New Chapter 11 Bankruptcy Filing - Charlotte Russe Holding Inc.

Charlotte Russe Holding Inc.

February 3, 2019

San Diego-based specialty women’s apparel fast-fashion retailer Charlotte Russe Holding Inc. is the latest retailer to file for bankruptcy. The company has 512 stores in 48 U.S. states. The company owns a number of different brands that it sells primarily via its brick-and-mortar channel; it has some brands, most notably “Peek,” which it sells online and wholesale to the likes of Nordstrom.

The company’s capital structure consists of:

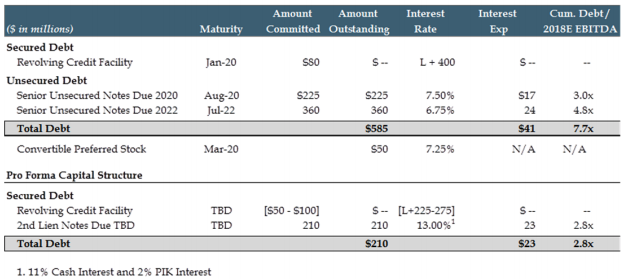

$22.8mm 6.75% ‘22 first lien revolving credit facility (ex-accrued and unpaid interest, expenses and fees)(Bank of America NA), and

$150mm 8.5% ‘23 second lien term loan ($89.3mm funded, exclusive of unpaid interest, expenses and fees)(Jefferies Finance LLC). The term loan lenders have first lien security interests in the company’s intellectual property.

The company’s trajectory over the last decade is an interesting snapshot of the trouble confronting the brick-and-mortar retail space. The story begins with a leveraged buyout. In 2009, Advent International acquired the debtors through a $380mm tender offer, levering up the company with $175mm in 12% subordinated debentures in the process. At the time, the debtors also issued 85k shares of Series A Preferred Stock to Advent and others. Both the debentures and the Preferred Stock PIK’d interest (which, for the uninitiated, means that the principal or base amounts increased by the respective percentages rather than cash pay interest or dividends being paid over time). The debtors later converted the Preferred Stock to common stock.

Thereafter, the debtors made overtures towards an IPO. Indeed, business was booming. From 2011 through 2014, the debtors grew considerably with net sales increased from $776.8mm to $984mm. During this period, in May of 2013, the debtors entered into the pre-petition term loan, used the proceeds to repay a portion of the subordinated debentures and converted the remaining $121.1mm of subordinated debentures to 8% Preferred Stock (held by Advent, management and other investors). In March 2014, the debtors and its lenders increased the term loan by $80mm and used the proceeds to pay a one-time dividend. That’s right folks: a dividend recapitalization!! WE LOVE THOSE. Per the company:

In May 2014, the Debtors paid $40 million in dividends to holders of Common Stock, $9.8 million in dividends to holders of Series 1 Preferred Stock, which covered all dividends thus far accrued, and paid $65.7 million towards the Series 1 Preferred Stock principal. The Debtors’ intention was to use a portion of the net proceeds of the IPO to repay a substantial amount of the then approximately $230 million of principal due on the Prepetition Term Loan.

In other words, Advent received a significant percentage of its original equity check back by virtue of its Preferred Stock and Common Stock holdings.

Guess what happened next? Well, after all of that money was sucked out of the business, performance, CURIOUSLY, began to slip badly. Per the company:

Following fifteen (15) consecutive quarters of increased sales, however, the Debtors’ performance began to materially deteriorate and plans for the IPO were put on hold. Specifically, gross sales decreased from $984 million in fiscal year 2014 with approximately $93.8 million in adjusted EBITDA, to $928 million in fiscal year 2017 with approximately $41.2 million in adjusted EBITDA. More recently, the Debtors’ performance has materially deteriorated, as gross sales decreased from $928 million in fiscal year 2017 with approximately $41.2 million in adjusted EBITDA, to an estimated $795.5 million in fiscal year 2018 with approximately $10.3 million in adjusted EBITDA.

Consequently, the company engaged in a year-long process of trying to address its balance sheet and/or find a strategic or financial buyer. Ultimately, in February 2018, the debtors consummated an out-of-court restructuring that (i) wiped out equity (including Advent’s), (ii) converted 58% of the term loan into 100% of the equity, (iii) lowered the interest rate on the remaining term loan and (iv) extended the term loan maturity out to 2023. Advent earned itself, as consideration for the cancellation of its shares, “broad releases” under the restructuring support agreement. The company, as part of the broader restructuring, also secured substantial concessions from its landlords and vendors. At the time, this looked like a rare “success”: an out-of-court deal that resulted in both balance sheet relief and operational cost containment. It wasn’t enough.

Performance continued to decline. Year-over-year, Q3 ‘18 sales declined by $35mm and EBITDA by $8mm. Per the company:

The Debtors suffered from a dramatic decrease in sales and in-store traffic, and their merchandising and marketing strategies failed to connect with their core demographic and outpace the rapidly evolving fashion trends that are fundamental to their success. The Debtors shifted too far towards fashion basics, did not effectively reposition their e-commerce business and social media engagement strategy for success and growth, and failed to rationalize expenses related to store operations to better balance brick-and-mortar operations with necessary e-commerce investments.

In the end, bankruptcy proved unavoidable. So now what? The company has a commitment from its pre-petition lender, Bank of America NA, for $50mm in DIP financing (plus $15mm for LOCs) as well as the use of cash collateral. The DIP will roll-up the pre-petition first lien revolving facility. This DIP facility is meant to pay administrative expenses to allow for store closures (94, in the first instance) and a sale of the debtors’ assets. To date, however, despite 17 potential buyers executing NDAs, no stalking horse purchaser has emerged. They have until February 17th to find one; otherwise, they’re required to pursue a “full chain liquidation.” Notably, the debtors suggested in their bankruptcy petitions that the estate may be administratively insolvent. YIKES. So, who gets screwed if that is the case?

Top creditors include Fedex, Google, a number of Chinese manufacturers and other trade vendors. Landlords were not on the top 30 creditor list, though Taubman Company, Washington Prime Group Inc., Simon Property Group L.P., and Brookfield Property REIT Inc. were quick to make notices of appearance in the cases. In total, unsecured creditors are owed approximately $50mm. Why no landlords? Timing. Despite the company going down the sh*tter, it appears that the debtors are current with the landlords (and filing before the first business day of the new month helps too). Not to be cynical, but there’s no way that Cooley LLP — typically a creditors’ committee firm — was going to let the landlords be left on the hook here.

And, so, we’ll find out within the next two weeks whether the brand has any value and can fetch a buyer. In the meantime, Gordon Brothers Retail Partners LLC and Hilco Merchant Resources LLC will commence liquidation sales at 90+ locations. We see that, mysteriously, they somehow were able to free up some bandwidth to take on an new assignment sans a joint venture with literally all of their primary competitors.

Jurisdiction: D. of Delaware (Judge Silverstein)

Capital Structure: $22.8mm 6.75% ‘22 first lien revolving asset-backed credit facility (ex-accrued and unpaid interest, expenses and fees)(Bank of America NA), $150mm 8.5% ‘23 second lien term loan ($89.3mm funded, exclusive of unpaid interest, expenses and fees)(Jefferies Finance LLC)

Company Professionals:

Legal: Cooley LLP (Seth Van Aalten, Michael Klein, Summer McKee, Evan Lazerowitz, Joseph Brown) & (local) Bayard PA (Justin Alberto, Erin Fay)

Independent Director: David Mack

Financial Advisor/CRO: Berkeley Research Group LLC (Brian Cashman)

Investment Banker: Guggenheim Securities LLC (Stuart Erickson)

Lease Disposition Consultant & Business Broker: A&G Realty Partners LLC

Liquidating Agent: Gordon Brothers Retail Partners LLC and Hilco Merchant Resources LLC

Liquidation Consultant: Malfitano Advisors LLC

Claims Agent: Donlin Recano & Company (*click on company name above for free docket access)

Other Parties in Interest:

DIP Lender ($50mm): Bank of America NA

Legal: Morgan Lewis & Bockius LLP (Julia Frost-Davies, Christopher Carter) & (local) Richards Layton & Finger PA (Mark Collins)

Prepetition Term Agent: Jefferies Finance LLC

Legal: King & Spalding LLP (Michael Rupe, W. Austin Jowers, Michael Handler)

Official Committee of Unsecured Creditors (Valueline Group Co Ltd., Ven Bridge Ltd., Shantex Group LLC, Global Capital Fashion Inc., Jainson’s International Inc., Simon Property Group LP, Brookfield Property REIT Inc.)

Legal: Whiteford Taylor & Preston LLP (Christopher Samis, L. Katherine Good, Aaron Stulman, David Gaffey, Jennifer Wuebker)

Financial Advisor: Province Inc. (Edward Kim)

Updated 2/14/19 at 1:41 CT