upon an equitization transaction pursuant to which the WPG debtors will equitize a slug of unsecured notes and hand the holders of that debt the keys to the kingdom in the form of equity in the post-bankruptcy reorganized WPG entity to its pre-petition lender and plan sponsor, SVP Global. That said, the WPG debtors leave the door slightly ajar for a buyer to come in a la Hertz and make a play for the company. As of now, there hasn’t been a whole lot of noise about someone actually coming in and doing so. And so the WPG debtors are moving forward in an effort to expeditiously exit chapter 11 and focus on the future. Of course, to exit chapter 11, the WPG debtors will need to send out a disclosure statement and solicit votes on their proposed plan of reorganization and, thereafter, get bankruptcy court approval of the process and result.

On Monday, July 12, 2021, the Washington Prime Group Inc. ($WPG) debtors held a status conference and conditional disclosure statement approval hearing before Judge Isgur in the Southern District of Texas and it’s probably fair to say that it didn’t go the way the debtors had anticipated. We’re not sure they were expecting to hear phrases like “non-confirmable plan,” “unduly coerced,” and “really hard call coming up.” Yet they did.

Source: GIPHY

Without getting too into the weeds of the bankruptcy code, suffice it to say that most observers of bankruptcy situations are familiar with the “absolute priority rule” which spells out whether and how creditors are entitled to recoveries from a debtor’s estate. It is this provision in the bankruptcy code — 🙄 fine, we’ll cite it … section 1129(b)(2)🙄 — that requires that claims of a senior class of creditors be paid in full before any junior class of creditors may receive or retain any property in satisfaction of its claims. More plainly, secured creditors must get paid in full before unsecured creditors get paid a dime and so forth and so on down the capital structure such that unsecured creditors ought to get paid in full before stockholders get a penny. Similarly, preferred stockholders are senior in line to common stockholders.

And that’s where the rubber meets the road because usually — and we emphasize usually — stockholders don’t get f*ck all in bankruptcy. Recently, however, they have. And now “The Hertz Effect” looms large over other pandemic-era bankruptcies because, as the WPG debtors acknowledged out of the gate, it is awfully hard to value some of these businesses in light of potentially long-lasting pandemic-induced effects. The over-arching question here is: does WPG have equity value? And, if not, should equity be getting any sort of recovery whatsoever?

On the first question, the WPG debtors are clearly proceeding as if they don’t think so. The WPG debtors gave absolute no indication that any White Knight was close to galloping into bankruptcy court with a higher or better offer that takes out SVP Global and allows for value to flow through the capital structure.

Recognizing all of these factors and in a commendable attempt to avoid a big fight down the road, the WPG debtors here conjured up a scheme whereby both preferred and common shareholders are eligible for a recovery anyway — a “gift” of sorts, from the senior impaired consenting class. That eligibility, however, is contingent upon a multi-level “death trap” provision — a blatant quid pro quo where the prefs and common will only get something if they go along with SVP Global, the debtors, and the proposed equitization transaction by voting “yes” on the plan of reorganization.

Source: Primo GIF

A preferred shareholder took issue with this coercive tactic this week and found a sympathetic ear in Judge Isgur. Here are the scenarios at issue:

The preferred shareholders vote no on the plan. In this case, both the preferred shareholder class (Class 10) and the common shareholder class (Class 11) get bupkis. It doesn’t matter what the common do in that scenario.

If, however, the preferred shareholders vote yes on the plan and the common vote note no, the preferred will get either $40mm in cash or approximately 6% equity (subject to other caveats and dilution mechanisms).

If the preferred shareholders vote yes on the plan AND the common vote yes, the two classes will split the proposed “gift” recovery and each get $20mm in cash or approximately 3% equity.

It’s that last bit that concerned Judge Isgur. Notwithstanding the WPG debtors’ argument that anything either of these classes get is a “gift” in the equitization scenario, he suggested that the bankruptcy code may nevertheless preclude the last option because it fails to take into account the preferred shareholders’ liquidation preference over and above common equity. As he put it: the prefs either vote no and get nothing (lose) or vote yes and forfeit their liquidation preference and provide common with some sort of return (lose again). He indicated difficulty squaring that with Bankruptcy Code section 1129(b)(2)(C)(i) which, he argued, protects the liquidation preference before common is entitled to anything. The question then becomes: does that apply to a gift? This is where that “really hard call” statement comes in.

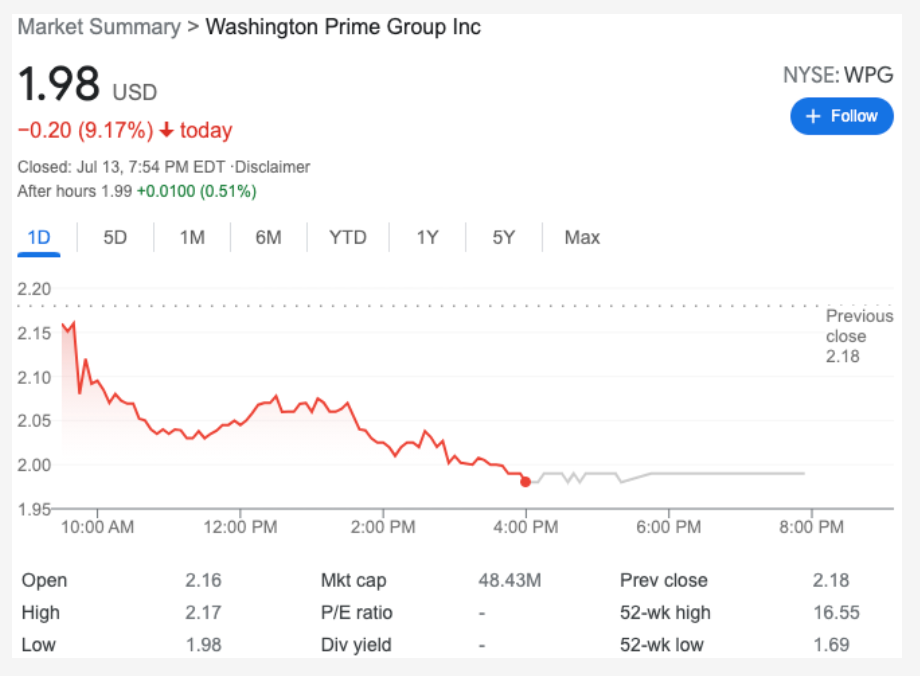

All of which begs the question: what does this mean for WPG common stockholders? Well, it ain’t good. Any WPG common shareholder who was of the view that there was a strong chance that they’d see some recovery may want to pay closer attention. It was clear that, as we initially took “pen to paper” here after market close on July 12, this already-ugly-AF chart may get a bit uglier if this issue doesn’t get sorted out (PETITION Note: even without this latest controversy, the stock appeared to be priced generously for some inexplicable reason. Markets be like 🤷♀️.).

Not that the memers comprehended that:

On July 13, the market got a bit wiser and the stock fell ~9%:

Interestingly, Judge Isgur — typically a champion for the little guy — insisted that the debtors file a revised disclosure statement that expressly acknowledges the possibility of a judicial finding that the proposed death trap violates the bankruptcy code. With that new language, he conditionally approved the disclosure statement. Ironically, his issue here, though, has the affect of screwing over the little guy, i.e., the common shareholders, and potentially precluding them from obtaining any recovery in the case. So, there’s that.

And so now we’re headed for a fairly vicious game of chicken going into a confirmation hearing. First, it goes without saying that the case is potentially setting up for a pretty rigorous valuation fight — especially if shareholders get organized (PETITION Note: the Office of the United States Trustee is currently soliciting interest in a committee and it sounds like there’s interest). Beyond that, the Judge showed an activist bent here, sparked in part by a preferred shareholder complaining about recovery going to common. Of course, there’s a beggars can’t be choosers element to this in that the WPG debtors could just decide that, given a valuation fight is on tap anyway, it may just make sense to pull a Lucy and rip that death trap option and any recovery right out from under all shareholders. After all, if there’s gonna be war anyway, why bother with dubious gestures for peace?