⛅The Rise of the Cloud. (Long Cloud Usage. Short Debt-Laden Intermediaries).⛅

The “cloud” is such a fundamental business component today that cloud considerations inform various aspects of business planning. Look no farther than Amazon Inc. ($AMZN), Microsoft Inc. ($MSFT), Cisco Inc. ($CSCO), and Google Inc. ($GOOGL), and you’ll see cloud computing providers who are minting money on a quarterly basis for providing services that alleviate the server and storage burden of businesses across all kinds of industry verticals. Underscoring the importance of the cloud, IBM Inc. ($IBM) spent a fortune — $34 billion! — acquiring Red Hat Inc. to boost its cloud-for-business offering. Furthermore, recent IPOs have illustrated just how important cloud services are: Pinterest Inc., Snap Inc. ($SNAP), Lyft Inc. ($LYFT), and many other high-flying companies pay hundreds of millions in fixed contracts for cloud computing services that power their applications in ways that everyday end users almost certainly don’t recognize and/or appreciate.

The “cloud,” however, subsumes various other services in addition to computing/storage. There are connectivity-focused applications (provided by the likes of AT&T Inc. ($T), Comcast Corporation ($CMCSA), and others) unified cloud communications applications (i.e., Vonage Holdings Corp. ($VG)), and point solutions (e.g., Citrix Systems Inc. ($CTXS)). One could be forgiven for thinking that everything and anything touching cloud would be gold in this environment. Imagine, for instance, if one firm could serve as an intermediary linking together various cloud-based solutions for other small, medium and large businesses!! Cha Ching!!

Apparently that’s not the case.

New York-based Fusion Connect Inc., “a provider of integrated cloud solutions, including cloud communications, cloud connectivity and business services to small, medium and large businesses” is bucking the hot cloud trend and barreling quickly towards a bankruptcy court. This begs the question: what the holy f*ck? How is that even possible?

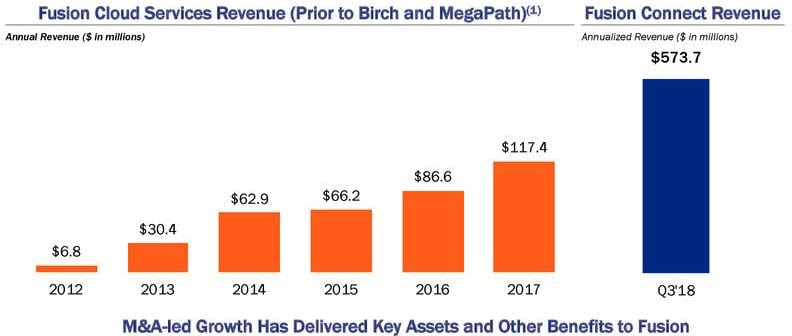

Per a January investor presentation, this is Fusion’s cloud services revenue:

The 2018 revenue is annualized: revenue in Q3 ‘18 was actually $143.4mm with gross margins of 49.1%. Net operating income was $4mm. Yet the company lost $0.23/share. How does that work? Well, the company had $21.6mm in interest expense.

The weighted-average rate of interest across the company’s credit facilities is approximately LIBOR + 7.7%. 😬 Not exactly cheap. Compounding matters is that the debt isn’t exactly cov-lite (shocking, we know): rather, the company is subject to all kinds of affirmative and negative covenants. Yes, once upon a time, those did exist.

The company’s recent SEC reports constitute a perfect storm of bad news. On April 2, the company filed a Form 8-K indicating that (i) a recently-acquired company had material accounting deficiencies that will affect its financials and, therefore, certain of the company’s prior filings “can no longer be relied upon,” (ii) it won’t be able to file its 10-K, (iii) it failed to make a $7mm interest payment on its Tranche A and Tranche B term loan borrowings due on April 1, 2019, and (iv) due to the accounting errors, the company has tripped various covenants under the first lien credit agreement — including its fixed charge coverage ratio and its total net leverage ratio. Rounding out this horror show of news, the company disclosed that it may need to seek a chapter 11 filing (combined with a CCAA in Canada) and has hired Weil Gotshal & Manges LLP, FTI Consulting Inc. ($FTI) and Macquarie Capital USA Inc. to advise it vis-a-vis strategic options. B.Riley/FBR ($RILY) analyst Josh Nicholsimmediately downgraded the company from “buy” to “neutral” (huh?!?) with a price target of $0.75 from $9.75. Uh, okay:

This is why you should never listen to equity analysts. This is the stock chart from the past year:

Like, the stock has been nowhere near $9.75, but whatevs.

On Monday, the company filed another Form 8-K. The company and 18 of its affiliated bankrupt US debtors…uh, we mean, guarantors…entered into a forbearance agreement with lenders under the Wilmington Trust NA-agented first lien credit agreement. The lenders will forbear from exercising rights and remedies stemming from the company’s defaults until April 29. The company had to pay 200 bps for the time to try and work this all out and agree to pay a slew of lender professionals, including Greenhill & Co. Inc. ($GHL) and Davis Polk & Wardwell LLP for an ad hoc group of Tranche B term lenders, Simpson Thacher & Bartlett LLP for the lenders of Tranche A term loans and the revolving lenders, and Arnold & Porter Kaye Scholer for Wilmington Trust.

The company’s Tranche B term lenders include East West Bank, Goldman Sachs, Morgan Stanley, Onex Credit Partners, Oppenheimer Funds and a whole bunch of CLOs. The latter fact may make a debt-for-equity swap interesting (PETITION Note: most CLOs are unable to hold equity securities).

The clock is ticking on this one.

DISCOVER MORE WITH PETITION’S SUNDAY A$$-KICKING MEMBERS’-ONLY BRIEFING. TO SUBSCRIBE AND GET THAT EXTRA EDGE AGAINST YOUR COMPETITOR, CLICK HERE.