On its February 8th earnings call, the company stated:

“We are pleased to deliver results in line with expectations set forth at the beginning of the year notwithstanding the challenges that materialized.”

Translation: “we are pleased to merely fall in line with rock bottom expectations given all of the challenges that materialized and could have made sh*t FAR FAR WORSE.”

The company reported a 4.4% net operating income decline for the quarter and a 6% same-center net operating income decline for the year. The company is performing triage and eliminating short-term pressure: it secured a new $1.185b ‘23 secured revolver and term loan with 16 banks as part of the syndicate (nothing like spreading the risk) to refinance out unsecured debt (encumbering the majority of its ‘A Mall’ properties and priming the rest of its capital structure in the process); it completed $100mm of gross dispositions plus another $160mm in “sales” of its Cary Towne Center and Acadiana Mall; it reduced its dividend (which, for investors in REITs, is a huge slap in the face); and it also engaged in “effective management of expenses” which means that they’re taking costs out of the business to make the bottom line look prettier.

Given the current state of affairs, triage should continue to remain a focus:

“Between the bankruptcy filings of Bon-Ton and Sears, we have more than 40 anchor closures.”

“…rent loss from anchor closures as well as rent reductions and store closures related to bankrupt or struggling shop tenants is having a significant near-term impact to our income stream.”

They went on further to say:

“Bankruptcy-related store closures impacted fourth quarter mall occupancy by approximately 70 basis points or 128,000 square feet. Occupancy for the first quarter will be impacted by a few recent bankruptcy filings. Gymboree announced liquidation of their namesake brand and Crazy 8 stores. We have approximately 45 locations with 106,000 square feet closing.”

Wait. It keeps going:

“We also have 13 Charlotte Russe stores that will close as part of their filing earlier this month, representing 82,000 square feet.”

Earlier this week, Things Remembered filed. We anticipate closing most of their 32 locations in our portfolio comprising approximately 39,000 square feet.”

And yet occupancy is rising. The quality of the occupancy, however — on an average rental basis — is on the decline. The company indicated that new and renewal leases averaged a rent decline of 9.1%. With respect to this, the company states:

As we've seen throughout the years, certain retailers with persistent sales declines have pressured renewal spreads. We had 17 Ascena deals and 2 deals with Express this quarter that contributed 550 basis points to the overall decline on renewal leases. We anticipate negative spreads in the near term but are optimistic that the positive sales trends in 2018 will lead to improved lease negotiations with this year.

Ahhhhh…more misplaced optimism in retail (callback to this bit about Leslie Wexner). As a counter-balance, however, there is some level of realism at play here: the company reserved $15mm for losses due to store closures and co-tenancy effects on company NOI. In the meantime, it is filling in empty space with amusement attractions (e.g., Dave & Buster’s Entertainment Inc. ($PLAY), movie theaters, Dick’s Sporting Goods Inc ($DKS) locations, restaurants, office space and hotels. Sh*t…given the amount of specialty movie theaters allegedly going into all of these emptying malls, America is going to need all of those additional gyms to work off that popcorn (and diabetes). Get ready for those future First Day Declarations that delineate that, per capita, America is over-gym’d and over-theatered. It’s coming: it stretches credulity that the solution to every emptying mall is Equinox and AMC Entertainment Holdings Inc. ($AMC). But we digress.

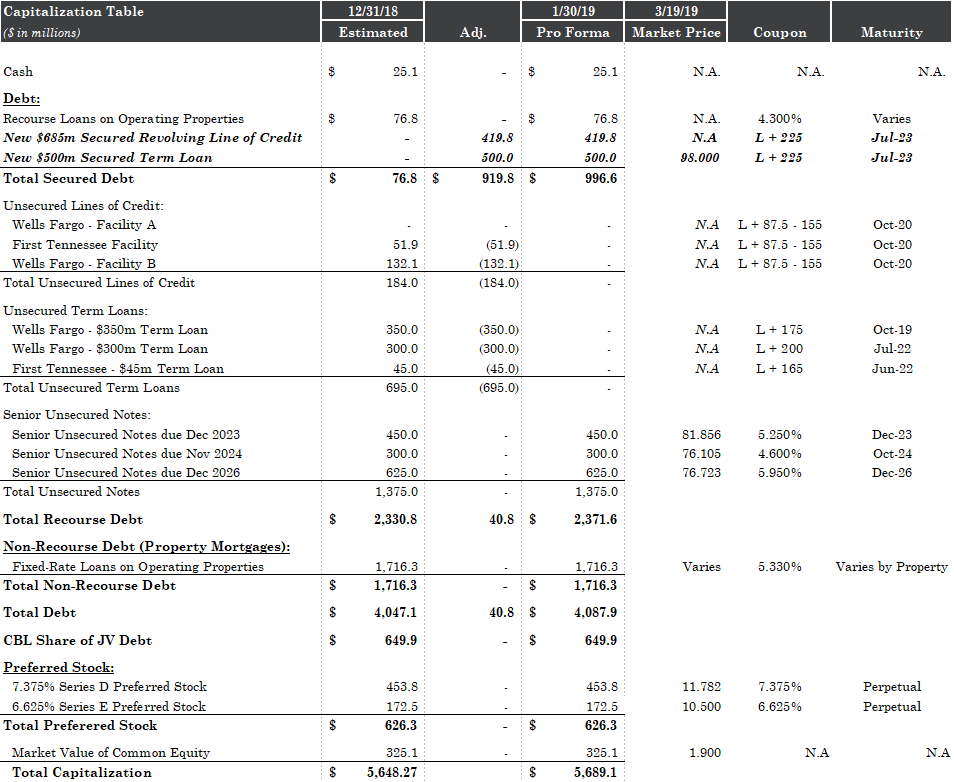

All of these factors — the average rent decline, the empty square footage, etc. — are especially relevant considering the company’s capital structure and could, ultimately, challenge compliance with debt covenants. Net debt-to-EBITDA was 7.3x compared with 6.7x at year-end 2017. Here is the capital structure and the respective market prices (as of March 19):